Buy. Borrow. Die — How the Rich stay rich

Learning to invest like the 1%

You might have heard of the saying wealth is control by the hands of a few. In this post, I will present to you the way the rich remains rich and how we can apply the same principle to increase our net worth.

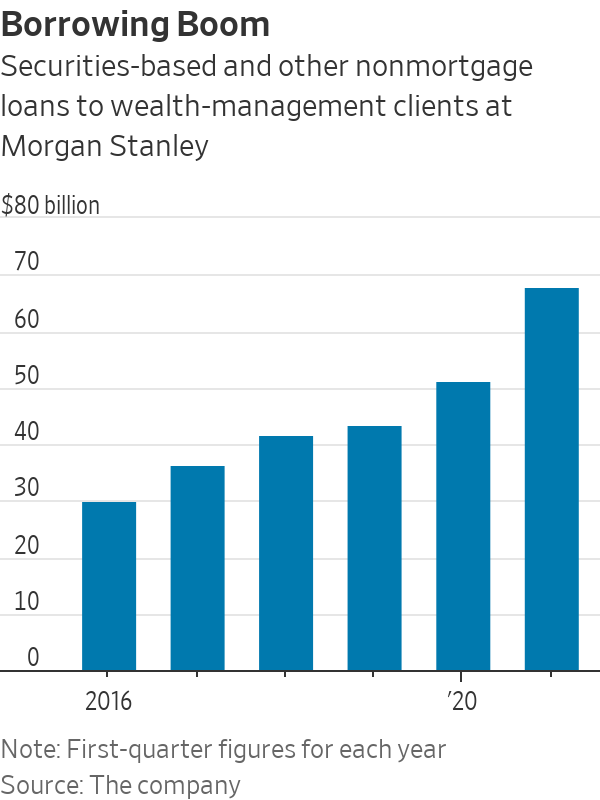

Morgan Stanley reported that the wealth management clients has $68.1 billions of security based (non-mortgage) loans. This number is twice as much as it was in 2016. Bank of America reported that they have $62.4 billions home security based loans. That poses an interesting question: Why are the wealthy borrowing money?

If they already have and make a lot of money, why do they need to borrow money? The answer to that question is fascinating, a technique that has allowed them to control this wealth without ever selling their wealth. This is how generational wealth is passed down and how most powerful wealthy families of America are created. Fortunately, this technique can be applied to everyone. You do not need to be rich to take a profit from knowing this information.

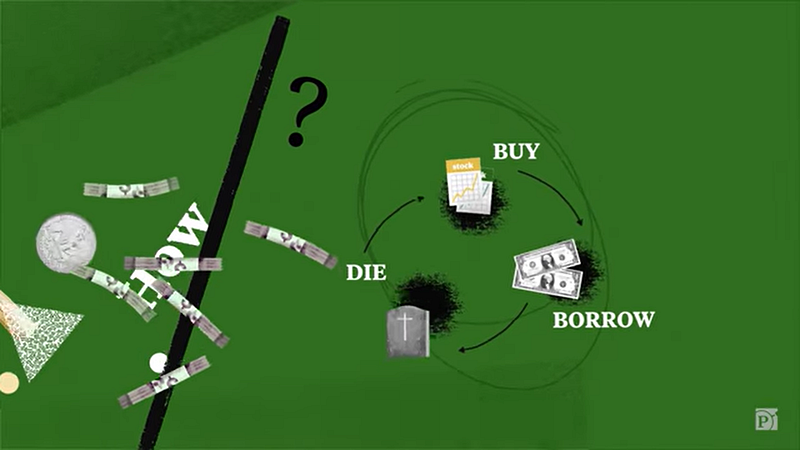

The technique is described in three simple steps: “Buy. Borrow. Die.” This phrase was created by Edward McCaffery, a tax law professor at the University of Southern California Law School to describe how the Rich has hacked the American tax system.

The basic premise is that the Rich buy an asset such as a stock or real estate, borrow against the asset for a low interest rate instead of selling it. Finally, they die and the estate goes to their heirs or beneficiaries.

When I started investing, after I pick the asset to buy, my next question often is when should I sell it. We often think to hold on to these asset for a few years, when we’re ready to retire as millionaires, we would sell off these investment to pay for our lifestyles. That is the traditional path to wealth that I learned as a beginner investor.

On the contrary, that is not how real wealth is control in this world. This technique helps you think like the rich.

Step 1: Buy an Asset

In traditional finance language, this phase is called the accumulation phase. The popular advice follows this sequence: go to school, get a degree, a high-paying job, save your money, buy up assets. Most of us will spend the majority of our lives in this phase.

Now let’s talk about all the different assets we can buy and what they can do for us. I have broken them down to three most popular assets: real estate, stocks, and crypto.

Real estate:

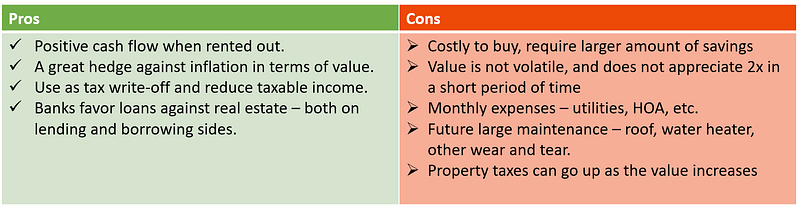

For most of us, owning a house might not be best investment because of the associated costs beyond mortgage — property taxes, insurance, utilities and other monthly expenses. However, using this strategy, you can transform your home from a liability (costing you money) to an asset (making you money) whereas a liability is something that cost us money.

Many wealthy people, net worth of hundred of millions of dollars, can live tax-free by simply borrowing against their real estate.

For example, they own apartment buildings and office buildings. They will borrow against these assets, refinance, pull out the money tax-free and live off that money while the buildings still generate positive cash flow. This is called maximizing loan to value — LTV.

They never incurred capital gain tax because they never sold the building. They were simply using it as an asset to borrow against, aka collateral.

Pros and Cons:

Stock:

You can think about stock and the exact same way. I have accumulated about $25,000 in Robinhood since 2018, which is a taxable account. Adopting the rich mindset, I hold this investment long term thinking that it will become much bigger. While holding, I can earn dividends from dividend stocks or I can borrow against this holding.

Crypto:

The same logic applies to my crypto investments. I buy blue chip stable cryptocurrencies such as Bitcoin and Ethereum, anticipating that it will worth millions a couple decades from now. I can also again — borrow against them.

The buy phase in the most important one and the takeaway here is the rich do not sell, they accumulate. It is the hardest phase to do, it’s where the sayings your first million is the hardest to come from. It takes the longest. — Andrei Jikh (Finance Youtuber)

Once you do reach this phase, things get really interesting because in the next phase instead of selling that asset and getting hit with capital gain tax, the rich will just borrow money.

Step 2: Borrow against the asset

The next step is exactly as it sounds — to borrow against the asset from step 1, effectively collateralizing them.

Stocks:

I can do this through SBLOC (securities-back line of credit). This allows the asset holder (aka my stock portfolio) to access 50% to 100% of its cash value at a special low interest rate. The loan is using the asset as collateral, which means the asset will get liquidated (sold) to pay for the loan in a catastrophic event.

Example: I’m in a cash crunch. I need cash and have none available. Let’s pretend the only assets I have is my portfolio in M1 Finance account.

Instead of selling the stocks or ETFs that I have, I can use this strategy to borrow against my asset. I can borrow up to 35% of the value of my portfolio at 2% interest. This is free money based on current inflation rate (7%).

The rich uses asset debt, and the poor uses credit-card debt. Credit card debt has high interest rate because the banks are taking a huge amount of risk if we default on our loan. They can ruin our credits but they get absolutely nothing from us if we decide not to pay.

Interest-rate Arbitrage

Instead, the rich takes advantage of asset-backed loans with a much lower interest rate and practice interest-rate arbitrage. The concept refers to the practice of borrowing money at a lower interest rate than the rate at which our stocks and other investments will grow by.

Example: You are investing $100,000 at your brokerage, and earning 10% per year. With SBLOC, you can borrow up to $100,000 at a special rate (2% for this example). You take this money and invest all of it it. Now you have invested a total of $200,000.

Interest payment = 2%* $100,000 = $2,000

Additional earning = 10% * $100,000 = $10,000

Extra earning (after interest) = $10,000- $2,000 = $8,000

This strategy, multiplied by infinity, will create phenomenal amount of wealth, worth millions of dollars.

However, there is a huge downside to this strategy. If something horrible happens like the COVID-19 pandemic, and the value of your portfolio goes down by half. You still owe the full value of your portfolio before it crashed. The value of your loan does not fluctuate in relation to the value of your asset. A lot of brokers have margin minimum, they will call in your loan and you can lose everything. An example of disastrous over-leveraging was Bill Hwang of Archegos Capital Management, who lost billions of dollars in March 2021.

This technique can be very powerful when used carefully because it will return a higher interest rate then the interest rate of your loan.

Real estate:

A similar technique is called HELOC (Home Equity Line of Credit). If you own a certain amount of equity in your house, the bank might give you a loan at a low interest rate. Your HELOC loan is backed by your house equity, and if you default, they will take away your house.

Example: You have $50,000 of equity in your house. You get a HELOC loan for $50,000 at an interest rate of 2%. You then go and pay off higher interest rate debts such as car loan and credit cards, effectively earning guarantee return by the difference of interest rates.

This technique is very helpful because it is available for anyone to use at any income level. Bankers love real estate-backed loan, even more than security-backed loan. Stocks fluctuate and are generally harder to predict value in the future. In comparisons, real estate is much more stable in value.

Crypto:

You can now borrow against your cryptocurrency holdings. Crypto companies such as BlockFi have one of the best incentives in the world — low interest rates and qualifications.

The biggest downside to crypto backed loan is the volatility of crypto. Cryptocurrency goes up and down in value, and your money can get a margin call away and you can lose everything. As always, the higher the risk, the higher the reward.

Your interest rate really depends on how much money you can give the banks. The more money you have, the more incentive they have to lend to you. Do your Google search on the rates and incentives that are offered by banks and other platforms.

Step 3: Die and pass it on

The step is pretty self-explanatory but that is a catch and this is what keep the rich generationally rich. When you die, your estate goes to your beneficiaries or heirs. The loan can be paid of by selling the assets the you borrowed against previously.

Many rich families established a trust, so they can pass on their wealth at a stepped up cost basis.

Example: Say you bought a $1 million building 20 years ago. Now it is valued at $2.5 million. It can be borrowed against or sold at that valuation. Your heirs will NOT realize any capital gain tax because they are getting it at the new $2.5 million cost basis.

Real estate:

Another popular tax strategy used by real estate developers is the 1031 Exchange Rule. The rule dictates that if you sell an investment property and find a like and equal or greater value property within a specific time frame, you can forego the capital gain tax on the original sale of your property. Hence, developers can avoid paying capital gain taxes repeatedly until they pass away.

Stocks:

Say you bought an ETF (publicly traded index fund) with a cost basis of $10 in 2010, by the time you pass away (hopefully like 20–30 years from now) your ETF worth $1000 per share.

If your heir chooses to sell the ETF at $1000 today, they will pay no capital gain tax. They have no gain since they receive the ETF at cost basis of $1000 per share.

They get the money from the sale, they buy whatever they want, which then they can pay off the loan. Or they can borrow and not pay it off and then die. And the cycle continues.

Key Takeaways:

You might ask why isn’t everybody doing these steps and loaded with debts as they maximize their Loan-to-value ratio on all their assets? The answer is it depends. Ask yourself this:

How much money do I have to make in order for this to make sense for me to do?

Traditional finance can be sound advice, and you generally should take these steps first before you consider doing this strategy.

- Step 1: Build your emergency fund 3–6 months.

- Step 2: Open up your 401K with your company and get it up to the company match.

- Step 3: Max out your Roth IRA.

- Step 4: Max out your company 401K.

- Step 5: Open up a taxable account. This will be the money you use to borrow against.

Another thing to remember is leverage can be a double-edged sword. Use it wisely based on your financial situation.

On a HELOC loan, your number needs to work for the bank in order to give you the loan. Similarly, you can get margin call away from your stock portfolio when stocks are falling.

I will end this post by quoting Andrei Jikh, as he cleverly sums up the mindset for this strategy.

Many people learn about this, and get really angry at rich people. At the end of the day, you can’t hate the players, you got to hate the game. But instead of hating the game, just learn the game rules, learn how to play and learn to love the game.

Thank you for reading my post, and I hope you found the content insightful as you plan your personal finance journey. If you find its helpful, please follow me and check out my other posts for more investing tips and self-improvement tips. As always, have a fulfilled day as you go out there and be your best self.