Evaluating My Asset Allocation: June 2019

Understanding asset allocation on a portfolio is one of the most important steps in the investing journey.

Diversifying our investments into different assets classes allows investors to get exposure to different levels of risk and different risk factors. No matter how small or large our portfolio is, spreading money over different baskets helps all types of investors against the rotten apples.

When calculating my net worth, I have mapped all my assets and ended up noticing the assets classes I am actually invested on.

The Breakdown

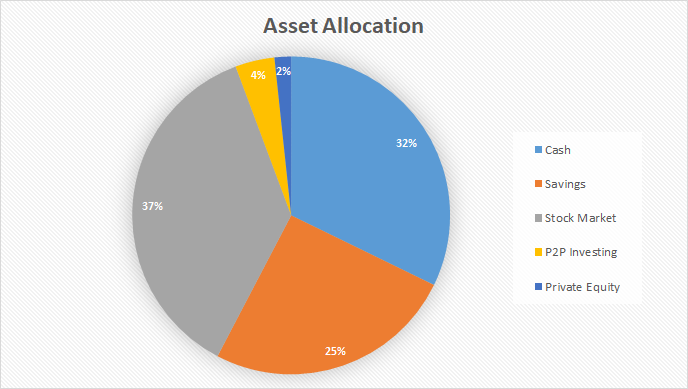

Since I have several savings and investment accounts, I am summarizing my assets into 5 main categories:

- Cash

- Savings

- Stock Market

- P2P Investing

- Private Equity

Cash is money on current accounts or savings accounts that I can easily move money from without penalties or having to wait several days to have it available. This also includes a 6-month emergency fund just in case of unexpected expenses or a job loss. Bonds and money market funds are also included here.

Savings is the money I put into special savings accounts such as housing savings accounts and retirement/pension plans. This is money that I cannot touch and that I contribute to every single month in automatic mode. All the money in these accounts is tracked but not really liquid money.

The stock market is currently my largest asset class if I do not count my own personal real estate which is always debatable if it is an investment or not. Here I have a mix of ETFs and stocks but for the purpose of keeping it simple, I combined both into this calculation. I have discussed my portfolio before and I do an update every month.

P2P Investing and Private Equity are small chunks of my total portfolio. I am a new investor in P2P (less than 2 years) and I am having quite good returns without much effort (between 8% and 13%) depending on the platform. There is a major risk I can see for P2P which is recession behavior. Most of the platforms, loan originators, etc did not handle a recession before so in my view that will always limit its weight on my portfolio. Same goes for private equity as liquidity is really long term and the failure rate of startups is really high. Therefore, little money goes into it.

So now let’s jump into the percentages:

So as mentioned my stock market asset class is the biggest chunk of the pie. No surprise here. I do hold different accounts for different purposes and when adding everything up I have 37% of my money directly and indirectly into stocks.

Then in second place is money with 32%. Why? Several reasons actually. So a 6-month emergency fund that covers not only my monthly expenses but also some free-float. Also, I am expecting some relevant expenses on furniture and house works in the coming 6 to 8 months so I am keeping more money aside.

“ I had the temptation of investing the money I would need in a short time frame and I got burned so I learned my lesson.”

Also, a possible recession or a strong pull back on the stock market, are other reasons that make me hold a little bit more cash than what I would normally do.

Then are my savings with 25%. Money that is not really growing that much but I get some tax benefits with a guaranteed interest rate. I could argue this is not the best ROI products but bring safety and predictability to my portfolio.

Finally, the 2 small chunks are just a way to get a little extra on money that I call the “play money”. I take the change the chance to have higher returns for a little more risk on money that in theory would not cause an impact on my financial life. But obviously losing money always has an impact on any investor.

The Next Month Plan

Depending on how the stock market behaves the next weeks and whether we are expecting the Fed to cut rates we might have a small rally in the stock market. On the other hand, we are still under a volatile environment with all the trade wars. The bond market can also be seen as signaling a possible recession.

So I might allocate some more money into the stock market if we have a pullback on the most recent uptrend. I am also counting on the tax return money in July so this would be fully invested into the market.

Long term I wish to allocate more money into the stock market and make it at least 60% of my portfolio.

What is your portfolio allocation? Let me know in the comments below.

If you like my content, please check my other stories:

Disclaimer: I am not a financial advisor. Always do your own research when investing in stocks.