IS AMERICAN’S LOYALTY PROGRAM WORTH MORE THAN THE AIRLINE?

Airline observers and investors were thrown into a frenzy this week with the publication of Stifel analyst Joe DeNardi’s report into the profitability of U.S airline Frequent Flyer Programs (FFPs).

The Stifel report can be found here.

DISCLOSURE: I contributed research and analysis to the Stifel report. I do not hold stocks in the airlines mentioned, nor do I provide investment advice.

As Barron’s reports — How big a deal could this be? DeNardi and Rachal argue that the AAdvantage program could generate about $2.7 billion in 2018, greater than the $2.5 billion in pre-tax earnings implied by the consensus estimate of $3.50 a share in 2018. They call it “an earnings stream immune from incremental capacity or weaker pricing,” while noting that “the risk/reward at current stock prices is incredibly compelling.”

Bloomberg sums up airline mileage revenue succinctly…

“For carriers such as American Airlines riding Citigroup Inc. plastic, or Delta on American Express Co., these programs are a cash cow, a golden goose, or any other fiscal livestock you care to conjure.”

The miles-selling business is BIG business for the airlines

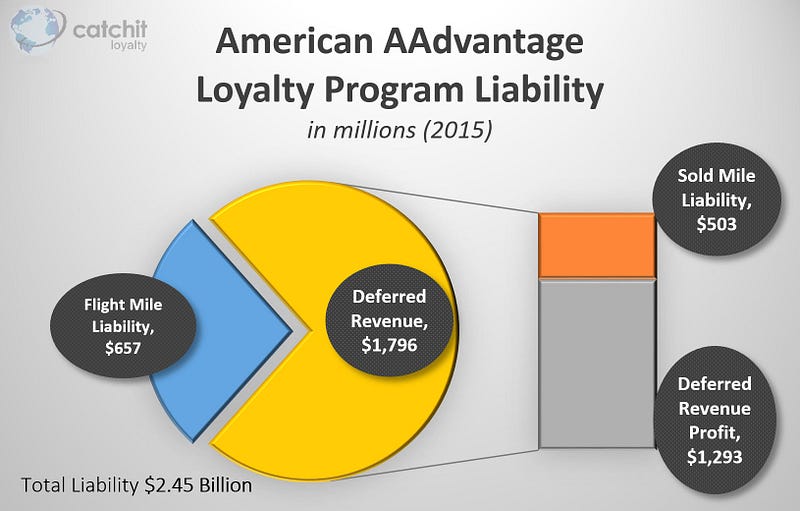

We’ve previously revealed how the American Airlines AAdvantage loyalty program generated an estimated $2.51 billion in revenue from selling miles to banks and other partners in 2016.

In fact, analysis by Catchit Loyalty reveals that American’s Partner Marketing revenue has increased 190% since 2001.

We’ve also revealed details of American’s redemption costs, and the mechanics of mileage-sale revenue and its pathway to the hidden Deferred Revenue Profit contained within the program liability.

What’s new in this report?

Whilst our previous articles have focused on the value and importance of mileage sales to the American AAdvantage program — DeNardi has investigated how mileage sales impact both overall airline profit, as well as the market valuation of American and other U.S. airlines.

For those with an accounting mind — DeNardi has focused his investigations on the loyalty program’s contribution to EBIT.

DeNardi also argues that the market (and analyst community) has significantly under-appreciated the importance and relationship of loyalty program performance to overall airline profit.

Airlines are earning upwards of 50 percent of income from selling miles

The Stifel research has highlighted that loyalty programs are contributing around 50% or more to airline income.

American reported GAAP pre-tax earnings of $4.6 billion in 2015, and $4.3 billion in 2016.

So was the loyalty program responsible for half those profits?

The lack of disclosures by the airlines make it difficult to accurately report precise breakdowns. As a result, it is necessary to apply estimations to aspects of any analysis.

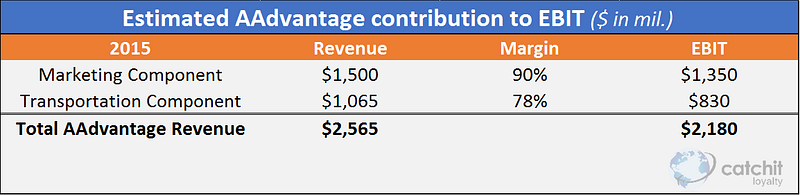

DeNardi has been cautiously conservative in his estimate of EBIT contributions — suggesting that the AAdvantage program contributed around 41% and 49% of EBIT in 2015 and 2016 respectively.

However our own analysis shows that the AAdvantage program was responsible for an estimated 47% of EBIT in 2015 and 55% in 2016.

TIP: For those playing along at home — see this article to understand the Marketing and Transportation components.

American also reported approximately $200 million in other “marketing related payments”, which is not shown in the table above.

The primary variance between the Stifel and Catchit Loyalty estimates is the exclusion or inclusion of these ‘marketing related payments’, as well as revenue recognized due to the absorption of outstanding US Airways’ mileage credits as a result of the merger with American.

According to American’s latest SEC 10-K filing — “At December 31, 2016, all the mileage credits associated with this liability have been recognized in passenger revenue”.

We concur with Stifel’s estimate that the AAdvantage program could generate about $2.7 billion in EBIT in 2018.

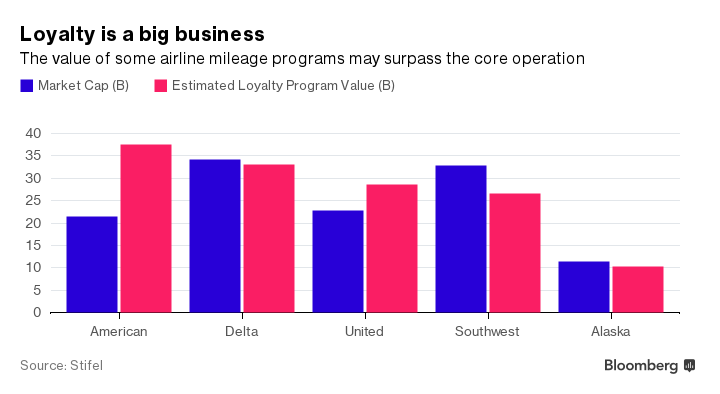

Program Valuation

In his report, DeNardi applies a price/earnings estimate, together with a discounted cash flow analysis to project estimated values for the loyalty programs of U.S. Airlines.

Controversially, DeNardi applies a 22x multiple that results in the American and United loyalty programs being potentially valued higher than the entire market capitalization of the airlines themselves.

No doubt these estimations will cause some level of consternation in airline boardrooms as management teams deliberate as to how to increase the level of transparency and disclosure to the market.

Whilst DeNardi emphasizes that he is not suggesting loyalty programs be spun-off, his report makes clear that airline mileage revenue is underappreciated by the market, and that there is significant upside potential to airlines to increase disclosures.

This is a position that we strongly support.

Rather than spinning-off their programs, DeNardi suggests that airlines report their loyalty programs as a separate entity. He uses the United Loyalty Services model from 2002–2005 as an example airlines should follow.

We would suggest that the best model for airlines to follow is that of Qantas, which reports its Qantas Frequent Flyer program as a separate entity. This has also allowed it to realize additional revenue through commercialization of its Qantas Loyalty brand.

STRONG AFFINITY FOR THE MILEAGE CURRENCY IS CRITICAL

We have been sounding the alarm for some time.

Whilst the Stifel report appears to be all upside for airlines — these massively profitable revenue streams are not without risk.

The risk — is that the most profitable co-brand partnership is only useful if customers perceive value in the airline mileage currency.

If airlines ignore the aspirational attraction of the loyalty program through continual enhancements and devaluations, then the points currency itself becomes worthless if customers no longer desire it

American’s recent changes to its program, which will see an estimated 20 billion fewer miles being awarded to members for flying, will result in potential savings to the airline of around $24.3 million according to Catchit Loyalty’s analysis.

SUMMARY

DeNardi has been issuing client notes and pressing airline management since last August, to increase the levels of financial disclosures.

Increasing these disclosures will not just be of interest to the investment and loyalty communities — but will also benefit the airlines themselves.

DeNardi believes that increased disclosures will force management to improve the core airline fundamentals, rather than using loyalty revenue to mask poor airline performance.

We feel that the Stifel report, together with increased attention from the investment community, will force management to be more accountable for its strategic decisions that affect the loyalty program as well.

Investors starting to pay more attention to the loyalty programs that generate ~50% of EBIT can only be a positive development.

— — — — — — — — — — — —

As a publisher and global speaker on hotel & airline loyalty programs, David is focused on developing strategic solutions for loyalty programs, and is passionate about the critical link between loyalty strategy and the customer experience. David can be contacted here.

— — — — — — — — — — — —

More Articles by David Feldman:

LOYALTY MYTHBUSTERS: DON’T WORRY ABOUT POINTS LIABILITY

LOYALTY MYTHS: IS BREAKAGE GOOD?

THE PSYCHOLOGY OF LOYALTY PROGRAMS

DOES YOUR AIRLINE EVEN WANT YOU TO FLY THEM?

AMERICAN AADVANTAGE CHANGES — WINNERS, LOSERS & MORE LOSERS

— — — — — — — — — — — —

References and Further Reading:

- Catchit Loyalty analysis based on airline 10-K SEC filings, investor presentations, and discussions with airline executives

- Stifel — Valuing Airline Loyalty Programs — Airlines Are Intrinsically Undervalued

- CNBC — American Airlines to soar over 100%: Analyst

- Barron’s — Why American Airlines is Soaring

- Bloomberg — Airlines Make More Money Selling Miles Than Seats

Disclaimer:

- I contributed research and analysis to the Stifel report. I do not hold stocks in the airlines mentioned, nor do I provide investment advice.

- Catchit Loyalty makes every effort to ensure the accuracy and quality of the information available in this article. Due to limited disclosure of program finances, significant estimations are included. Before relying on the information, readers should obtain any appropriate professional advice relevant to their particular circumstances. Catchit Loyalty can not guarantee, and assumes no legal liability or responsibility for the accuracy, currency or completeness of the information.