If You’re Gen X And Don’t Own A Home, You’re Up Against A Huge Life Decision

$200,000 in cash, $166,000 in interest — this Is just ridiculous

As with the data on how little house you get for your money these days, the housing numbers we detail today will — yes — shock you. Or at least I think they should.

They give you something to think about no matter your situation.

But specifically if —

- You don’t own a home.

- You don’t have an otherwise amazing and sustainable housing situation.

- Times two if one or both of the above apply and you’re Generation X annnnd— like me — in that somewhat uncomfortable middle section of life.

All three bullet points describe me.

So I have a huge life decision on my plate. A decision I just told my daughter about. As I prepared to tell her — absolutely — I was nervous. Because, although it’s necessary and even exciting to make big decisions in response to the housing crisis, it isn’t easy, especially if you care about how friends, family and others might react.

In this article, we survey this potentially dismal landscape and consider refreshingly positive ways to handle it. Including how I’m handling it.

Because no matter how bad things are (yes, they’re bad) or how much helplessly worse some people want to make them seem (yes, some people love to do this), there’s almost always a (better) way out. Particularly if you have a choice in the matter.

But first, if it isn’t obvious already, why do so many Gen Xers and others — maybe you — face such an important and pivotal life decision?

Entrepreneur Austen Allred recently ran the math on how much a 30-year home loan costs you —

Allred explained that if you purchase a $1 million house with a $200,000 down payment and get an $800,000 mortgage at a 7% interest rate, in the first three years you’ll be paying $193,000.

But because of the high-interest rate, a significant portion of your payments would go toward interest, leaving a substantial amount still owed on the principal.

“After those $193,000 of payments your $800,000 mortgage is now at $774,500,” he said. “You paid $166,000 in interest, $25,500 in principal.”

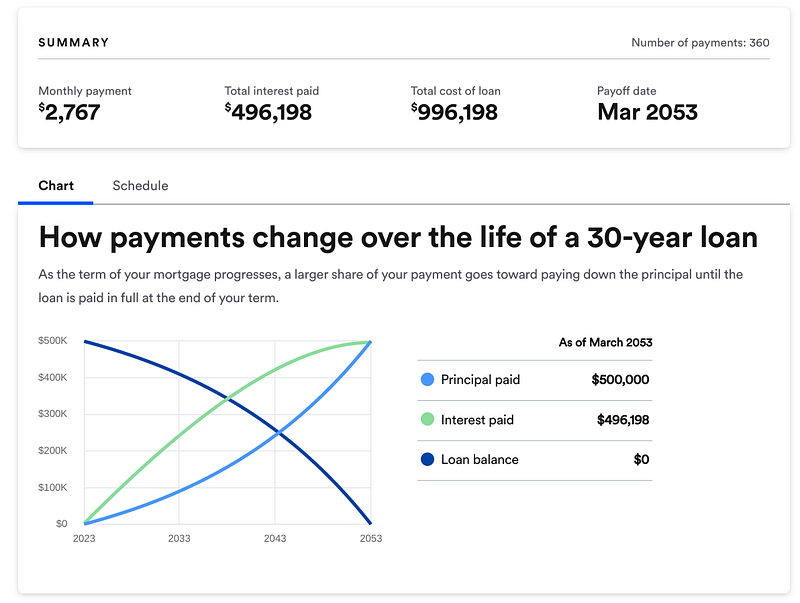

Not long ago — for the life of me I can’t find the link to the Medium article — I ran similar numbers. However, I did find the screenshot I used.

It’s not just the stuff banks and mortgage lenders don’t like to advertise. The insane amount of interest you’ll pay on the loans they give out.

It’s that you need serious financial strength to secure this loan and come up with six figures for a down payment in the first place.

Make no mistake — taking on a mortgage in America today is life changing. And not in the oh, look, you made it kind of way it used to be. It can give you a one-way ride on the personal financial hamster wheel, otherwise known as the grind.

Even if you scale it back — like we did the other day — to the median price of a home in America, it doesn’t look good —

The median price of a house nationally is $440,000, as of July 2023. This is only $9,000 lower than the all-time high set in June 2022.

Let’s say you can put 10% down. That’s $44,000 up front, just for the down payment. At a 7% interest rate on a 30-year mortgage, you’re looking at a monthly payment of about $3,400, including property taxes and insurance. To afford this payment — using the don’t spend more than 30% of your income on housing standard — you need to earn roughly $11,333 a month, or approximately $136,000 a year.

In fact, it looks bad. Shockingly, if not terrifyingly bad.

With the interest rate on a 30-year mortgage now at roughly 7.34% (as of August 16, 2023), it has only gotten worse on all of these calculations. In just a matter of days!

You know the problem. We identify and illustrate it frequently.

So — if you’re impacted by some or all of this — what are you going to do?

You have to make a decision and make one quick.

Whether you’re one of those people sitting on the sidelines waiting for things to cool down so you can buy a house or there’s no way you can touch home ownership in most of America to begin with.

If you’re sitting on the sidelines, you’re likely waiting for interest rates to drop before you make a housing-related move.

But here’s the deal — amid a low supply of houses on the market and prices near all-time highs nationally (and still in record territory in tons of cities), expect prices to skyrocket as rates drop and buyers flood the market. So what you might save in interest likely won’t offset the increased cost of the house you want to buy.

Maybe more importantly — or, at least, less of a good problem to have — what if you’re in the there’s no way you can buy a house in most of America regardless group?

Maybe you’re like me —

- You don’t view home ownership as something you must do.

- But you’re all for it if it makes you better off financially today and for the duration than you were yesterday.

- You refuse to stretch yourself financially and/or work to the extent and at the type of job you would need to be able to afford a home in the relatively expensive parts of 2023 America.

- You don’t want to turn 50, 55, 60 or whatever with an out-sized rent or mortgage payment. Hell, you don’t want either at the moment if you’re younger or older than that.

- You want a soft and easy life, best attained through a combination of a low cost of living, work you enjoy doing that pays decent or better money and a physical habitat that provides a high and desirable quality of life.

If this or something like it describes you, welcome to the turning point of your life. You have some decisions to make.

Just this week, I told my almost 20-year old daughter that me and my partner plan to move to Spain within a year or two. I basically covered each of the above bullet points with her, letting her know that we have a fighting chance — maybe even a good one — to buy a nice apartment in the type of urban setting we love for meaningfully less than 300,000 euros.

Ultimately, we’re doing this to ensure we’re in the best position possible as we head into act two of our life.

I was nervous about telling my daughter. Because as much as it’s a no-brainer decision to make, it’s still a big one. Leaving family isn’t easy. Of course, you’ll miss them, but there’s also concern over how they might react.

At the same time, you have no choice but to look at the bright side. Because there’s always another side to the overly emotional and dramatic. And it’s often bright. The bright side being that you’re doing what’s best for you and keeping life vibrant and fresh by inviting new challenges and experiences.

I’m more than thrilled to make Spain my home with my partner and have our kids visit us there. It’s an opportunity for growth — for us and our respective daughters— as well as a new chapter in our relationships with them.

No matter the housing-related, life decision you end up making, it’s going to be better to approach it kind of, sort of like this than to lead with emotion and everything that could possibly go wrong.

If you live up the street or a 40-minute drive from Mom and Dad, it might be life-altering for them and/or you to move to a different city or across the country or world, but …

If you really love the city you’re enjoying life in today, but it is or will get uncomfortably expensive, it might be difficult to leave, but …

Insert your if/but here …

However you categorize then slice it —

It’s going to be more life-altering and difficult to be something like:

- Fifty years old, sitting on the couch in the living room of your $2,500-a-month apartment or in year 15 of a $4,500-a-month, 30-year mortgage.

- Living with the reality that you need to come up with that amount of money (or more) every single month for the rest of your life or another 15 years before you pay for anything else. That’s an easy-bake recipe for having no life.

So —

Determine what your thing is with respect to the ideal place to live out the rest of your life.

Figure out how to end up in that type of environment with the lowest housing payment possible today. And one you can bring lower sooner rather than later.

This might be a smaller city or suburb. It might be the countryside. Maybe it’s another country entirely.

Whatever it is — the time to start planning and acting is now. Because this housing crisis will only get worse.

If you’re Gen X and you don’t own a home, there’s added urgency. But if you’re younger and prefer not to deal with the rigors of the runaway American dream, you’ll be doing yourself a favor by planning and acting now, rather than waiting till your, say, 35-plus.

In forthcoming Medium articles, we’ll detail concrete ways — based on these broad ideas — to make it all happen, address how and why some of us Gen Xers got here and how we feel about it.

To receive a notification each time I publish a Medium article, go here. In future articles, we’ll go more in-depth on the things I touched on today.

To subscribe to my Never Retire: Living The Semi-Retired Life newsletter where I chronicle my big decisions on lifestyle, housing and cost of living, which includes moving to Spain sooner rather than later, go here.

This article is for informational purposes only. It should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any major financial decisions.