An Introduction to the FX Market

Get the basics of the FX market in under 3 minutes

Background

The foreign exchange (FX) market is the place where one currency can be exchanged for another. It is an over the counter (OTC) market, meaning that it is not traded on any exchanges.

The participants of the market are big international banks which can serve everyone else; making life easier so that individuals do not have to seek each other out.

The FX market is the largest market in the world, with a total of 5067 billion USD in daily transactions (according to BIS). The United Kingdom appears to be the largest hub, doing almost twice as much volume as the second hub, the United States.

How does it work?

To get a good understanding of how it all comes together, first we need to understand what an FX pair is and how it works, before looking to understand the inner workings of the FX market.

What is a currency pair?

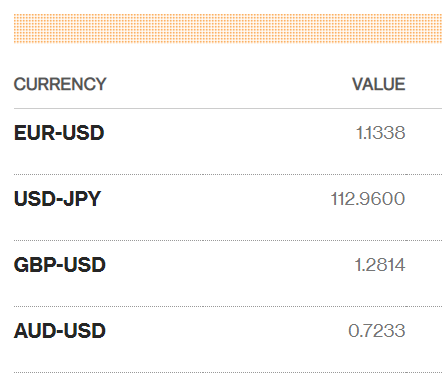

In the FX market, each currency is valued against a different currency. That is, if you were looking to execute an FX transaction, you’d see something like this:

Taking an example from the above table, we can see that we have a EUR-USD pair valued at 1.1338. What this tells us, is that EUR is the base currency and USD is the variable currency; meaning that for each EUR you own, you can get 1.1338 USD.

This is known as an FX Spot quote. FX spots are essentially transactions that can be executed right now and will settle as soon as possible depending on each currency’s settlement days. Typical spot settlement is two days, though there are exceptions to this (Eg. USD CAD will settle in T+1 days, where T is the day the transaction took place).

Note: You can determine the FX Settlement days by looking up each currency’s settlement days and then taking the max of the two. (For instance, USD settlement days is T+1 whereas GBP is T+2, making the pair GBP/USD pair to have T+2 settlement days)

How does the FX interbank market work?

As we already mentioned, the participants of the FX market are big international banks. Each of these banks will have quotes of what they think is a fair price for each pair is, which is how the market price is determined. This type of market is known as a quote-driven market, and the banks are market makers. (Note: The banks quote a different buy and a sell price (bid/offer) for each pair, with the difference being the spread; The spread is how they make their money)

It is worth noting here that each bank might be offering slightly different deals, which means to determine the best price one would have to request a quote from various providers.

Finally, the last thing you need to know is that FX movements are tracked in pips. Pips are 0.01% or 0.0001 (though for USD/JPY it is actually 0.01; you know just to confuse you)

As promised, if you have read the above, you now have a good basic understanding of the FX market in less than 3 minutes. If you have found it interesting and want to learn a bit more about it, keep reading on. Keeping the information at the same level, I will cover some more basic products, valuation insights and risks.

What are some different FX products?

FX Forwards

What are they?

An FX Forward contract is an agreement to carry out an FX transaction at some pre-determined point in the future for a pre-determined rate. Taking, for example, the GBP/USD pair that we have seen before, we know that a Spot contract settles at T+2. Anything that has a settlement date for T+X, where X>2, it is considered to be a Forward contract.

How do you determine the price of an FX Forward?

To determine the price of an FX Forward, we need to consider what factors influence its price. Obviously, the spot rate of the transaction will act as the basis of our valuation; but what else would make a difference? Well, FX transactions mean that we will buy and sell foreign currencies; as such, the interest rate we can get from depositing said currencies will also have an impact on the valuation.

This brings rise to what is known as the Interest Rate Parity.

FX_fwd = FX_spot * (1 + r_v * t_v) / (1 + r_b*t_b)

where,

FX_fwd = The fair forward rate

FX_spot = The spot rate

r_v = The interest rate offered for the period in the variable currency

r_b = The interest rate offered for the period in the base currency

t_v = The fraction of the year for the variable currency (using the correct day-count convention) t_b = the fraction of the year for the base currency (using the correct day-count convention)

Worked Example

Assume you want to calculate the rate for a 60 day forward for our favourite GBP/USD pair.

First, we need to figure out what the rates of return are for each deposit in each currency; and we can do that by referencing an index.

FX Spot rate GBP/USD = 1.2814

2 month USD LIBOR = 2.49900

2 month GBP LIBOR = 0.76575

FX_fwd = 1.2814 * (1 + 2.49900 * 60/360) / (1 + 0.76575 * 60/360)

= 1.60966

FX Non-Deliverable Forwards (NDFs)

Non-deliverable forwards have the same mechanics as normal FX forwards, with the only difference that they cash settle the difference of the contract. That is, there is no physical delivery of the underlying currencies, but rather the difference gets settled in some other currency.

As an example, take a three month USD/CNY NDF (US Dollar Vs Chinese Renminbi) with a notional amount of 1,000,000 CNY for an FX rate of 6.94.

At the pre-agreed rate, you would have a transaction of 144, 092.2190 USD (=1,000,000/6.94).

In 3 months, when you take a fixing you find out that the rate is actually 6.50; So this rate you would have a transaction of 153, 864.1538 USD.

The difference between the two transactions is 9, 753.9348USD which you will either have to pay or receive depending on whether you bought or sold that contract.

Note: Although NDF contracts can be of any underlying currencies, there are some currencies that cannot be traded in the forward markets due to government-imposed restrictions. These restrictions are often imposed to stop FX rate volatility.

FX Swaps

FX Swap contracts are essentially a combination of two FX transactions of the same underlying FX pair that mature at different times. That implies that it can be a Spot-Forward or a Forward-Forward combination.

A simple example of this is entering a spot transaction to sell 100m GBP/USD at an FX rate of X and a 3-month Forward Transaction to buy 100 GBP/USD at an FX rate of Y.

Risks Associated with FX Transactions

Credit Risk

Credit Risk is the risk you face that your counterparties will not be able to meet their financial obligations against you. It is usually calculated in money amount, that signify the money you stand to lose if your counterparty was to default. There are two main counterparty risks associated with FX transactions.

Settlement Risk

When you enter an FX transaction, you are essentially swapping currencies with a counterparty; i.e. you hand over one currency (e.g. USD), and they hand over another (e.g. GBP). As we have seen above, for the transaction to settle, it could take several days. Settlement risk is the risk that your part of the transaction would go through, whereas your counterparty defaults before they pay their part of the transaction.

A particularly famous example of this was seen with Herstatt bank (For more information see here)

Credit Exposure

Credit Exposure describes the monetary loss you would face if your counterparty were to default. There are different measures to calculate the maximum of such loss such as Potential Future Exposure (PFE).

Spot transactions are often modelled as having no PFE exposure and only having Settlement Risk.

Market Risk

Market Risks are the risks that an investor is facing that affect the whole overall market.

Interest Rate Risk

Interest Rate risk, as the name suggests, is the risk that a country’s interest rates could change. That is a macro-economic event that will have a direct impact on the FX rates related to the specific country.

To explain this concept as simply as possible, you can just imagine what would happen to a country whose interest rates on offer keep rising. More and more foreign money will enter the market to take advantage of said rising interest rates. As a result, as more and more people are buying the local currency, the demand will cause the valuation of the currency to rise.