Digi Q4 results now CelcomDigi

The Celcom merger added 3,956.51 to the current ~11,732 million total shares outstanding based on the current filing, therefore, adding dilution to the existing ownership of Digi’s shares. Digi has issued shares to Telenor to reach equal ownership following Telenor’s payment of RM300 million to Axiata via the Circular notes seeking investors to fund the Cash Consideration through existing borrowing facilities. Digi’s previous Total diluted shares outstanding were 7,775 million before the merger. Digi’s price movement had been stagnated since 2015 although owners of Digi’s shares can still enjoy dividends for daily expenditures.

Digi was traded at the high of 4.05 in March 2022 in the chart and down to the lowest 3.20 level in June 2022, net profit dropped to RM236.15 million from RM264.83 million a year earlier as revenue due to the implementation of Malaysia’s one-off Cukai Makmur or Prosperity Tax for 2022. Perhaps, the merger could help to reinvigorate the capital appreciation of CelcomDigi with their combined forces.

Earnings

Q4 earnings beat primarily with the merger of Celcom to DIGI across all the segments Postpaid, Prepaid, MVNO, Fiber, and Digital. The new Company is called CDB in Bursa Malaysia in tandem with the release of Q4 earnings on 24 Feb ‘23.

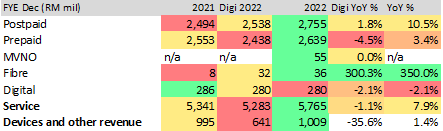

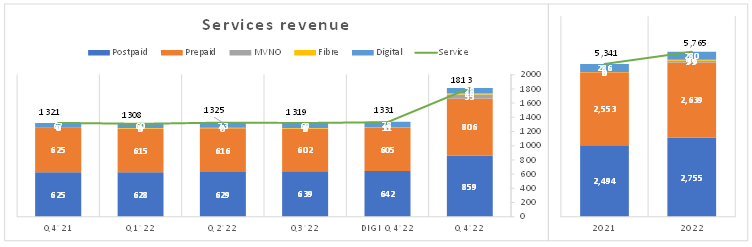

Celcom’s 1-week accreditation to CelcomDigi, CDB starting 30 November 2022 increased to RM1,813 million from Celcom of RM491 million in year-end 2022 at 27% contribution to CDB. Celcom’s 1-week contribution provided an overall uplift of +36% traction to quarterly revenue at a double-digit growth rate. On annual basis, we see the addition of ~8% in Services revenue.

Digi Q4 services revenue was RM1,331 minor incremental adds in comparison to Q4 and Q4’21 however the services annual 2022 was tepid weaker at -1.1% YoY. The larger contribution was largely by the strong traction with Fiber and Digital (Enterprise) charting at 23% and 13% growth. Digi Q4 Enterprise is seen as returning to grow despite the weaker setup seen in Q4’21 until Q3’22.

Digi’s Postpaid 2022 provided minor improvement at YoY 1.8% although the Prepaid cannot offset the minor contraction at -4.5%. Prepaid revenue was lower with the end of the Jaringan Prihatin program. They believe Celcom Digi Bhd (CDB) is set to benefit from the return of migrant workers, quoted the article.

2022 Results

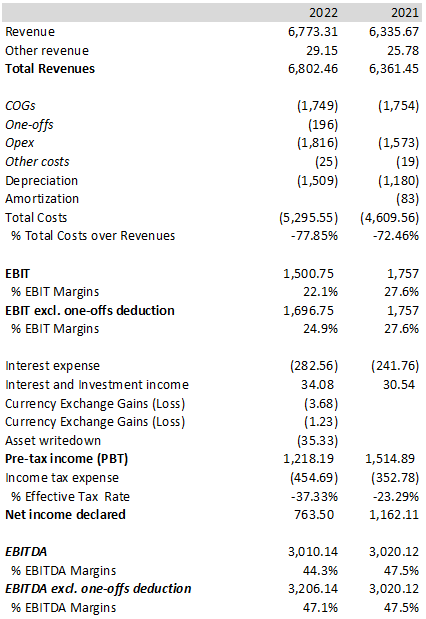

COGS, One-offs, and Operating Expenses (Opex) numbers in the table above were derived from CDB’s MDA quarterly report Q4. Opex including one-off cost will be 2,012m. For other costs, the missed numbers were based on my calculation and were believed to be reconciliation errors marked by the italic font.

Current year EBITDA in 2022 could have a higher percentage at a 44.3% rate valuing at 3,010.14m and 47.1% with one-offs exclusion that could be normalized back to the prevailing rate at 47.5% in 2021 before the merger. However, EBITDA could hide the actual depreciation values behind EBITDA when valuing the asset. The larger depreciation was due to Capex’s seen as early as 2019 when Digi invested in fiber and more recently invested in the 5G network in 2022.

Thus EBIT Margin can be deduced to 24.9% after the merger and 22.1% excluding one-off costs. Digi was valued at an EBIT margin of the average of 32% until COVID-19 in 2020 to the bottom in 2022.

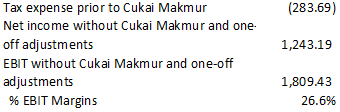

The last annual effective tax rate (ETR) was 37% in 2022. Assuming the previous ETR in 2021 of 24%, before Cukai Makmur tax, and with the current one-off expense exclusion, Pre-tax income could have produced an addition of ~500m to the Net income at 1,243m instead of ~763m (my adjusted numbers concerning the claim CDB’s MDA quarterly report Q4). EBIT margin would be improved to ~27% on the upside.

The absence of a prosperity tax in the revised Budget 2023 may provide a “huge relief” for the corporate sector, said the Bursa Malaysia chairman. With the Celcom+Digi merger, CDB may provide a synergistic opportunity with an EBIT margin of ~27% in 2025.

Capital expenses

CelcomDigi’s management cited expects higher integration-related opex and capex in the 2023–24 forecast with capex over revenue guidance of 15–18% for the 2023 forecast (current or 2022 capex over revenue was ~13%) which might cut cash availability to free cash flow in short term (2 to 3 years).

KUALA LUMPUR (Feb 10): CGS-CIMB Securities remains positive on the completion of the Celcom-Digi (CDB) merger on Nov 30, 2022, as the firm believes the management will be able to deliver on the substantial RM8 billion net present value of cost synergies (net of integration cost).

It said the bulk of this will be via network integration (RM5.5 billion), where 6,000–7,000 sites (out of a combined 23,900) are to be decommissioned by the end of the financial year 2023, while the remaining sites are to be integrated or optimized in the next 24–36 months. Meanwhile, another RM1.1 billion/RM1.4 billion of cost synergies will be extracted from information technology (IT) integration and others.

I viewed the line sentence with NPV with my skeptical view depending on the derivation of its free cash flow calculation.

Debt load

Recent CelcomDigi Q4’22 filing under the line Borrowings and debt securities via floats, Sukuk, fixed-rate term loan, and debt securities offerings for the total amount of ~14.8 billion for the spike of ~10b addition in debt. Digi’s total debt was 4.6b based on the Q3 earnings report before the merger.

The ability to pay back debt depends on a variety of factors depending ability to generate future Revenue, EBIT, the debt amount, debt maturity level, depreciation in cash flow, cash from operations, and Capex. Consensus analysts are estimating a top line of 13b in 2023 and EBIT margins of ~23% to 27% throughout 2025, we may see higher depreciation, and reinvestment in telco infrastructure.

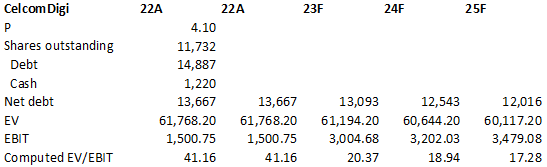

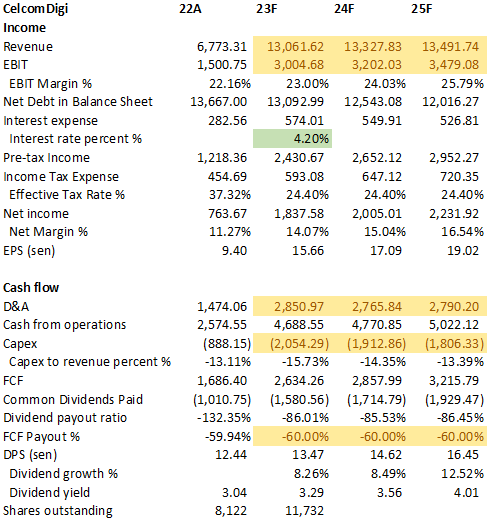

At the end of 2022, available cash is 1.2b, and with the Net debt of 13.6b, we can estimate to pay back some debt amounting to about ~13b. Based on the interest expenses rate of 4.2% (present Malaysia’s government 10-year bond stood at ~4.01%), pre-tax income we could deduce to 2,431b in 2023 and 3,033b in 2025. Free cash flow can be estimated to be about ~3.8b in 2023 before paying dividends to the shareholders. Based on the ability to pay back its debt, the Net debt over EBIT ratio in years can be deduced from 4.36 years at end of 2023 to 3.38 years in 2025.

Digi’s Net debt over EBIT ratio had been traded for an average of ~2.2 years in the last 10 years. With the recent merger, that ratio can spike up to above ~4 years as calculated above. Comparable or higher to Axiata and OCK’s average Net debt over EBIT ratio have been 5.7 and 4.3 years in the telco sector. Though the current debt load is higher than the current leverage (~4 years), I believe the load is still manageable. My preference is anything below 5 years in debt load ratio.

Valuation

At the price of 4.10, at debt and cash on year-end 2022 as tabulated above, CelcomDigi is still on the expensive side based on EV over EBIT ratio despite the forecasted data available. EV over EBIT ratio of 20x (or 25x in NTM P/E ratio) at end of 2023 looks a tad higher on the expensive side which is over 15x P/E ratio, a premium valuation. Peer comparison based on Time dotcom NTM EV/EBIT has been able to provide at 15x.

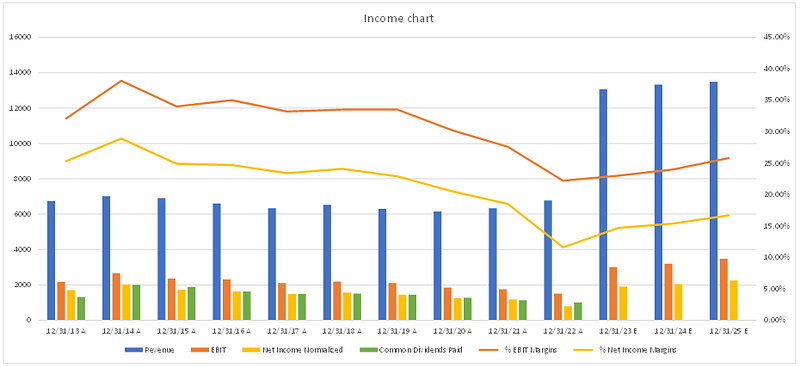

Based on Digi’s long-term 10 years trend, the Company has stagnated starting in 2014 despite the initial growth before the 2010s. Mobile penetration has stopped growing and reached to saturated market since 2014. Previous EBIT margin and Net margin can still be maintained at the healthy rate of 35% and 23% margins until 2019 before the onset of COVID-19 in 2020. The dip in the Net margin (yellow line) at end of 2022 was lower than the EBIT margin (orange line) caused by the inclusion of a one-off event. Digi’s management decided to pay dividends more than net income despite the one-time cost payment to Axiata when incorporating Celcom.

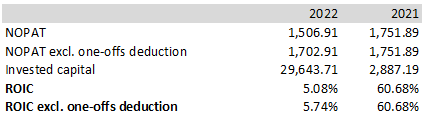

ROIC (return on invested capital) has been suppressed down to between the 5% to 6% range due to higher load debt with the merger purchasing Celcom.

The next three years’ forecast in 23F to 25F were based on analysts and TIKR (analytic software, hilted in yellow) consistent with the management expectation. I made an assumption set to an interest rate of 4.2% based on the average 10-year bond rate. With the pre-tax income and tax expense. we can deduce the net margin to 14.1% in 23F towards 16.5% in 25F.

The dividend per share (dividend payment) forecast may expect to grow towards 13 to 16 sen. I believe the FCF payout ratio could provide better prediction, compare to dividend payout, guided by the management’s capital expenses divide by revenue guidance of 15–18% in 23F to 25F.

Takeaways

Digi’s fiber and data center (enterprise) revenue had been timid although it is at the growing rate of 23% and 13% at end of the year, Q4 2022. Digi leveraged a partnership with Axiata and TM’s HSBB (Layer 3, high-speed broadband) network to deliver high-speed broadband in 2019. While Time dotcom and TM act as the first tier with investment in submarine cables as early as the 2010s which serve as the backbone of the connectivity infrastructure.

Malaysia’s MVNO was the first introduction in Asia under its Yoodo which offer 5G services on the merger under the CelcomDigi umbrella. 5G will be the key revenue driver for the industry. CelcomDigi chose Single Wholesale Network (SWN) for 5G, allowing existing MVNOs to invest their capital in developing the applications and services to drive growth. 5G may provide lower latency broadband connectivity setup for users in addition to factories, enterprises, etc. new usage model in 5G. The current 5G penetration rate has reached 50% coverage of populated areas (COPA). This may pave a way for a tailwind for future growth in the telco sector.

CGS-CIMB’s target price was set to 4.15 and RHB’s target price was 4.32 taking into account the merger’s integration cost and synergies.