{kind=link}

DeFi Loans and credit scores

Credit scores are the most important three digits that are essential to living in this world. They absolutely dominate US lending with 90% of lenders using them but that doesn’t make them good. journey with the credit scores started in Oct 2021, when I was selected for an open banking global competition. GOFC. Individually, I was captivated by the BNPL phenomenon, knocking down on the fortress of credit cards and the banks. Albeit slowly but sundry.

We, as a team, proposed an idea for Banks to use open banking APIs, to build a marketplace that will bring together the merchants and consumers, and start pushing their new credit cards, building on the idea of BNPL. One of the criteria for moving ahead in the competition was to build a functional app, which given the dearth of time MBAs have we couldn’t.

But the idea remained in my head, and I discussed it with Sen and Aditi, during our defi -blockchain class. We proposed a BNPL scheme on the blockchain, where folks who were taking loans on makerDAO, Aave, and compound can simply use this. Post-class, me and Pris worked on this project and further developed the idea, and the slide deck at the end is what we pitched to @whartoncypher.

1. HISTORY OF CREDIT SCORES:

In 1956, engineer Bill Fair teamed up with mathematician Earl Isaac to create Fair, Isaac, and Company, with the goal of creating a standardized, impartial credit scoring system. Within two years, they had begun selling their first credit scoring system. Today, that company goes by a different name: FICO.

The current FICO score system debuted in 1989 and has become the industry standard. It is a number between 300 and 850 determined by the following factors (by descending level of importance): payment history, amounts owed, length of credit history, types of credit used, and recent credit inquiries.

2. HISTORY OF CREDIT BUREAUS:

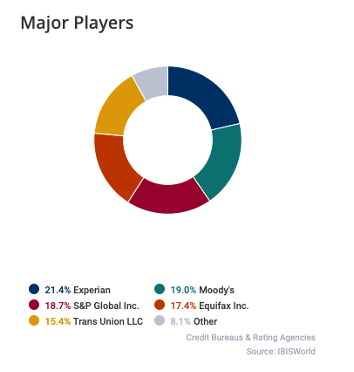

The three major credit bureaus, Experian, TransUnion, and Equifax, track your financial information to determine your credit score. Each of those companies has its own unique history.

Equifax is the oldest of the three credit bureaus, dating all the way back to 1899 when it was known as the Retail Credit Company. They were one of those early credit bureaus we mentioned above, and they would collect all manner of information about potential credit seekers, including personal details, like marital troubles or political opinions.

TransUnion was founded in 1968 as a railroad leasing organization. Railroads were not interesting enough because they immediately acquired the Credit Bureau of Cook County. Experian is the newest of the credit bureaus. It was founded in 1996.

Over the years there have been other players in the business as well, as shown below

3. LOANS IN DEFI WORLD:

With the advent of the Decentralized world, the credit scores of the real world do not work in this brave new world’, and since they do not work, we need something new (or do we?)

The decentralized finance lending platforms basically focus on offering crypto loans with a trustless approach. According to the trustless approach, users could lock their crypto assets on the lending platforms without worrying about any intermediaries. Borrowers can take DeFi loans directly from the decentralized platform through P2P lending. [1]

One of the key differences from traditional loans is the collateral needed for defi lending. The defi lenders need to have collateral in the cryptocurrency, and the loans in the Defi world are overcollateralized. There are other risks associated with DeFi, such as wrong liquidity pool estimations, compromised private keys, insufficient access control, and 51% attacks.

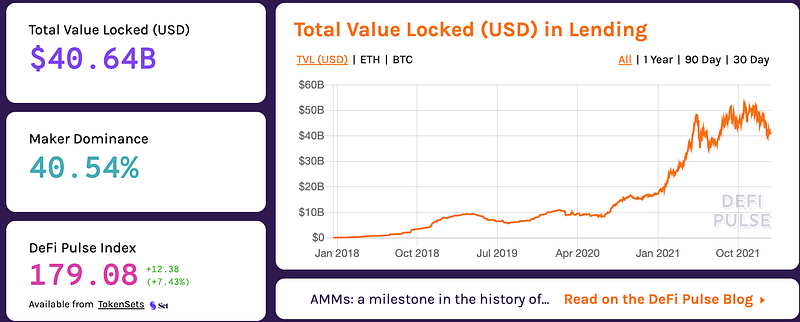

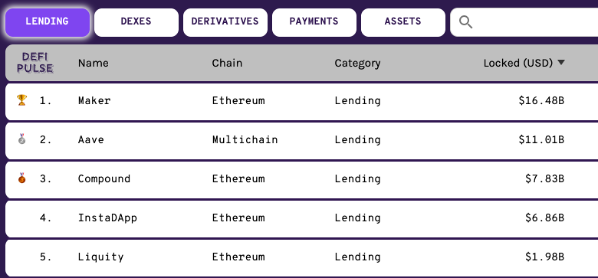

Yet the lending business has been growing and as of today stands at $40.64B, with the top five players as MakerDAO, Aave, Compound, InstaDapp, and Liquity.

4. CREDIT SCORE FOR DEFI WORLD

One of the challenges hindering mass adoption is over-collateralization in DeFi loans. Often the user ends up paying a 150–200% collateralization ratio. One of the reasons for this is the market volatility, which comes inherently with cryptocurrencies lending and borrowing.

Over the last four months, I took a course on Decentralized finance under Prof Andreas Park, learned the basics of decentralized finance, and pitched an idea based on Credit Score for defi. A month later with help of my friend, we pitched the idea to @Whartoncypher. The slide deck is linked here

https://www.slideshare.net/arunabh010/credex-credit-score-for-web-30

Most recently, we applied for the Wharton fintech accelerator and pitched this idea to them. We are open to feedback and look forward to what you people think of this?