Earn 10% interest on cash, pay 2% on loans, and trade crypto like a pro: Welcome to the new world of banking

4 next-gen banking tools you can start using today to improve your finances

If you have cash sitting around (i.e. not in an investment account) that isn’t earning 10% interest annually, today is the day to change that.

How, might you ask? It’s all made possible via defi and crypto lending. If you’re new to the space, I have another article coming shortly to explain the basics, and I’ll link it here when it’s available.

In the meantime, this article will cover the following:

- How to earn >10% interest on your cash

- Blockchain + traditional bank = The future bank

- How to trade crypto like a pro without doing anything

- How to access 2% APY lending

I’m continually surprised by the number of what I believe are well-informed individuals in this space (future finance) who aren’t aware of some of these platforms. I figure if they aren’t aware of them, then there’s a large audience who could find this information helpful.

In writing this article, I assume the reader is familiar with Bitcoin and other cryptocurrencies, has a basic understanding of how the blockchain works, and a working knowledge of how to access these resources (i.e. via an exchange or Coinbase or the like).

NOTE: Buying crypto on Robinhood does not count/will not work. It’s not a true wallet, in the sense that one cannot send crypto directly to the platform, and if you buy crypto on Robinhood, you cannot transfer it to an external account.

Also, some of the following links are personalized links — would appreciate your clicking on them as thanks for the knowledge I drop here!

How to earn +10% interest on your cash

It’s all about defi (decentralized finance) and crypto lending. Here’s the deal.

There are a lot of people whose net worths have increased tremendously on paper with their Bitcoin, Ethereum, Doge, and other cryptocurrency investments.

The challenge is we largely live in a world where these are not yet readily accepted methods of payment for everyday things like food, clothes, houses, or cars (though that may be changing soon with Tesla).

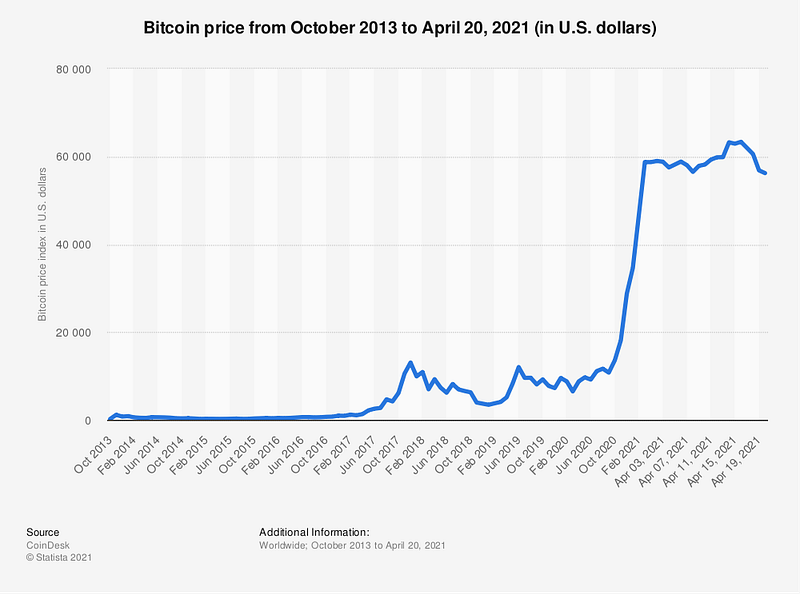

So, these individuals somehow need access to cash. However, neither are they ready to sell their crypto because, well, this:

So, what do they do?

Enter crypto lending. With traditional lending products, you have to fork up some kind of collateral to get access to cash so the lender is protected in the event you default on your payments.

What defi has enabled is a person wanting to borrow money can give a lender custody of their crypto. Then, in the event the borrower defaults on payments, the lender takes possession of the crypto as repayment — which they’re more than happy to do, as the underlying asset (i.e. Bitcoin) is demonstrating there’s still massive appreciation to be had.

However, these lenders desperately need access to cash, and they’re willing to pay for it — up to +10% interest APR. That’s where you and I come in.

We go to their platforms, give them our cash, which they turn around, and loan to borrowers at some nominal rate (usually around 6–8% APR).

The best part here is, so long as you have faith in the institution and crypto market as a whole (it just passed $1 trillion earlier this year, so I don’t think it’s going anywhere anytime soon), it’s a fairly safe investment.

Worst case scenario, the borrower defaults, the institution sells off the underlying asset and repays the loan you’ve provided them. Unlike traditional lending, the institution doesn’t need to go and seize a house or a car and liquidate it before it can repay your loan. It’s instantaneous as part of the smart contract of the loan.

Enough talk already! Here’s how you do it. Unfortunately, the process today is a bit cumbersome, but there are some companies out there looking to change it (which I’ll talk about in the next section).

- As is today, there aren’t any easily accessible institutions where you can just send them cash (unless you live in the EU or the UK), and earn interest directly. Today, you first need to purchase a stablecoin like USDC or USDT. These two have the largest market caps ($11bn and $40bn respectively), and I tend to lean towards USDC because it’s easy to access with a Coinbase account. Ultimately, you can buy it anywhere so long as you can transfer it out (DO NOT USE ROBINHOOD).

- Once you have USDC in your possession, then you need to transfer it to a lender. Two of my personal favorites are Nexo and Celsius. I’ve been using both of them for over a year, and while they have some differences, they typically pay some of the highest interest rates of any platform. Currently, Celsius is paying 10.5% interest, compounded and paid out weekly, on stablecoin, whereas Nexo is paying 8%, compounded and paid out daily. However, if +10% of your wallet with them is in Nexocoin they will bump your interest rate to 10%. With either platform, you can actually boost your interest rate even further (to around 12%) if you elect to take your payment in their respective “coins”.

- Now you can sit back and collect your interest! At some future date if you elect to pull your coin out, you'll need to transfer it back to an institution (like Coinbase) that can take your stablecoin and convert it back to cash.

One of the best things about this entire process is the time and cost of moving large sums of money around between your exchange and the defi lenders is it costs pennies and takes seconds.

The longest leg of the entire journey is getting money from your bank to your exchange (Coinbase can take up to 14 days to transfer money in from your bank), and from your exchange back to your bank account.

Also, note that there are a TON of the defi institutions popping up. One of the biggest ones is called BlockFi. I just typically haven’t used them because Nexo and Celsius have always had better interest rates — and that’s what I’ve cared about the most.

Blockhain + traditional bank = The future bank

In the previous section, I highlighted a couple of issues with the current system. The biggest blocker of why I don’t put all of my liquid assets in with a crypto lender is due to the lag time of going from cash to stablecoin to the lending institution, and then back to cash again so I can use it to pay off my credit card.

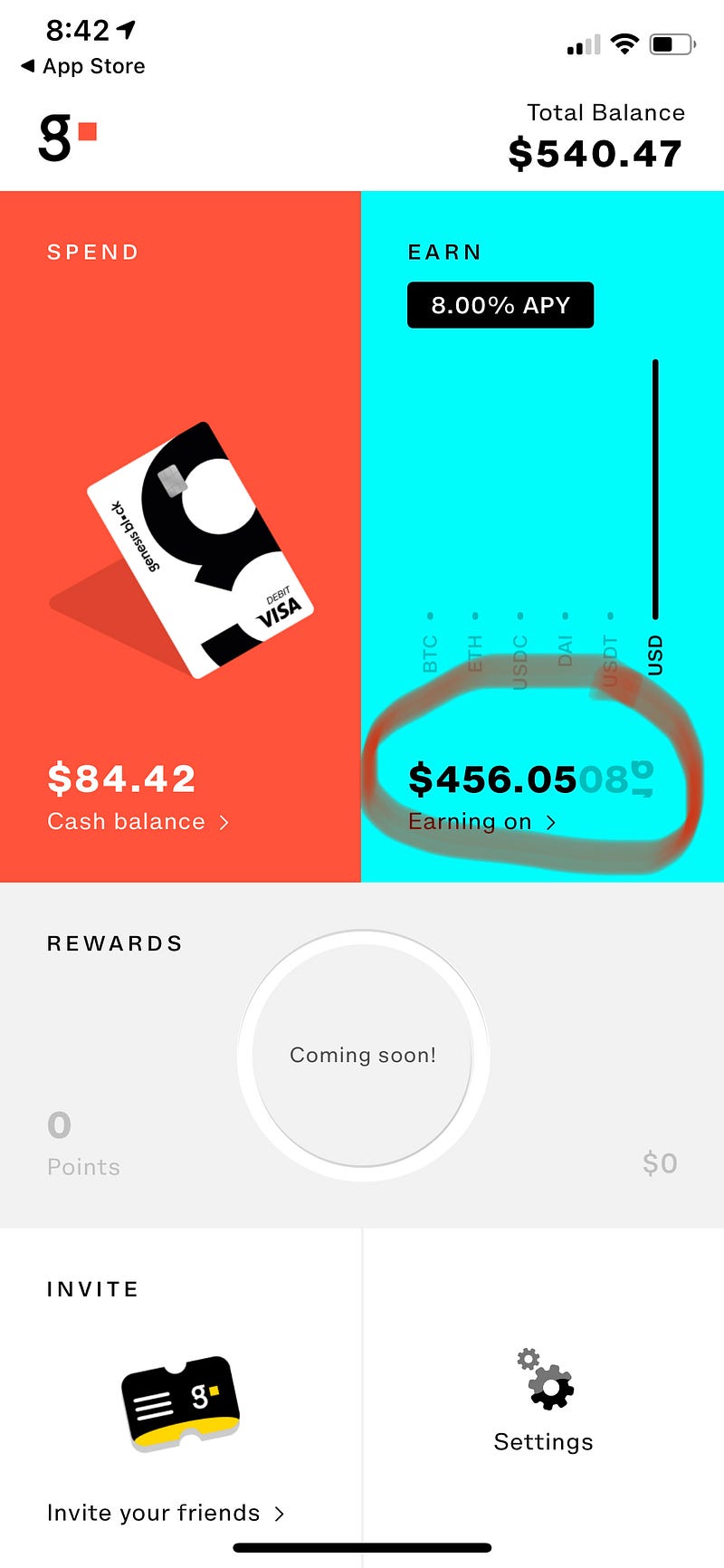

And then along came Genesis Block.

I believe what these guys are building is the bank of the future. What they have done is pair a regular cash checking account with a crypto savings account that earns anywhere from 8–10% APY.

As a consumer this allows you to instantly transfer funds between your checking account and your high yield savings account. So instead of having to go through the rigamarole I described in the previous section, you literally just hop on the app and move money between the accounts as needed.

One of the things I love about their platform is you can literally see the interest accumulating by the second. There’s a little number counter that shows how much interest you’re earning every second.

The two biggest downsides right now are (a) they’re in a closed beta stage, so if you’re interested, you’re going to need to fight your way down their waitlist and (b) there’s a $1k max limit on what the account can hold while they work through the beta.

However, I’m hopeful about the future here, and believe this truly is the future.

One other thing I should add. The platforms I listed above (BlockFi, Nexo and Celsius) all theoretically have debit cards you can use to get access to your funds and could potentially fill some of the gap I’ve felt on their platforms. However, I’ve been on the waitlist for that product since I signed up over a year ago, and have yet to see anything. So thus far, in my mind, it’s still theoretical.

How to trade crypto like a pro without doing anything

I’ve long been interested in trading crypto, but between my day job, wife, kids, etc. it has been hard to find the time to dedicate to that endeavor. I have friends who’ve made a lot of money doing this.

I’ve always semi-lamented my lack of involvement there. And then I ran into eToro.

Turns out, these guys are huge and going public via a SPAC IPO this year (it never ceases to amaze me how often I come across these huge companies I’ve never heard of in my entire life…).

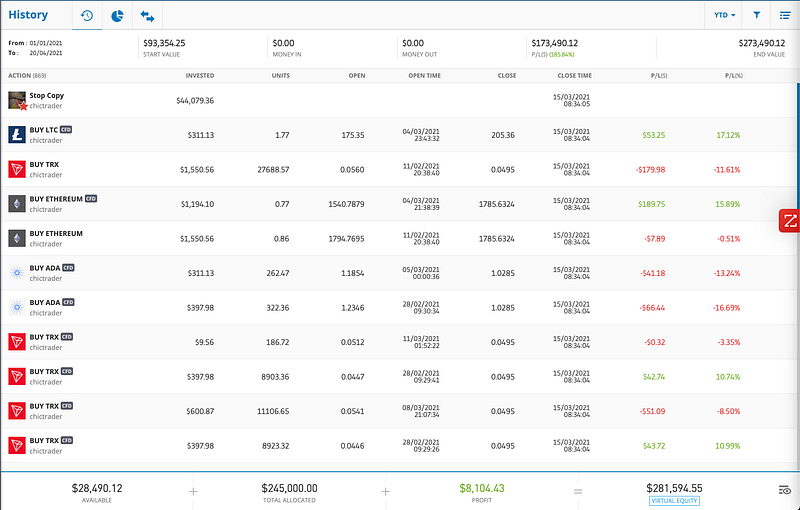

eToro is a crypto trading platform, with a really interesting twist. When you go on eToro and create a portfolio, you have the ability to copy other traders. There are people who literally make a living off trading on eToro, and they’re damn good at it. They spend their entire day watching the market, researching trades, seeking to understand trends, and moving positions between different currencies. It’s amazing.

No longer do I need to feel the impetus to be the expert trader, I just need to find people who are and then set my portfolio to copy them.

The platform takes a bit of learning to get used to it. They know this though, and thus every new account comes with $100k of virtual currency you can use to play around with to get a hang of how it works — which has proven incredibly useful. I started with $100k about 6 months ago, and in that time my portfolio has grown to nearly $300k. Unfortunately, it’s all in the fake, virtual currency, but it does give a good indication of what’s possible on their platform.

How to access 2% APY lending

Finally, one of my new favorites. There’s a ton I could say about these guys, and maybe I will in a future article — but the main thing I wanted to address here is how to access 2% interest rate debt.

The company is called M1 Finance, and they break the mold of this article a bit as they are not a crypto-related institution, but more of a new-age bank with some really cool products they’ve cooked up.

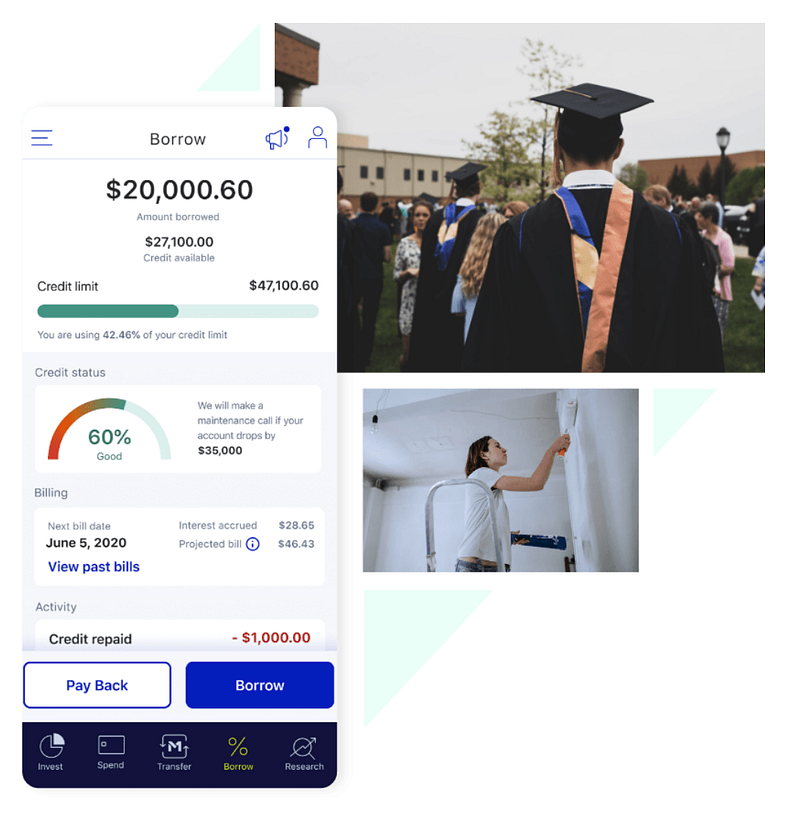

One of the products they have is their brokerage-based line of credit. This product works very similarly to how I described the crypto lending product above — but the difference is instead of taking crypto as collateral, they use your brokerage assets and allow you to borrow up to 35% of the value of your portfolio.

So for instance, suppose you have a brokerage account with $30k in it. M1 will give you access to a ~$10k line of credit. From there, you can transfer the cash directly to your bank account, and have immediate access to the funds. No credit check, no complicated forms to fill out — instant money.

From there, M1 charges you 2% annualized interest, monthly ($10k * 2% = $200 / 12 months = $16.67 / month), which as long as you pay the interest, you can float the line of credit without further penalty.

One cool thing you can do is, if you already have a brokerage account with another broker, you can request to transfer the account over with all the underlying positions already in place, without having to start fresh on M1, and then get immediate access to the line of credit.

The biggest risk here is if the stock market drops, or your brokerage account drops below a certain dollar value, M1 may sell off your stocks to cover payments against the line of credit.

Defi is the future

These tools have all come out in the few years, and it seems like new ones are coming out every day. And every one of them gets me more excited than the last, as it feels like tools that have historically only been available to the uber-wealthy are becoming available to the rest of us.

As decentralized financial tools become more and more ubiquitous, we’ll continue to see the democratization of money. I can’t wait to see what comes next.

Thanks for reading! If you have any questions or would like to hear more about something specific, feel free to leave comments below or send me a note on LinkedIn.

Click here to book time with me during office hours if you’d like to chat.