Are Markets Efficient?

Yes, but not to the degree claimed by the Efficient Market Hypothesis (EMH).

Overview:

The Efficient Market Hypothesis (EMH) assumes that all participants behave rationally and that information is available to all. Because of these two assumptions, the market’s price should be the correct one.

Flaws in the Assumptions

In order for the market to work, the participants need to make logical decisions to drive the price to their true value. Mistakes can still be made by individual actors, as long as they are not systematic errors. On average, mistakes in one direction should be cancelled out by mistakes in the other direction. Other participants will buy/sell more to profit from the error.

The problem is that people do make systemic errors. Amos Tversky and Daniel Kahneman spent most of their careers documenting human biases. A good overview can be found in their book, Thinking Fast and Slow.

One example is Anchoring. It is the tendency to rely too heavily on an initial piece of information. All predictions and estimates are made in relation to that starting point. This can effect markets by influencing earnings estimates towards the first analyst’s estimates. It can also influence the price people are willing to pay for a stock because the current price acts as an anchor.

Counter Examples in Practice

Palm and 3Com Partial Spinoff

Back in 2000, 3Com did a partial spinoff (5%) of its Palm business by doing a partial IPO. The remaining shares were planned to be distributed to shareholders by the end of 2000. Each share holder would receive 1.5 shares of the new Palm stock for each share of 3Com. Before the Palm IPO, the price of 3Com was $104. After the IPO, Palm stock finished at $95. The EMH would predict that 3Com should have jumped to at least $145 (1.5 shares x 95$). Instead, the stock price fell to $82. Either the remaining assets of 3Com were worth -$60, or the market’s pricing of the Palm stock is inconsistent.

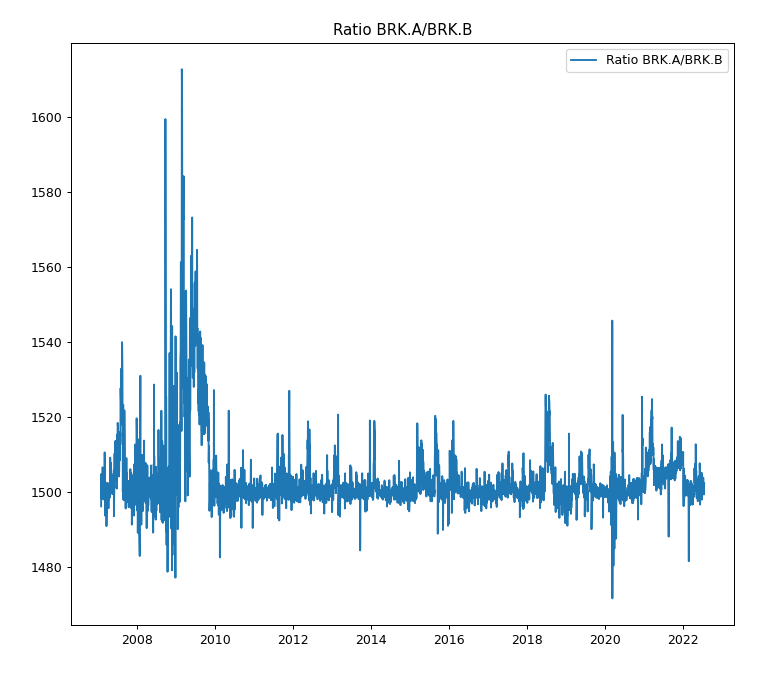

Berkshire A and B Shares

Market inefficiency can also present in different classes of stock. Berkshire Hathaway has class A shares that are worth x1,500 class B shares. There are differences in the voting proportion as well, but this is not a major factor in determining the value (if nothing else, it should be constant). Note that class A shares can be converted to 1,500 class B shares, but the reverse is not true.

If the EMH were correct, we would expect the ratio of the prices between the two classes to essentially be 1,500. There is actually a lot more variability in the relationship. The graph below shows this relationship using the closing price for both shares over the past 15 years. The relationship is close to 1500, but not precisely so. The biggest discrepancies happen when there is lots of selling (’08 financial crisis and 2020 Covid drop).

Any delta below 1,500 presents an arbitrage opportunity. When the ratio drops below 1,500, you could buy a class A share, convert it to 1,500 class B shares, and sell them. The profit would be the delta in the ratio relative to 1,500.

The Super-investors of Graham-and-Doddsville

In 1984, Warren Buffett gave a speech as part of a celebration of the 50th anniversary of Benjamin Graham’s Security Analysis. Michael Jensen also gave a speech in support of the EMH. Jensen’s main analogy was that orangutans wagering money on coin flips would produce some “winners” by chance alone.

Buffett agreed, but added, if all the winning primates came from the same zoo, wouldn’t it be worth seeing what the zoo feeds them? He then proceeds to list investors that come from the same intellectual “zoo” of value investing, as laid out by Benjamin Graham. These investors have beaten the market over extended periods (>10 years). Their analysis approach is value based, but each man selected different securities (so you can consider them independent “coin flips”).

I think you will find that a disproportionate number of successful coin-flippers in the investment world came from a very small intellectual village that could be called Graham-and-Doddsville. A concentration of winners that simply cannot be explained by chance can be traced to this particular intellectual village.

The Magic Formula

One last example comes from an investor who would make an updated version of the Super-investor list. Joel Greenblatt developed the magic formula as a value based approach that would let retail investors beat the market. It comes down to buying Good Business at “Cheap” prices. The strategy has beaten the market over every 5 year period back-tested. I did a more extensive article about this approach here:

He also made a free website to others follow the approach.

Conclusion:

Systematic Biases in Human Thinking can lead to market inefficiencies. The first example of this are different classes of stock that trade a prices out of whack with their ownership stake. Additionally, partial spin-offs give the market opportunities to price a stock twice. The market hasn’t always agreed with itself. There are other less obvious discrepancies between price and value. These opportunities are exploited by value investors, of which there are numerous examples.

If you enjoyed this article, feel free to “applaud”, and you can follow me on Medium or sign up for emails to be notified of more stories like this.

Note that this article does not provide personal investment advice and I am not a qualified licensed investment advisor. All information found here is for entertainment or educational purposes only and should not be construed as personal investment advice.

Some of the links in this article are affiliate links, and I may earn a small commission.

Subscribe to DDIntel Here.

Join our network here: https://datadriveninvestor.com/collaborate