EBITDA: The Pros and Cons of a Controversial Accounting Metric.

“We won’t buy into companies where someone’s talking about EBITDA.” — Warren Buffett

“I don’t like when investment bankers talk about EBITDA, which I call bullsh*t earnings.” — Charlie Munger

Quite the harsh reaction from two of finance’s legends.

You may have heard of EBITDA before, but what exactly is it?

And why do legends like Buffett and Munger despise it so much?

What is EBITDA?

EBITDA stands for earnings before interest, tax, depreciation, and amortization.

It’s used as an alternative to net income, but as we’ll discuss later, it can be misleading.

EBITDA = Net Income + Taxes + Interest Expense + Depreciation & Amortization

It’s important to know that there is no legal requirement for companies to disclose their EBITDA, due to it being a non-GAAP metric. However, it is quite simple to find a company’s EBITDA through its financial statements.

Earnings, tax, and interest are in the income statement and depreciation and amortization are in the cash flow statement.

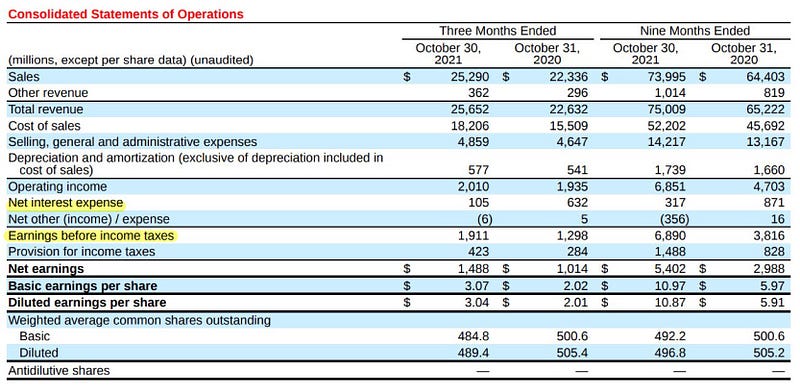

Finding a Company’s EBITDA

Above is the income statement and statement of cash flows from Target’s Q3 10-Q filing. Highlighted are the components relevant to finding Target’s EBITDA.

Following the equation previously mentioned, we first take earnings before income taxes, or EBT, and add back net interest expenses.

For this example, we’ll look at Target’s trailing 9-month numbers.

EBT + Net Interest Income = Earnings Before Interest and Tax (EBIT)

$6,890 (EBT) + $317 (Net Interest Income) = $7,207 (EBIT)

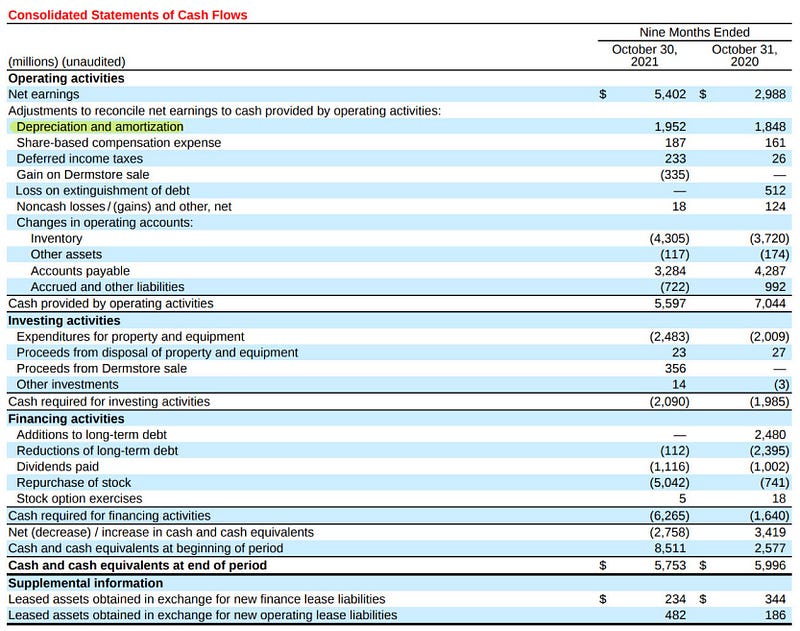

Now that we have Target’s EBIT, we just need to add back depreciation and amortization, found in the statement of cash flows.

EBIT + Depreciation & Amortization (D&A) = EBITDA

$7,207 (EBIT) + $1,848 (D&A) = $9,055 (EBITDA)

Thus, Target’s trailing 9-month (ended Oct. 30, 2021) EBITDA was $9,055 (in millions).

Pros of EBITDA

The concept of EBITDA emerged in the 80s as LBO investors were analyzing troubled companies that needed a financial revamp. These investors used EBITDA to determine whether these companies could meet its interest payments after reshuffling the capital structure (for more info, look here).

So why do investors sometimes use EBITDA to analyze and measure profitability between comparable companies, rather than just net income?

EBITDA can display a company’s financial performance without accounting for its capital structure.

Often, EBITDA is used in valuation ratios such as EV-to-EBITDA and EBITDA-to-Sales (essentially EBITDA margin).

EBITDA can be a quick way to determine the cash flow a company has available to pay the debt on long-term assets, such as property, land, and vehicles.

EBITDA also makes it easier to compare the financial health of different companies and capital structures. The reason for this is that interest, which is influenced by a company’s choice of financing, is ignored.

Taxes are also ignored, since it can be easily affected by realizing investment gains and acquisitions.

Lastly, calculating depreciation & amortization can be subjective and difficult to quantify, and thus, is ignored in the EBITDA calculation.

EBITDA is also used when analyzing merger & acquisition (M&A) opportunities. Since a company’s debt is typically not assumed by the buyer, a buyer wouldn’t care as much about how the company is financed. Cash flow will probably be more important.

When analyzing specific companies, you’ll notice that unprofitable growth companies will probably feature EBITDA in their presentations and earnings calls rather than net income. From the management team’s perspective, this is done to give investors a better idea of profit trends, but this can often blur the company’s real financial performance and health.

Cons of EBITDA

Some analysts and investors will claim that EBITDA can be thought of as a proxy for cash flow. This is insane.

EBITDA is still a ‘non-GAAP’ metric. This means that companies may display their own accounting figures, thus, reporting standards will vary from company to company. It is important to understand how the underlying company calculated its EBITDA.

Often, companies will emphasize EBITDA over net income and claim to achieve ‘positive EBITDA’ simply because it is a flexible metric and can be manipulated to distract from real problems in the company’s financials.

Investopedia best describes a common criticism of EBITDA, which is “it assumes that profitability is a function of sales and operations alone — almost as if the assets and financing that the company needs to survive were a gift.”

Completely ignoring the cost of assets and cost of debt strips much of a company’s financial picture. In addition, depreciation and amortization are ‘non-cash items’ that will inevitably turn into a cash cost. Eventually, deterioration of equipment will cost the company money to replace old equipment or maintain software. This can’t be tossed to the side as if it doesn’t exist.

Lastly, EBTIDA makes a company seem cheaper than they really are. Since EBITDA adds back certain costs. The EBITDA value will be higher than traditional bottom-line earnings, thus resulting in lower valuation multiples. A company at 5x EBITDA may seem ‘cheap’ but could actually trade at 35x earnings.

In investing, you can’t rely on one indicator or metric when finding investment opportunities. This is especially true for EBITDA.

If you do indeed look at a company’s EBITDA multiple, be sure to also look at other metrics that will help show the full story of the company’s financial standing.

Thank you for reading! I hope you found this to be valuable and insightful!