Calculate any Option Greek using the Black Scholes Formula in Python

Inputs in Black-Scholes Option Pricing Model Formula

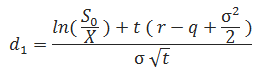

- S0 = underlying price

- X = strike price

- σ = volatility

- r = continuously compounded risk-free interest rate

- q = continuously compounded dividend yield

- t = time to expiration

For,

- σ = Volatility = India VIX has been taken.

- r = 10% (As per NSE Website, it is fixed.)

- q = 0.00% (Assumed No Dividend)

Note: In many resources, you can find different symbols for some of these parameters in the Black Scholes Formula. For example,

- The strike price is often denoted

K(Here it isX). - The underlying price is often denoted

S(without the zero) - Time to expiration is often denoted

T – t(difference between expiration and now).

In the original Black and Scholes paper (The Pricing of Options and Corporate Liabilities, 1973) the parameters were denoted x (underlying price), c (strike price), v (volatility), r (interest rate), and t* — t (time to expiration) in Black Scholes Formula. The dividend yield was only added by Merton in Theory of Rational Option Pricing, 1973.

Python Code

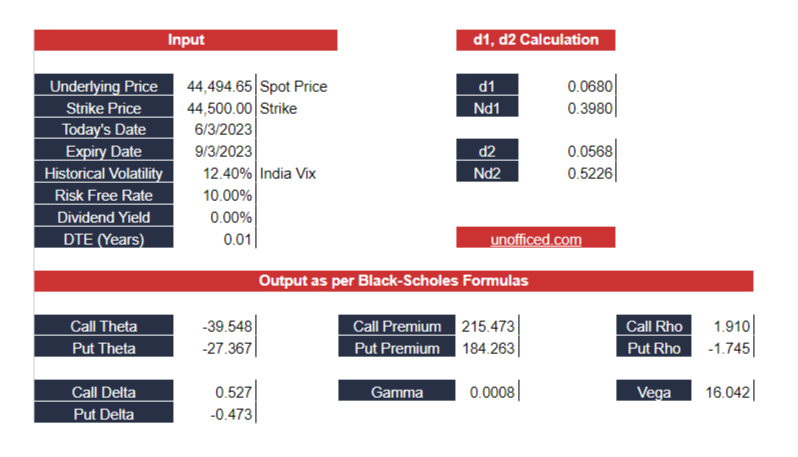

This Python code patch is written for the NSEPython Library first time. It will match with Zerodha’s Black Scholes Calculator perfectly.

import math

from scipy.stats import norm

def black_scholes_dexter(S0,X,t,σ="",r=10,q=0.0,td=365):

if(σ==""):σ =indiavix()

S0,X,σ,r,q,t = float(S0),float(X),float(σ/100),float(r/100),float(q/100),float(t/td)

#https://unofficed.com/black-scholes-model-options-calculator-google-sheet/

d1 = (math.log(S0/X)+(r-q+0.5*σ**2)*t)/(σ*math.sqrt(t))

#stackoverflow.com/questions/34258537/python-typeerror-unsupported-operand-types-for-float-and-int

#stackoverflow.com/questions/809362/how-to-calculate-cumulative-normal-distribution

Nd1 = (math.exp((-d1**2)/2))/math.sqrt(2*math.pi)

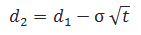

d2 = d1-σ*math.sqrt(t)

Nd2 = norm.cdf(d2)

call_theta =(-((S0*σ*math.exp(-q*t))/(2*math.sqrt(t))*(1/(math.sqrt(2*math.pi)))*math.exp(-(d1*d1)/2))-(r*X*math.exp(-r*t)*norm.cdf(d2))+(q*math.exp(-q*t)*S0*norm.cdf(d1)))/td

put_theta =(-((S0*σ*math.exp(-q*t))/(2*math.sqrt(t))*(1/(math.sqrt(2*math.pi)))*math.exp(-(d1*d1)/2))+(r*X*math.exp(-r*t)*norm.cdf(-d2))-(q*math.exp(-q*t)*S0*norm.cdf(-d1)))/td

call_premium =math.exp(-q*t)*S0*norm.cdf(d1)-X*math.exp(-r*t)*norm.cdf(d1-σ*math.sqrt(t))

put_premium =X*math.exp(-r*t)*norm.cdf(-d2)-math.exp(-q*t)*S0*norm.cdf(-d1)

call_delta =math.exp(-q*t)*norm.cdf(d1)

put_delta =math.exp(-q*t)*(norm.cdf(d1)-1)

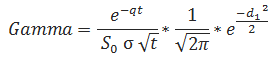

gamma =(math.exp(-r*t)/(S0*σ*math.sqrt(t)))*(1/(math.sqrt(2*math.pi)))*math.exp(-(d1*d1)/2)

vega = ((1/100)*S0*math.exp(-r*t)*math.sqrt(t))*(1/(math.sqrt(2*math.pi))*math.exp(-(d1*d1)/2))

call_rho =(1/100)*X*t*math.exp(-r*t)*norm.cdf(d2)

put_rho =(-1/100)*X*t*math.exp(-r*t)*norm.cdf(-d2)

return call_theta,put_theta,call_premium,put_premium,call_delta,put_delta,gamma,vega,call_rho,put_rhoUsage

S0 = 34950.60

X = 35000.00

σ = 14.72

t = 3

call_theta,put_theta,call_premium,put_premium,call_delta,put_delta,gamma,vega,call_rho,put_rho=black_scholes_dexter(S0,X,t,σ="",r=10,q=0.0,td=365)

print(call_theta)

print(put_theta)

print(call_premium)

print(put_premium)

print(call_delta)

print(put_delta)

print(gamma)

print(vega)

print(call_rho)

print(put_rho)Output

-35.57594968706057

-25.994786756764814

175.92468507293597

196.56938065246504

0.4850057898780081

-0.514994210121992

0.0008543132102275919

12.621618527502404

1.378793315723619

-1.495555563365108Call and Put Option Price Formulas

Call option C and put option P Prices are calculated using the following formulas:

where N(x) is the standard normal cumulative distribution function.

The formulas for d1 and d2 are:

Original Black-Scholes vs. Merton’s Formulas

In the original Black-Scholes model, which doesn’t account for dividends, the equations are the same as above except:

- There is just

S0in place ofS0 e-qt - There is no

qin the formula ford1

Therefore, if the dividend yield is zero, then e-qt = 1 and the models are identical.

Black-Scholes Formulas for Option Greeks

Delta

Theta

… where T is the number of days per year (calendar or trading days, depending on what you are using).

Gamma

Vega

Rho