Automate Your Iron Butterfly Strategy Using Python: A Step-by-Step Guide

Options trading offers a wide range of strategies for traders to capitalize on various market conditions. One such strategy that is favored by experienced traders is the Iron Butterfly. The Iron Butterfly is a neutral options strategy that involves selling an out-of-the-money (OTM) call and put option, while simultaneously buying a further OTM call and put option with the same expiration date. This results in a “butterfly” shaped payoff diagram that can generate profits in a range-bound market. In this article, we will delve into the details of the Iron Butterfly strategy, provide trade examples to illustrate its application, and show you how to automate it using Python.

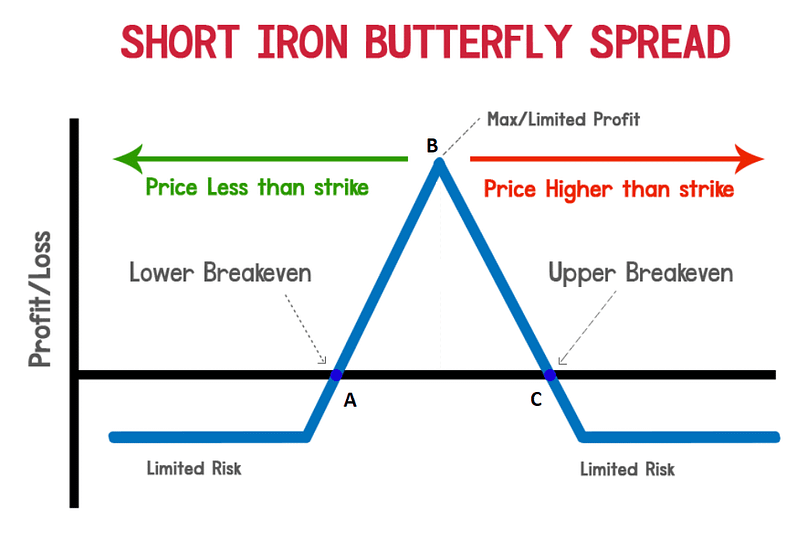

Iron Butterfly Strategy:

The Iron Butterfly strategy is a four-legged options strategy that involves selling an OTM call and put option, and buying a further OTM call and put option with the same expiration date. The strike prices of the call and put options are typically equidistant from the current stock price, creating a symmetrical payoff diagram. The Iron Butterfly strategy is often used in a neutral or slightly volatile market, where the trader expects the underlying stock or index to remain within a specific range until expiration.

Trade Example:

Let’s take a trade example to better understand the Iron Butterfly strategy. Suppose stock XYZ is currently trading at $100, and we decide to implement an Iron Butterfly strategy with the following parameters:

- Sell 1 XYZ 105 call at $2.00

- Sell 1 XYZ 95 put at $1.50

- Buy 1 XYZ 110 call at $0.50

- Buy 1 XYZ 90 put at $0.25

This would result in the following trade:

- Sell 1 XYZ 105 call at $2.00

- Sell 1 XYZ 95 put at $1.50

- Buy 1 XYZ 110 call at $0.50

- Buy 1 XYZ 90 put at $0.25

This trade creates a symmetrical Iron Butterfly strategy with a range-bound payoff diagram, as shown in the graphical representation of the strategy.

Code Example:

Now, let’s see how we can automate the Iron Butterfly strategy using Python. We will use the popular options trading library, py_vollib, to calculate the option prices and Greeks, and pandas for data manipulation. Here's an example code snippet that demonstrates how to implement the Iron Butterfly strategy using Python:

import py_vollib

import pandas as pd

# Define the option parameters

stock_price = 100

strike_call_sell = 105

strike_call_buy = 110

strike_put_sell = 95

strike_put_buy = 90

call_sell_price = 2.00

call_buy_price = 0.50

put_sell_price = 1.50

put_buy_price = 0.25

# Define the range for the stock price

stock_price_range = range(80, 121)

# Create a pandas DataFrame to store the option prices and Greeks

df = pd.DataFrame(index=stock_price_range, columns=['Call Option Price', 'Put Option Price', 'Total Option Price', 'Delta', 'Gamma', 'Theta', 'Vega'])

# Loop through each stock price in the range

for stock_price in stock_price_range:

# Calculate the option prices and Greeks for the call options

call_sell_option_price = py_vollib.black_scholes_merton.black_scholes_merton('c', stock_price, strike_call_sell, 1, 0.01, 0, 30/365)

call_buy_option_price = py_vollib.black_scholes_merton.black_scholes_merton('c', stock_price, strike_call_buy, 1, 0.01, 0, 30/365)

# Calculate the option prices and Greeks for the put options

put_sell_option_price = py_vollib.black_scholes_merton.black_scholes_merton('p', stock_price, strike_put_sell, 1, 0.01, 0, 30/365)

put_buy_option_price = py_vollib.black_scholes_merton.black_scholes_merton('p', stock_price, strike_put_buy, 1, 0.01, 0, 30/365)

# Calculate the total option price for the Iron Butterfly strategy

total_option_price = call_sell_price + put_sell_price - call_buy_price - put_buy_price

# Calculate the Greeks for the Iron Butterfly strategy

delta = call_sell_option_price['delta'] - call_buy_option_price['delta'] + put_sell_option_price['delta'] - put_buy_option_price['delta']

gamma = call_sell_option_price['gamma'] - call_buy_option_price['gamma'] + put_sell_option_price['gamma'] - put_buy_option_price['gamma']

theta = call_sell_option_price['theta'] - call_buy_option_price['theta'] + put_sell_option_price['theta'] - put_buy_option_price['theta']

vega = call_sell_option_price['vega'] - call_buy_option_price['vega'] + put_sell_option_price['vega'] - put_buy_option_price['vega']

# Store the calculated values in the DataFrame

df.loc[stock_price] = [call_sell_option_price['price'], put_sell_option_price['price'], total_option_price, delta, gamma, theta, vega]

# Print the DataFrame

print(df)This code calculates the option prices and Greeks for the Iron Butterfly strategy at different stock prices within a specified range. The py_vollib library is used to calculate the Black-Scholes-Merton option pricing model, which is commonly used for European options. The results are stored in a pandas DataFrame for easy analysis and further automation. Please note that this is a simplified example for illustrative purposes, and real-world trading may involve additional considerations such as transaction costs, margin requirements, and market liquidity. Always thoroughly understand the risks and complexities of options trading before implementing any automated trading strategy.

By automating the Iron Butterfly strategy using Python, traders can efficiently calculate and analyze option prices and Greeks at different stock prices, helping them make informed decisions on entry and exit points, risk management, and potential profit/loss scenarios. It’s essential to thoroughly test and validate any automated trading strategy using historical data and consider real-world market conditions before deploying it in a live trading environment.

Note: This article is curated using AI-assisted tools.

New to trading? Try crypto trading bots or copy trading on best crypto exchanges

Join Coinmonks Telegram Channel and Youtube Channel get daily Crypto News