Even if You Want 7 or 8 Figures, You Still Need a Budget

This Problem Hurts the Rich as well as Middle Class

Everyone wants to be rich, but even the rich need to have a budget.

You may think this doesn’t make sense, but look at all of the people who have become rich and famous, a few end up broke because they lived beyond their means.

No matter how much money you make, you should live on a budget and have savings to cover you.

Let’s take a look at a few of the rich and famous.

Antoine Walker was drafted in 1996 and played for the NBA’s Boston Celtics, Dallas Mavericks, and Miami Heat. He blew over $110 million due to a lavish lifestyle and bad investments. Walker declared bankruptcy and now has a networth of $250,000.

MC Hammer known for his song Can’t Touch This was earning as much as $31 million a year thirty years ago before filing for bankruptcy in 1996 with a debt of $13 million. His large entourage of 200 people and lavish lifestyle of a mansion, racehorses, and line of cars came back to hurt him. Two lawsuits of copywriting songs didn’t help either.

Musician Michael Jackson was $400 million in debt when he suddenly died in 2009. Numerous lawsuits and a lavish lifestyle depleted his vast fortune as the King of Pop.

Emmy winning actor Nicholas Cage blew $150 million in 15 years on homes, automobiles, and rare artifacts.

Former heavyweight boxing champ, Mike Tyson, earned over $400 million in his career but he declared bankruptcy. He owed money to his manager, trainer, IRA, lawyers, divorce, and child support.

This list goes on and on.

Living a glamorous life didn’t help these wealthy people.

Not enough in savings

Living above ones means applies to many people and not just the rich.

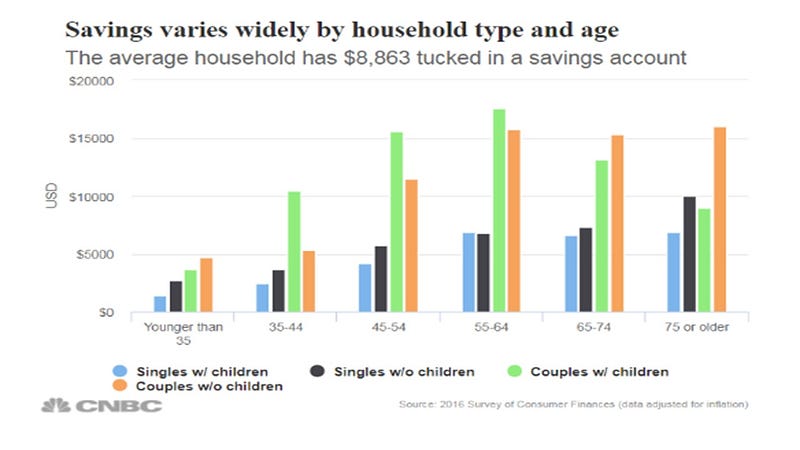

Before the financial crisis from the corona virus, the average household had a savings of $8,843 in their bank account according to CNBC.

For couple who were 34 and younger without children, they had $4,727 in savings. For single people without children, they had $2,729 in savings.

Then as people were older, married couples between the ages of 35 to 44 with children had a savings of $10,399 in savings. The next age group between the ages of 45 to 54 had the most in savings at $15,589.

Couples between the ages of 55 to 65 had the most in their bank with $17,587.

Chartered Financial Analyst and Chief financial analyst for Bankrate.com Greg McBride said, “The ultimate destination should be enough to cover six months’ expenses, perhaps nine to 12 months for sole breadwinners or self-employed individuals.”

Most people don’t have enough in savings and one or two months from their own financial crisis.

The solution

Since many people don’t have much in savings as the rich and famous mentioned earlier, these similar issues affect the average person.

One solution is to save more money.

To do this, an easy way is to create a budget.

If a business can have a budget, then shouldn’t a person or family have a budget as well?

Suze Orman recommends to have a savings of eight months to a year to cover living expenses. After going through the corona virus this year, this makes a lot of sense.

Statistics show 60% of millennials don’t have an emergency fund of $1000.

In general, a budget should cover your housing, transportation, and food expenses.

Once these areas are covered, savings should be increased followed by investments.

To get started, start with saving $25 or more a month and then gradually increase how much you save the next month. This will be hard at first but having this extra money will help when you really need it.

Changing your habits is a start and will increase how much you have saved for those rainy days when an emergency happens.

The savings may not generate a lot in interest for you but the security of having the money available will be there when you need it.

You never know when your car breakdown or you need to make a last minute flight to visit family.

I encourage you to read these articles next:

Tips for the New Stock Investor

How Much the Average Person has in Their Emergency Fund

Are you working to increase your emergency fund?

Tom Handy is a top Investment and Bitcoin writer on Medium, and father of two kids. He retired from the Army and sits on several non-profit boards. Tom is the top Yelper in his community and a top Google Guide. He’s on several social media channels and you can find him on Twitter @tomhandy1 and Instagram @tomhandy1.

This article is for informational purposes only. It should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any significant financial decisions.