Boomers: The Do-Nothing Generation

Wait! What! Oh, it really isn’t what it sounds like.

Many years ago, I came across a news article about how the Boomer Generation had the nickname “The Do Nothing” generation. The headline made me read further as it insulted me a little bit. As you may be able to tell now, I am a boomer.

The story behind the headline

As boomers, we grew up in a very different world than it is today. We could run around outside by ourselves from morning until dark. Ride our bicycles into other towns miles away. We had to make our own fun as we didn’t have all the variety of things to do that is here today.

As we grew up to be adults as it was still a fairly simple world. And then everything changes as time went on.

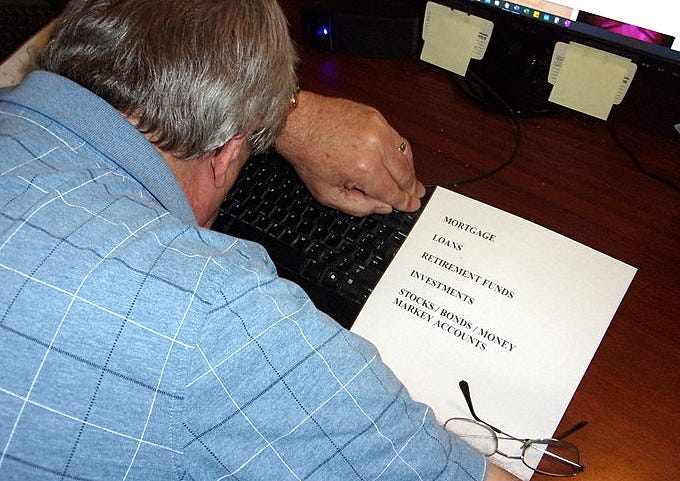

Mortgages

When you wanted to buy a house, you were looking at a 15-year mortgage or a 30-year mortgage and that was fine. As time went on there were dozens of new types of mortgages such as fixed rate, Adjustable-Rate Mortgage (ARM), balloon, FHA, VA, and on and on. There was pressure to change the old-fashioned mortgages we had to the new types of mortgages.

It was so confusing to learn the differences that — you guessed it — we “did nothing”.

Car and Personal Loans

The same thing occurred with car loans. There was one rate that was assigned to the car loan. It may have been 12%, but cars may have only been $2,000 to $3,000 so it didn’t break you. Now there are many types of car loans.

You guessed it again: It was so confusing to learn the differences, we “did nothing”.

Investments

When we wanted to invest money, we usually went to the bank or a broker. Back then you may get CD (certificates of deposit) vehicles for 10%, not 1%, or sometimes nationwide a 3% today.

When you wanted to invest in the stock market, you bought stocks like Coca-Cola, DuPont, Railroads, etc., and just held them for years. And if you held them like for years, it would pay off big time. Now when you want to invest, there are stocks (but Nasdaq, S&P 500, or Dow Jones), money market funds, options, annuities, etc., available for the everyday investor.

So, we kept our stocks and once again did nothing. (are you seeing a pattern?)

Retirement funds

If you were lucky, your job had a pension. You did not have to do anything as the fund was handled for you. For those of us without pensions, you could open an IRA (Individual Retirement Account). Simple. You opened an account and could put a limited percentage of your salary into the IRA.

Better, yet there were now 401K plans through your workplace. Again. You put a percentage of your pay into the fund, but the company would usually match a percentage of their dollars to add to yours. All automatic.

But wait. Suddenly, there were many options on where to put your money in the 401K or IRA. You could not research the many options and use the one most suited to your lifestyle.

But this was already working fine, why would I confuse myself — I’ll leave it where it is and “do nothing.”

See, it really wasn’t what it sounded like

We really didn’t “do nothing”. It was that we just left what we considered well enough alone.

I for one feel better now about being part of the Do-Nothing Generation.