Born into Debt: The American Variety of Poverty

We understand poverty by degrees like the winter cold. When my husband, a Nigerian, says he was “born with nothing,” he means he was a co-wife’s son treated poorly by his siblings. Eventually, he and his mother would leave his father’s compound and move back to her home village. He would grow up in poor but adequate housing, supported by a Mom who sold what she could in the town. And upon her death, in his young adult life, he would be left with millions of Naira in microfinance debt at a crippling interest rate, the result of his choosing to borrow money to try and save her life.

On a scale of ice-age-frozen to hot summer, this is a mild snow. We have to consider, of course, children who are born to be sold, children who are born and thrown away, children who are orphaned and living in slums. These children run the risk of never running into hope (even by accident). So, to keep perspective, the children who may never have hope are residents in the coldest winter ever.

American Poverty

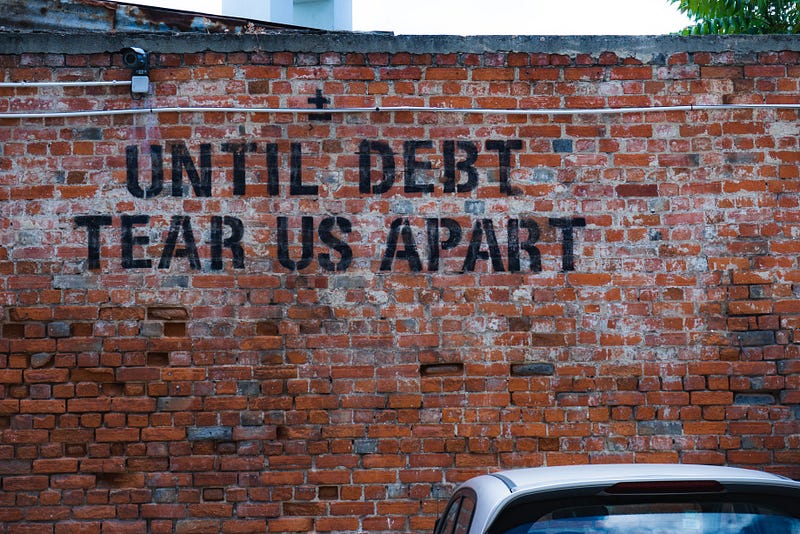

American poverty is not like the orphan’s suffering or the faithful son’s hospital bills. It appears to be quite warm and sunny from the outside, so sunny that people give up their lives in other nations for a chance to achieve the American Dream: stability. When they get here, they are too often surprised by an ice-cold fact. Hardly anybody owns anything. The whole country is suffocating in debt.

Hardly anybody owns anything. The whole country is suffocating in debt.

Rented and Financed Housing

The average American child is born into a household where two adults work (or one adult works two or more jobs) to pay for housing. The housing cost is often more than 50% of the income earned each month. How can this be in such a wealthy nation? We are not raising our families on compounds.

About 60% of Americans have no will or estate plan for surviving family members. Properties are not being passed down to children for their children and so on. So, a body has to have a place to live… a place from which to commute to that stable American job. A place to live means a rental, a mortgage, or a subsidized property in government housing.

Essentially, you don’t own your living space for 15–30 years (at the least).

The average American doesn’t own their living space for at least 15–30 years.

Financed Transportaion

The US public transport system is limited and practically absent in rural communities. That means that Americans need cars (to commute to those stable jobs).

Money, again, is a problem because 70% of Americans have less than $1000 saved. In order to get to work regularly, Joe or Jean might finance the cheapest reliable ride ($5–8 thousand certified used, $10–12 thousand new) and pay for top tier insurance to satisfy the lender’s lien requirements.

This would mean not owning the car you drive for 5–7 years, and also paying the recurring premium insurance debt. In 2019, the average American car loan balance was a whopping $18,500. 43% of Americans are in debt because of their car troubles.

Financed Communications

Cell phones can be purchased at dollar stores now for $20–40. A $30-40 prepaid card can pay for a month of talk and text, and that’s pretty outstanding. The problem is that phones don’t just make calls and receive texts now. They house the apps that monitor our health, put us in contact with our employers, keep us connected (literally) to our friends, and deliver our freelance work paystubs. The cell phone houses everything.

The cheaper phones don’t do everything well. Because the phone companies know that most of us can’t afford the better phones (but we need the better phones, apparently) they create finance opportunities where phone costs can be divided by 12 or 24 months with interest. Over 40% of America’s smartphone users took the financing option in 2018.

You can buy that $1,000 iPhone or Samsung Galaxy device, but you insure it too because you know you won’t really own it for 1–2 years. The same is true for phones in the $250–300 range. Without fluid, disposable income, even a $250 phone purchase is too much to cover at once.

Without fluid, disposable income, even a $250 phone purchase is too much to cover at once.

That doesn’t even take into account that the average American pays over $100 per month for cell phone service.

Rented or Financed Appliances

Yes. In America we can pop over to a Habitat for Humanity shop or thrift store and furnish a whole house. There are great discount stores where assemble-upon-arrival furniture can be purchased for big savings. You can even go online and order items according to type and price, one item at a time.

But sometimes the washing machine breaks and the warranty is finished. The stove goes out, suddenly. An electric pole falls in the yard and has to be replaced.

You can actually anticipate these emergencies because appliances don’t last forever, but the average American doesn’t have an emergency fund set aside for appliance replacements or home repairs. In 2018, less than 30% of Americans had a sufficient emergency savings fund. So, what do we do?

The average American doesn’t have an emergency fund set aside for appliance replacements or home repairs.

We finance it! There are stores that offer financing opportunities for appliances. With excellent credit, you might get a few interest-free months, but that still means you don’t own your washer or stove for about a year and six months.

And if major incidents occur on your property — pole down, weather damage, minor fire — there are always high interest cash advance (payday) loans to borrow quick money against money you haven’t earned yet. About 12 million Americans are trapped in payday loan cycles with interest that totals over 400% each year.

Financed Education and Training

This is a huge one. Americans owe $1.7 trillion in school debt, and almost 70% of college students borrow an average $30,000 to complete their education.

Why is this happening? Higher paying careers often require a minimum amount of education to start (academic or vocational). Then, if you want more money or more opportunity, you have to complete more schooling. The home that can’t replace a washing machine certainly cannot afford $1000-per-class coursework.

In the end, many Americans never “own" their careers. Until student loans are paid, every disposable dollar or salary increase should go to education financiers. Can we keep up with that? No. More than 1 million student loans go into default each year.

In the end, many Americans never “own” their careers.

A Different Winter Altogether

It looks cozy. It seems like the American Dream is alive and well. We are driving nice cars, living in good homes (according to world standards), enjoying flourishing careers, upgrading our phones every year, and enjoying high-end appliances. But in the end, we die and leave our children with more debt than assets.

They have to take out student loans. They have to finance cars. They have to rent or mortgage housing. They borrow against their paychecks in emergencies. The cycle continues.

How Do We Stop This?

I have no idea. After all, I’m an American also born into debt. I know that if I sell my home and move my family into an RV or a tiny home, I can end the debt cycle. That would potentially mean no property for my children to inherit.

I could lower my communications cost, but I need upper tier internet speeds for my online work (my primary income). I often find myself writing (my secondary income) on my cell phone early in the morning while the house is asleep.

I could get rid of my car and buy a $1200 used ride, but there is one car to three adults here. Two of us commute to work. We need a reliable vehicle to maintain our income.

I guess my husband and son could go finance their own cars, but that would just continue the cycle.

Good thing I got out of the payday loan trap in 2016.