Are You Aware That You May Be Paying Singapore GST Even Though You Made the Purchase from Overseas Vendors?

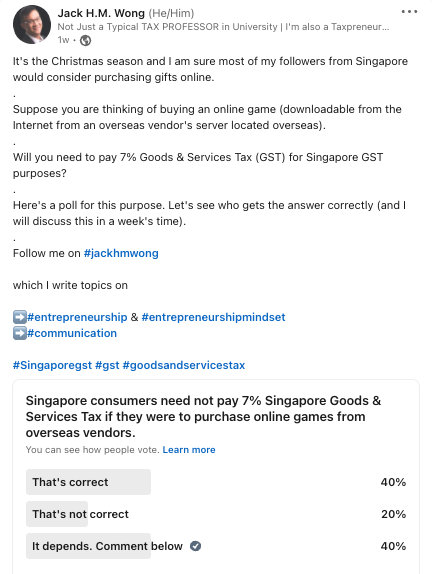

Last week, I created a poll to determine my followers’ awareness of the extended treatment of the Singapore Goods & Services Tax (GST) effective from 1 January 2020.

As you can see from the results, 40% agreed that Singapore consumers need not pay Singapore GST (currently at 7% and soon to be 9%) if they were to purchase the online games from overseas vendors via the Internet. 20% said this statement is incorrect, while 40% of the remaining followers said: “it depends.”

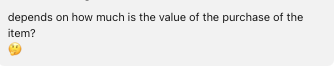

I asked one of the followers who voted for “it depends” for further elaboration, and this is the comment provided by this follower:

As promised, let’s discuss the correct Singapore GST analysis of this position.

What’s the correct answer?

The correct answer is “it depends.”

Why is it incorrect to say that “Singapore consumers need not pay7% Singapore GST if they purchase online games from overseas vendors”?

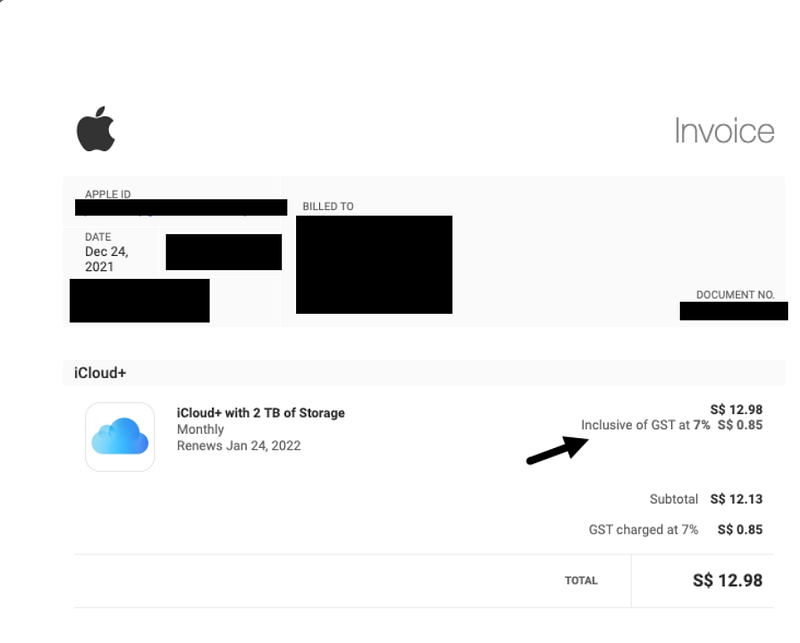

Please look at the following invoice I received from Apple yesterday on my monthly subscription to their iCloud services. Did you notice that a 7% GST is charged on this invoice?

Is this invoice from Apple Singapore? The answer is not. It is from one of the foreign entities under the Apple Group.

Is this invoice legitimate? The answer is yes. If you search the website of the Singapore tax authorities, you will find the following entities that have already registered for Singapore GST:

- Apple Canada Inc (M90372997G)

- Apple Distribution International Ltd (M90372993A)

- Apple Inc (M90372992E)

[Editor Note: We have only provided three Apple entitles in this newsletter. The list of Apple entities that have already registered for Singapore GST is more than that]

If you are a Singapore consumer and receive services from Amazon, Facebook, and Zoom, you may want to check your invoice because a GST is also charged at 7% (and soon to be 9%).

Accordingly, even though you may not be aware, you have already been paying Singapore GST on such services provided by non-Singapore service providers (i.e., overseas vendors), and this is the result of the introduction of the “Overseas Vendor Registration” (OVR) regime on the supply of B2C digital services practical from 1 January 2020.

As announced by the Ministry of Finance in last year’s Budget announcement, the existing OVR regime will be further extended to cover the supply of B2C remote services effective from 1 January 2023. Examples of remote services include the provision of online consulting and online coaching by overseas companies to Singapore consumers. If you are interested and haven’t yet subscribed to my newsletter, I have discussed this aspect in my previous newsletter (click here to read).

So, what conditions trigger the GST charge by overseas vendors to Singapore consumers?

Condition 1: Is this a supply of a Digital Service?

From the scenario mentioned in the poll, it is a supply of digital services by overseas vendors to Singapore consumers (who are not registered for Singapore GST).

More precisely, the term “digital services” can be found in Schedule 7 of the Goods & Services Tax Act (Cap. 117A) (“the Act”):

“any service supplied over the Internet or other electronic network and the nature of which renders its supply essentially automated with minimal or no human intervention, and impossible without the use of information technology.”

In our case, the transaction is about purchasing an online game from an overseas vendor via the Internet. And therefore, it falls within the meaning of ‘digital services” for Singapore GST purposes.

[Editor Note: This is not a supply of goods because the online game is downloadable via the Internet. For GST purposes, this is a supply of services instead of goods. Therefore, the GST charge does not depend on the value of the supply, as mentioned by one of my followers.]

Condition 2: Does a taxable person make this supply in the course or furtherance of any business carried on by him?

The next question is whether the overseas vendor is a “taxable” person for Singapore GDST when supplying digital services. This can be found under Section 8(1A) of the Act.

A taxable person for Singapore GST purposes is a person who has already been or is required to be registered for GST. This can be found under Section 8(2) of the Act.

Under Schedule 1 of the Act, an overseas vendor is liable to register for GST on either the retrospective or prospective basis.

Retrospective basis: The global turnover and value of digital services made to non-GST registered customers in Singapore for the calendar year (i.e., 1 January to 31 December) exceed S$1 million and S$100,000, respectively.

Prospective basis: There is a reasonable expectation that the value of the global turnover and supplies of digital services to non-GST registered customers in Singapore to exceed S$1 million and S$100,000, respectively, for the next 12 months.

From a Singapore consumer’s perspective, I would say that it is the responsibility of the overseas vendors to determine whether it is liable to register for Singapore GST and not the Singapore consumers.

In practice, if the overseas vendors are liable to register for Singapore GST but they fail to do so (and accordingly, no GST has been charged to the Singapore consumers), they are unlikely to recover the GST output tax subsequently from the Singapore consumers as the transactions are considered “done deals.”

In short, if the overseas vendors are already Singapore GST-registered, the supply of digital services in the abovementioned scenario will come with a GST charged at the prevailing rate (currently 7% and soon to be 9%). It means that there is no difference in the GST charge on this purchase between being made by a local GST-registered supplier and an overseas GST-registered vendor.

Can Singapore consumers not pay the 7% GST?

First, the GST charge forms part and parcel of the invoiced amount. It is the responsibility of the GST-registered overseas vendors to account for the proper amount of the GST and pay it to the Singapore tax authorities.

As consumers, as far as we understand, the possible way to avoid this GST charge legally is to provide the overseas vendors with their GST registration number. Nonetheless, even if the consumers are GST-registered, they must demonstrate that digital services are part and parcel of their business.

The Singapore tax authorities have warned non-GST registered customers and GST-registered customers purchasing these services for non-business purposes of the consequence of providing incorrect or false information to the overseas vendors. If they are caught, they may face a fine of up to $10,000, or in a case where there is evidence of willful intent to evade tax: (i) a fine of up to 3 times the amount of tax chargeable on the supply in addition to an amount not exceeding $10,000; and/or (ii) an imprisonment term of up to 7 years.

We trust that you will find this edition of our newsletter helpful. Let us know if you have any questions regarding the discussion above.

You can also subscribe to my “All Entrepreneurship Aside” Newsletter at http://succeedwithjackwong.com/newsletter

Jack HM Wong Taxpreneur | Accredited Tax Advisor | Associate Faculty of International Tax at Singapore University of Social Sciences

Originally published at https://www.linkedin.com.