Fear of Taking Risks when You Invest? Use This New Approach Instead.

Learn how to Break Free from Loss Aversion with this New Approach to Risk & Volatility, and make your Money Work HARDER for you.

If later you find this article valuable, throw us some Medium love! 🥰 What you can do to support us: Clap up to 50, leave a message, highlight some text if you see fit & be sure to follow. 💌

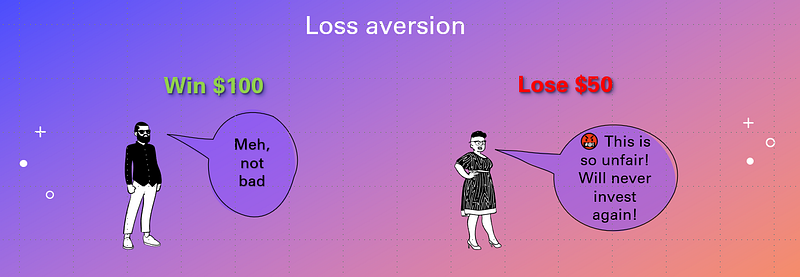

People tend to weight potential losses way heavier than gains. Loss aversion is an irrational behavior in which losses hurt more than gains feel good. I want to make sure that at the end of this article, none of us will have a single bit of loss aversion blocking our path to wealth!

Many of us run away from risks in a bit of an irrational manner, preventing us from growing our portfolio and generating compounding returns.

📌 A Side Story about Not Taking Risks

In 2009, I advised my mom to go to the bank and put part of her savings in an S&P 500 index fund (a basket with stocks of the 500 biggest US companies).

Sadly, the bank clerk told her, “Be careful; this is a risky investment, and you can lose all your money.”

After hearing that, she was scared, followed what the bank clerk said and never invested.

Every day, people miss investment opportunities because instead of looking at risk/reward ratios, they only look at risk. This is one of the reasons why poor people stay poor.

If my mom had made that investment from 2009 until now, the return on investment would be 420%! This would allow her to worry less about retirement.

📌 Investing for the Long Haul: The Near Certainty of S&P 500 Returns

In fact, if you are investing in a 10-year time frame over the last 150 years, the S&P 500 would return positive for 96% of the time.

And no, you can’t “lose all your money” by investing it in a diversified manner and with a long enough time horizon.

We have 150 years of data that shows that the likelihood of losing money investing in the S&P 500 is very low if you are a long-term investor.

⚠️ It’s very sad to see millions of people skipping financial freedom because of this kind of loss aversion bias, but I hope this article can help clarify these misconceptions.

⚖️ The Loss Aversion Bias

Most times, this lack of understanding of risk/reward ratios comes from the loss aversion bias (sometimes also called the prospect theory):

— Investors tend to place more weight on perceived losses than gains:

To lose hurts, yes, I totally get it.

But missing potential gains and not reaching financial freedom hurts even more!

📌 Another Side Story about Painfully Missing Profits

I gave you the example of my mom not investing in the S&P 500 back in 2009, but let me give you another painful example with the respective math.

I have a couple of friends — Tiago and Andre — who were truly frugal and penny pinchers since university. We would get a 300 EUR monthly school allowance from the government, and my friends Tiago and Andre always managed to save most of it (while I was blowing up all the money within a week of receiving it 😇).

By the age of 25, they definitely had way more cash saved than me.

Andre and Tiago were good at saving indeed but, until today, terrible investors. Why do I say that they were terrible investors? Do I say this because they made terrible investments where they lost a ton of money? Nope.

I say this because they didn’t invest at all! They were so afraid of losing money that they just left every dollar sitting in their bank account.

As you know, banks pay very low interest, and sadly, cash in a bank account will be eaten away by inflation, and you will be missing huge gains.

💡 A savings account in a bank is seen as safe, yes, but in the long term, other investments could bring WAY BETTER returns with low risk.

📌 There’s something that is even more painful than losses…

Do you know what hurts even more than losses? Missing profits that could be way bigger than any potential losses. Let me show you some numbers.

— The risk-averse penny-saver who puts the $$$ in a bank savings account:

- Saving $200/month

- Save for 20 years

- Total balance after 20 years: $53,356

- Total interest earned (from the savings account): $5,156

— The non-risk-averse penny-saver who puts the $$$ in an S&P 500 index fund:

- Saving $200/month

- Save for 20 years

- Total balance after 20 years: $174,914.61

- Total interest earned (from the index fund): $126,714.61

Wow, that’s a huge difference, no?! You can almost retire in Thailand with this sum of money!

Saving the same amount of money every month and investing in the stock market would multiply your savings. That’s the beauty of compound investing.

Bear in mind that the calculations above do not even consider that they would increase the savings rate, which is likely to happen when you get better-paying jobs.

“In investing, what is comfortable is rarely profitable.”

— Robert Arnott

📈 The TOP 50 Wisdom for Successful Investors — FREE to download 📈

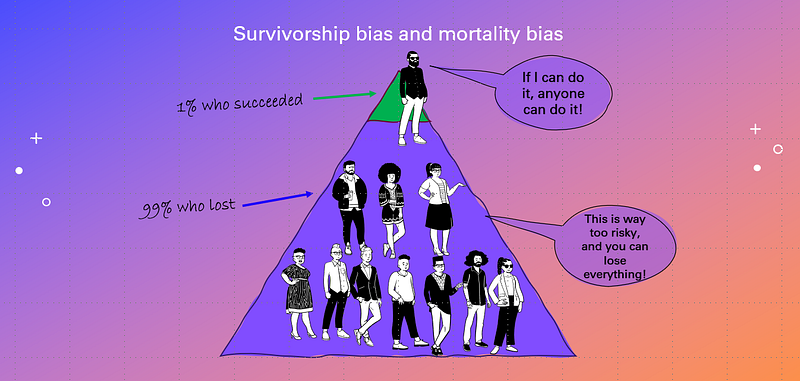

🧠 Blame the survivorship bias?

When it comes to investing, most people talk about their investments ONLY when they are successful. Have you ever seen anyone bragging that they blow up all their money buying degen crypto shitcoins?

For example, I only send screenshots of my crypto or stock portfolio to my girlfriend when the prices are up like 10%. I never share when the portfolio is all red and not doing well. 😏

In the same way, people who succeed tend to brag about it on social media, and successful investors are even invited to share their stories on big media. We always hear the success stories being repeated again and again, although those stories probably represent a small percentage of the investors.

This is not to say that people who lost won’t share it with the world. Losers sharing their losses can have an even greater impact than winners sharing their wins, especially people who are prone to be loss-averse.

For most people, hearing something like “Crypto is risky,” “Bitcoin is too volatile,” or even “invest only the money that you can afford to lose” will put them off without even properly thinking about risk/reward ratios and understanding that a volatile asset isn’t necessarily risky.

For that reason, people miss amazing investment opportunities.

📌 The best way to deal with risk?

Dig deeper. Do your due diligence and learn about whatever you are thinking of investing: a cryptocurrency, a token, a stock of a company, a property market, etc.

💡 Your best investment will be investing in your knowledge so that you don’t fall into the “survivorship bias trap.”

🤔 Given the chance, would you make the following investment? Understanding risk/reward ratios.

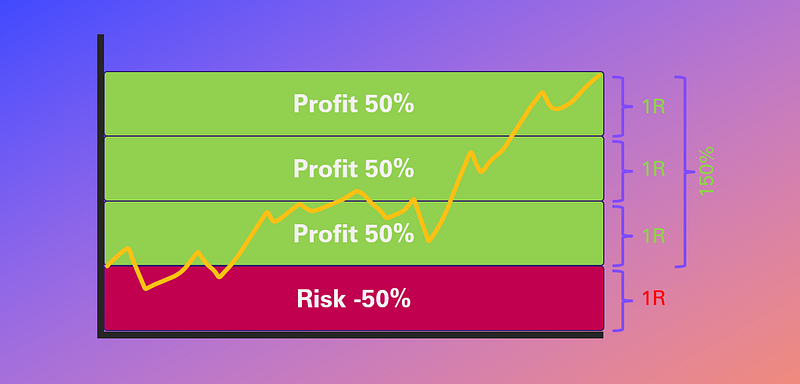

💡 Would you invest in an asset that can: — Lose 50%; or — Profit 150%

Most people would prefer to pass on this investment. No one wants to lose 50% of the capital invested, right?

The problem is that that decision might be (very) irrational.

📌 Why avoiding risk might be (very) irrational?

Every investment that we make is a bet, and we need to calculate the respective potential final payout for those bets. And as you can see on the chart, the risk/reward of this investment is attractive.

Let’s say you invest $1,000 in that investment, and there’s a 50/50 chance of losing or winning.

The potential payout is: ($1000 * 150%) + ($1000 * -50%) = $1000

The payout is clearly positive, right?

And as you can see, there’s 3:1 risk-reward, where the upside is 3x the risk or 3R:1R.

Still, many people might eventually not take this bet because even with a positive payout, if you bet only once, you still have a 50% risk of losing money. I get that.

However, if you can take this bet multiple times, the story is totally different. If I can bet 40 times, the payout is so interesting, and the likelihood of losing money is so low that you should definitely take the bets!

📌 This is why you should never “bet” only ONCE

Let’s look at the math.

The expected payout value or, in other words, the return on investment of betting 40 times is:

(20 * $1000 * 150%) + (20 * $1000 * -50%) = payout

20 * $1500 + 20* -$500 = $20 000

So, if you bet 40 times, this would be a win of $ 20,000.

To eventually lose money, you would have to lose over 31 times out of 40, which is highly unlikely to happen. Yes, the likelihood of losing money in this bet is 0.16%, which is a one-in-630 chance of losing money.

💡 In other words, there’s a 99.84% probability of making money if you bet 40 times.

Although one single bet carries a 50% chance of losing money, we need to zoom out. In life, there are dozens, hundreds, or even thousands of possible bets.

While most people understand probabilities, in the real worst, few seem to believe in them.

You can also increase the odds of winning by spreading these bets across a diversified portfolio that includes stocks, crypto, ETFs, and REITs. This way, the likelihood of having bad bets is way lower.

This is also what people in the Venture Capital space call asymmetric bets.

If you take enough asymmetric bets (where the potential upside is higher than the downside), you will come up as the big winner!

📌The markets are usually even more favorable to investors

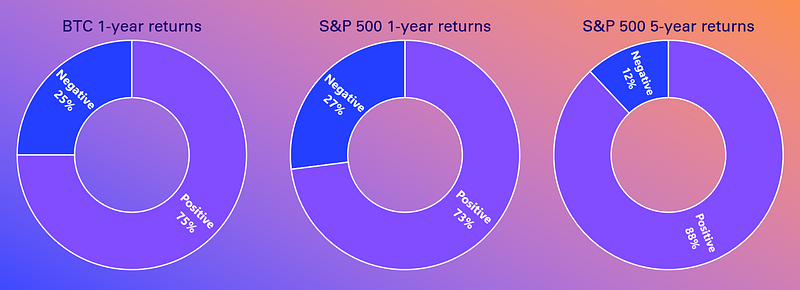

Anyway, although in the example above, I talk about a 50/50 chance of making money. Usually, the markets are even more favorable to investors. Let me give you some examples:

- Bitcoin was positive in 9 out of 12 years (75% positive 1-year periods)

- S&P 500 was positive in 69 out of 95 years (73% positive 1-year periods)

- S&P 500 was positive in 79 out of 95 5-years (88% positive 5-year periods)

So, although past performances are not a guarantee of future performances, there’s still a reasonable chance that some of these assets perform okay.

The conclusion to draw from the chart above is that rather than looking at the outcome of individual investments or individual years, we need to consider the big picture.

When an investor loses after placing a smart bet, they should not be upset, as this is an outcome that can occur. The most important thing is to understand what the best move is according to the probabilities and look at the big picture:

- “I’m going to make 40 bets.” instead of - “I’m betting my life on this one investment.”

By the way, if you want to increase the profitability of your investments and reduce risks, you should definitely take a look at these articles:

- 🎯 I have Found the Winning Investment Strategy to Beat the Odds & Outperform God 🚀

- 💪 The Powerful Investment Strategy You Didn’t Know You Need — Portfolio Rebalancing 🔄

- 🚫 Ditch All those Get-Rich-Quick Passive Income Strategies: Use this Proven & Reliable Way Instead 💡

- 🎭 The Big Fat Lie: “The Rich Get Richer & The Poor Get Poorer” 💸

✨ Conclusion

So to conclude: don’t be chicken-little.

Loss aversion was helpful to humans 100,000 years ago because back then, if you didn't do the right decision, you’d be eaten by a bear or poisoned by a plant that you decided to eat.

💡 It’s okay to take calculated risks in the investment world, especially when it comes to long-term investing with a fairly diversified portfolio.

Also, understand that volatility and risk are two totally different things.

💡 Avoiding investments due to the fear of losses is like avoiding taking an airplane because it travels too fast (despite the fact that it’s very safe).

Understand that the survivorship bias can distort the perception of risk but it’s in your power to research and do the proper due diligence that will allow you to make informed and profitable investment decisions.

Finally, dear readers…

💡 Understand that leveraging probabilities is essential in investing.

By spreading investments across a diverse portfolio and making multiple ‘bets’, you can significantly reduce the risk of losses, even if some individual investments don’t yield positive returns.

If you found this article valuable, why not throw us some Medium love? 🥰 What you can do to support us: Clap up to 50, leave a message, highlight some text if you see fit & be sure to follow. 💌

🌞 Stay in touch with us: