Exploring Credit Risk and IFRS 9 Models: A Deep Dive into Loan Credit Risk Analysis

This article focuses on two key and popular models used in credit risk management: Credit Risk and IFRS 9 Models, with examples to illustrate their application.

In the fast-paced world of financial lending, where every decision can make or break the bottom line, mastering the art of credit risk management is essential.

Let’s explore these below:

1. Credit Risk Models

Credit risk models are statistical models used to estimate the probability that a borrower will default on a loan.

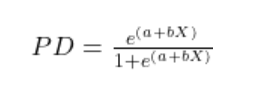

There are several machine learning models used to predict default, and one of the oldest and most common technique is Logistic Regression, which predicts the probability of default (PD) based on various borrower characteristics.

Mathematical Formula: The logistic regression model predicts the probability of default using the following formula:

- (PD): Probability of Default.

- (X): A vector of borrower characteristics (such as annual income, FICO score, debt-to-income ratio, etc.).

- (a), (b): Model coefficients that are estimated from the data.

Example:

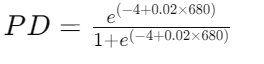

Let’s assume you have a dataset containing loan information, and we’ll focus on one variable here for simplicity, i.e., the FICO score of borrowers.

A FICO score is a type of credit score used by lenders to assess an individual’s creditworthiness. The FICO score ranges from 300 to 850, with higher the score, the lower the credit risk.

Okay, so with that short note, let’s use logistic regression to predict the probability of default based on FICO score.

Given: - Intercept (a = -4) - Coefficient (b = 0.02) - FICO score (X = 680)

Calculation: Substitute the values into the logistic regression formula:

Calculating the above values, we get Probability of default (PD) as 0.993.

This means there is a very high probability (99.3%) that the borrower will default implying they are likely to repay the loan in full.

In real-world scenario, the lender might decide to reject the loan application or charge a higher interest rate to compensate for the risk.

2. IFRS 9 Models

The IFRS 9 (International Financial Reporting Standard 9) framework is published by the International Accounting Standards Board (IASB).

The framework requires financial institutions to calculate the Expected Credit Loss (ECL) on loans and other financial instruments. This standard emphasizes forward-looking provisions, meaning banks must estimate potential future losses based on various economic scenarios.

Mathematical Formula: The ECL is calculated using the following formula:

- PD: Probability of Default (as calculated in the Credit Risk Model).

- LGD: Loss Given Default, representing the percentage of the loan that would be lost if the borrower defaults.

- EAD: Exposure at Default, which is the outstanding balance at the time of default.

Example:

Let’s expand on the previous example by calculating the Expected Credit Loss using the PD obtained earlier.

Let’s assume:

- PD = 0.993. This we have taken from the logistic regression model result above.

- LGD = 40%. Simply put, it means the lender expects to recover 60% of the loan through collateral or other means if the borrower defaults.

- EAD = $50,000 . This is the outstanding loan amount.

Let’s do the calculation: Substitute these values into the ECL formula: ECL = 0.993 x 0.40 x 50,000 = 19860

Interpretation: This means that if the borrower defaults, the lender could lose around $19,860. To be safe, the lender would set aside this amount as a backup, just in case, following the IFRS 9 guidelines.

Importance of IFRS 9 in Credit Risk Management:

IFRS 9 models are vital because they ensure that financial institutions are adequately prepared for potential loan losses. By calculating ECL, banks can maintain healthier balance sheets and comply with regulatory requirements, reducing the impact of unforeseen economic downturns.

Conclusion

In the context of loan credit risk, Credit Risk Models and IFRS 9 Models provide powerful tools for predicting and managing potential losses.

Logistic regression helps estimate the probability of default, which feeds directly into the calculation of expected credit losses under IFRS 9.

Together, these models work together to help financial institutions better assess risk, make smarter lending decisions, and keep their finances stable.

If you’re working in the BFSI sector, especially in risk management or regulatory compliance, understanding and using these models is a must.

Hope you liked this tutorial and found it useful.

If you are interested in this subject, please explore the following blogs:

If you’re as passionate about AI, ML, DS, Strategy and Business Planning as I am, I invite you to connect with me on LinkedIn.