China is not the winner of US debt crisis

5 reasons a potential default couldn’t undermine the US dollar’s standing vis-à-vis China

A possible US debt default raises concerns about its economic repercussions and broader implications for the global financial landscape. While some argue that such a default could undermine the US dollar’s dominance and America’s standing vis-à-vis China, it is important to critically examine the validity of these arguments.

This article aims to explore both sides of the debate and provide a comprehensive analysis of the potential impacts of a US debt default on global currencies and power dynamics. I argue that the recent US debt crisis would not impose a threat to the US dollar’s dominance over Chinese renminbi (RMB) for the following reasons:

1. Resilience of the US Dollar

The historical resilience of the US dollar provided its dominant status as global reserve currency. The US dollar’s liquidity, stability, and the depth of its financial markets have attracted investors worldwide. Despite economic challenges and past financial crises, the US dollar has maintained its position as the primary currency for international transactions. This suggests that the global confidence in the US dollar may not be easily displaced, even in the event of a debt default.

The RMB’s resilience is closely tied to China’s economic performance. A strong economy and stable growth provide a foundation for the RMB’s resilience. Although China’s economy has grown rapidly, it still has some challenges, including high debt levels and concerns over corporate governance, which could impact the RMB’s resilience.

The independence of central bank also matters to a country’s currency resilience. The US Federal Reserve (Fed) is known for its independent monetary policy and credibility. While the People’s Bank of China (PBOC) also plays a crucial role in managing the RMB, there are perceptions that it may have less independence compared to the Fed, which can negatively affect the market confidence of China.

2. Limited Alternatives to the US Dollar

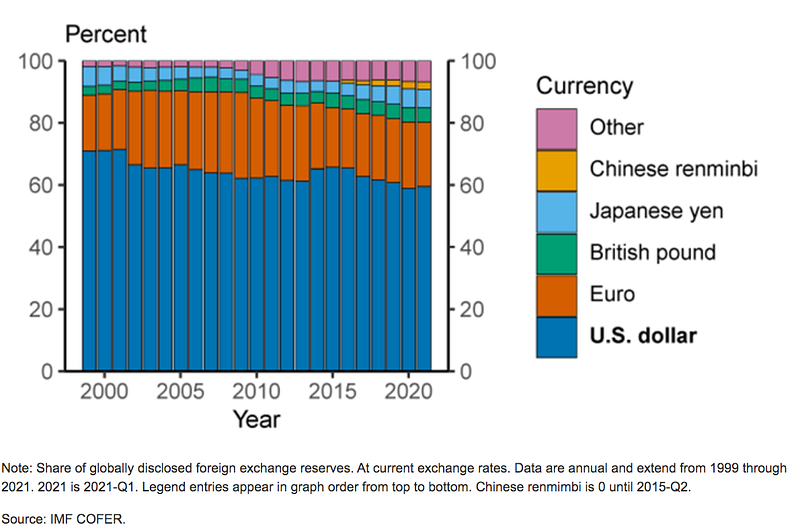

While there may be growing interest in invoicing trade in RMB, the adoption of an alternative global currency faces significant hurdles. The euro, introduced in 1999, has not surpassed the US dollar’s dominance. While the euro has weakened considerably against the US dollar in recent years, it is still practically at par with the US dollar. As of today, the US dollar remains the dominant currency in international transactions and financial markets, with the euro being dominant only in Europe.

Foreign exchange reserves from 1999 through 2021-Q1

The existing infrastructure and networks built around the US dollar would be difficult to replicate or replace swiftly. Thus, the likelihood of a rapid shift away from the US dollar as the global reserve currency may be overstated.

3. Strength of the US Financial System

Critics argue that a US debt default would strain an already fragile banking system and lead to higher interest rates. According to Moody’s Analytics’ projection,

“A default lasting even a few weeks could cause a recession comparable to that during the global financial crisis, resulting in the loss of nearly 6 million jobs and a stock market fall off of almost one-third, which could wipe out $12 trillion of household wealth.”

However, it is important to consider the resilience of the US financial system. Lessons learned from previous crises have prompted regulatory measures and safeguards that aim to strengthen the system. These reforms have made the banking system more robust, reducing the likelihood of a systemic collapse in the face of potential shocks.

While risks persist, it is not necessarily an inevitable outcome that a debt default would destabilize the entire financial system.

4. China’s Financial Constraints

While China’s rise as a global economic power is evident, there are significant constraints that limit its ability to assert dominance in international finance. Capital controls, restrictions on capital movement, and the relative underdevelopment of domestic financial markets present challenges for China. According to an IMF report,

“China faces serious domestic challenges such as an aging population, a rural-urban divide, an underdeveloped financial system, insufficient innovation, and reliance on carbon-based energy sources.”

Concerns about executive behavior, transparency, and governance continue to raise questions about the international community’s confidence in fully embracing the Chinese financial system.

These factors suggest that China may face obstacles in capitalizing on a US debt default to enhance its own standing.

5. Political and Strategic Considerations

The assumption that a US debt default would provide China with an opportunity to seize a leadership role in international finance is premature, as geopolitical dynamics and potential conflicts of interest may temper China’s ability to project influence unidirectionally.

It is important to note that China’s economic growth has certainly been influenced by its relationship with the United States. The financial interdependence between the two economies has helped fund China’s infrastructure projects, stimulate domestic consumption, and support investment in various sectors of the economy.

Though China’s rise as a global power has generated apprehension among some nations, particularly regarding its non-Western, nondemocratic model, political tensions and disagreements on global issues, such as responses to conflicts or human rights concerns, could impact China’s ability to effectively leverage a US debt default to its advantage.

Conclusion

The potential impacts of a US debt default on global currencies and power dynamics are complex and multifaceted. While arguments have been made about the erosion of US dollar dominance and the subsequent rise of the Chinese RMB, it is crucial to consider the factors that highlight the resilience of the US dollar, limited alternatives, the strength of the US financial system, China’s own financial constraints, and broader political and strategic factors.

Nobel economist Paul Krugman stated that

“the dominance of the US dollar in global markets isn’t at risk unless the US defaults on its debt, an event that would dent confidence in the greenback.”

Therefore, the recent US debt crisis would not pose a significant threat to the US dollar’s dominance over Chinese renminbi (RMB), as along as the Democrats and Republicans could eventually reach an agreement on debt ceiling and solve the issue.