BE UNIQUE

Financial Planning for Millennials

Tips to get the most out of your hard-earned money!

As a Millennial you should know this, you still have time to start saving for your future but starting early might be the best decision you have ever made! Securing your future isn’t complicated. However, the sooner you start, the better you will be. Starting at your late 30s or 40s will mean that you have to save a larger portion of your income.

Here are some steps to help you in your journey, these steps are generic. In the end, you know your situation best and only you can draft a plan that suits your specific needs and goals in life.

Know your spending

Most Millennials live paycheck-to-paycheck because they do not track their expenses. There are multiple apps to help you track and control your expenses out there. You can start using those. However, these apps are not tailors to your specific needs and situation. Therefore, I will recommend you to start an excel sheet to track your income and expenses. Save this excel sheet to Dropbox, Onedrive, iCloud or any other cloud service out there, so it will be accessible to you anywhere anytime. Do a tab for each month, write in your income, your fix costs and the amount of money you have free to spend (do not spend it all though). Doing that will make you aware of your spending habits and will help you in optimizing your expenses and will help you easily answer the question: Where did my money go?

Note: you can use a suitable app as well. But, know this, apps will never be tailored to fit your specific needs and goals.

Know your fixed and reoccurring costs

Write down your monthly fixed costs and your reoccurring costs as well. These costs are the first thing to go away from your “money to spend”. Fixed costs are rent, mortgage, car payments, student loans, utilities, subscriptions, insurances, 401K etc.

Reoccurring costs are payments that are not monthly but rather annually, semi-annually or quarterly. For example, credit card fees or amazon prime subscription. Knowing these costs allow you to budget for them monthly and you won't be surprised if all of a sudden a 59 $ yearly payment is due, it would have been (59$ / 12 months = 4.92 $ monthly).

Use 20% of the remaining money to treat yourself

Alright, this might be controversial for some people. However, living your life for the sole purpose of saving and or financial independent will cause fatigue if you don’t treat yourself to what you want. Use 20% of your remaining money (Income — fix costs) to treat yourself right.

This money can be used to save for a vacation, a nice bag, luxury watch, new laptop, label clothes, you name it. Spending this amount on yourself will allow you to feel that you are not just working in the system to pay rent and live. But you will feel satisfied and may increase your level of happiness.

I put 20% monthly on the side to save for watches, vacations, sneakers (Jordans and Yeezys) and other items I might feel like to buy for myself or others. You can use this for tattoos, hairstylists, nails, hobby (sailing, skydiving, jet-skiing, racing, video games, whatever). Just keep it within 20%.

Define a strict budget for food and outings

Have a second bank account and transfer the amount of money you need for food and outing (monthly) to it. Do not exceed this budget and control it as well. For example, if you plan to use 500$ a month on this, then that’s 16.6$ a day or 117 $ a week. Live it religiously, if you spend 100$ on groceries in a certain week, then you only have 17$ for the weekend and It might be best to tell your friends that you will stay home watching Netflix. Do not use the money for the next week to cover this weekends expenses. It is ok to miss out on a single weekend and just stay home.

Work on your savings

Alright, now to start talking about savings. There are multiple strategies and ways to do it. It also depends a lot on the country you live in (I live in Germany, so I do not care about 401K for example), my needs later in life might differ extremely from yours. Therefore, your saving strategy is yours and yours only. However, the golden rule of saving: save at least three months’ pay for emergencies. You can leave this money in your saving account or in a low-risk investment portfolio. This money should be easily accessible in case of emergencies (car broke down, you need a new fridge, you lost your job, etc.).

After you have saved three months’ pay to the side, start working on your investment portfolio (for some nations the next step would be to max out your retirement accounts). Diversify your investment portfolio to reduce the risk in case of marker drops (you are still young, even if the market drops, your investment still have time to recover if the market drops in a certain point).

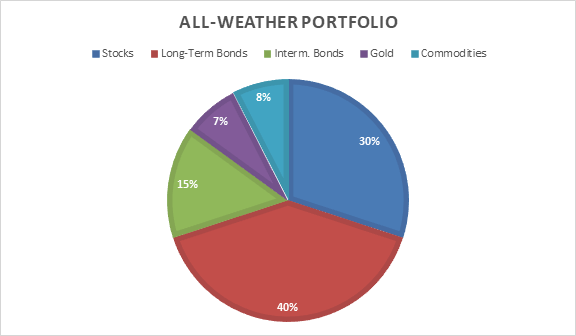

There are multiple ways and advices on how to diversify your portfolio, for beginners I’ll recommend using the All-Weather portfolio by Ray Dalio to start with. You might need to adjust it a little bit depending on where you live (Ray Dalio suggests investing 45% in US Government Bonds, for European, this might be a high risk because these bonds are in Dollar and most European use Euro instead).

I use this portfolio for approximately 60% of my savings, the rest is divided into crypto, REITs (Real Estate Investment Trust) and dividend stocks.

I will not give a suggestion on how to manage your savings. There are multiple books, youTube videos and professionals out there, that might help you in this matter. Do the research for yourself and find out what you feel most comfortable with.

Work on your goals

During all this do not forget your own goals and your own needs. Goals vary from one person to the next. Do not follow others blindly but rather be inspired by them. Everyone before you made a certain mistake when they started savings, learn from their mistakes, try to avoid them but in no way just listen to them and follow blindly if they are not financial professionals.

People’s goals and your goals are different. Their way of life is different than your way of life. I do not care about retiring at 40, I can’t even manage a single weekend without working. Others want to retire early and therefore they are extremely frugal. Someone wants to own a fancy car, you might use public transportation. Each is different and unique and each follows their own goal.

I found a certain youTube series very helpful to get inspiration and learn from others and their lives. “CNBC make it : Millennial Money” series is currently my favorite when it comes to getting inspired and learning from others and their experience. I’ve added the playlist of this series in the video embedded below.

Control yourself

From now until then control your plan. See where you can spend less and what subscription service, for example, you have not been using and cancel it. See the results of your investments and re-balance it if necessary.

Give yourself a pat on the shoulder for a job well-done if you’ve managed your budget and you’ve achieved a goal from your goals.

You will hear a lot of people bragging about the killing they made from their latest investment (usually start-ups or cryptocurrencies). Do not get dragged into this, do not forget, they’ve most probably just bragged about the one time it worked and forgot to mention the times it did not.

If you want to try risky investments and gamble in it, limit it to 5% of your total portfolio. Have the mindset that this money is lost already. Do not get upset if you lose it and do not get dragged in the devil’s cycle if it works and you make a killing out of it. Remember this is just like gambling.

Ask a professional

When you start small, it is easy to manage it on your own and learn along the way. In a certain point of life however, it is not bad to ask and benefit from a professional’s advice. For me, I’ve been seeking a professional’s advice since I started my saving journey. Books, YouTube videos and podcasts might be a source of advice too. However, these sources do not consider your own unique status (income, geographical locations, risk level, age, etc.), be inspired by them but a professional’s help, in the end, is the right way to do it.