An Open (Financial) Letter to Millennials

A Generation of Financials Wins and Financial Fails

The Millennial Generation (generally classified as those born between 1980 and 1999) is transforming the economic, social, and political world of the United States. Individuals in this generation are generally more optimistic, more diverse, and much more expressive (think Social Media) than older generations (US Chamber Foundation).

As an individual born right in the middle of this generation, I agree with the findings of this research. However, I want to focus on the many interesting financial characteristics and behaviors of my generation that may have the biggest impact of all these changes on our future.

Given my prior background in both the Finance and Financial Advising industries, I find this perspective especially interesting. In this field, I’ve worked with members of many different generations and held both a Series 7 and 65 license.

Financial “Wins” of the Millennial Generation

What do Millennials do better?

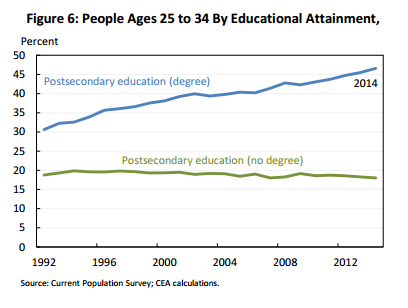

- Millennials Value Education

More Millennials have a college degree than any other generation of young adults. In 2013, 47% of 25–34 year-olds received a post-secondary degree.

College graduates are able to earn an additional $1 Million during their working lives compared to High School graduates. Millennials are investing in their future in this way, which is great news. But are they paying too much? We’ll get to that later…

(White House Millennials Report)

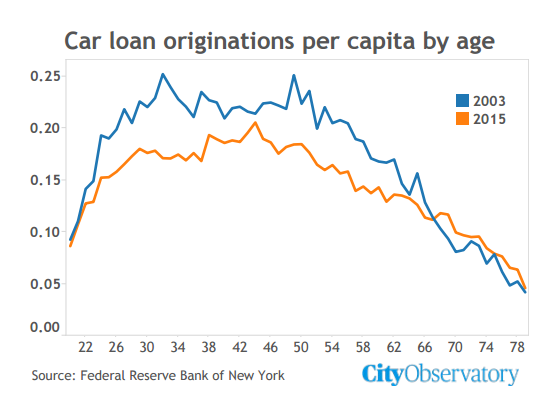

2. Millennials Don’t Buy Cars (or even bother getting driver’s licenses)

Millennials are about 29% less likely than those in Gen X to purchase a car (USA Streetsblog).

Diving a little deeper, in the chart below, you can see that in 2015, the share of car originations in the 22–35 age bracket was approximately 25% lower than it was during 2003, when the prior generation (Gen X) was in that same age bracket.

This is great news for Millennials. While they’re missing out on building their credit score through a car loan, they’re avoiding taking on (even) more debt. The reason for lower car ownership shouldn’t be surprising. The rise of Uber, Lyft, Car2Go, ZipCar, and many other transportation sharing options has made living without a car (in a city at least) possible for the first time.

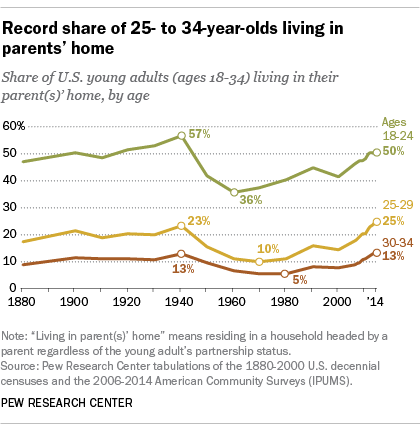

3. Millennials Live at Home with Their Parents

For the first time since 1880, young adults aged 18–34 are more likely to live with a parent than in any other arrangement.

Even more surprisingly, this trend isn’t being driven by the lack of employment, but rather the high cost of rent, delayed marriage, and a large increase in the high school education only segment of the generation (Pew Research).

For a generation that has the second-highest debt burden, this is good financial news. The Millennial generation members who live at home could theoretically save more of their paycheck and pay down debt faster, right?

Not so fast…it’s time for the financial fails of this new generation.

Financial “Fails” of the Millennial Generation

What don’t Millennials do right?

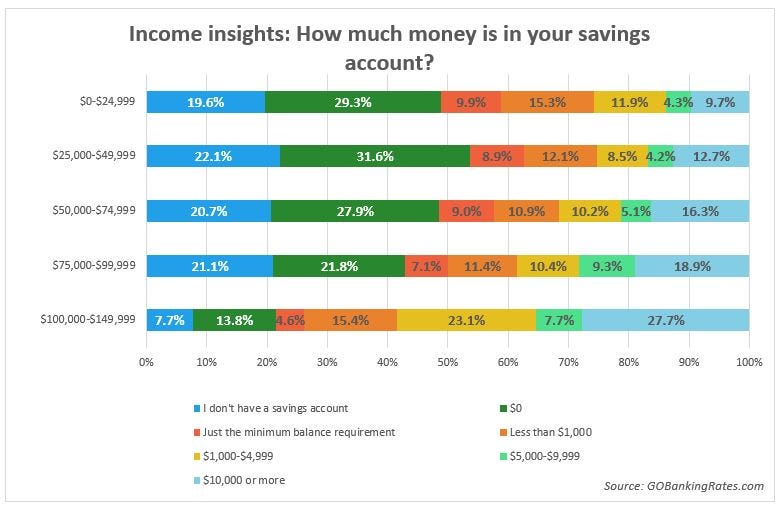

- Millennials Have Little to No Savings

23% of younger millennials (18–24) don’t have a savings account.

Even of older Millennials, the percentage isn’t much better at 18%. What’s interesting is this trend doesn’t appear to be driven by income. For those Millennials who make $75–$100k/year, 43% either don’t have a savings account or have nothing saved (Millennial Money).

For anyone who’s taken a basic math or finance class that covered the principle of compounding interest, you know this lack of savings won’t end well for the Millennial generation.

Take this simple example as proof:

Susan saves $5k/year from age 25–35 (10 years)

Bill saves $5k/year from age 35–65 (30 years)

John saves $5k/year from age 25–65 (40 years)

Who saves the most by retirement?

Well, that should be pretty easy, it’s John.

But by how much?

He will have saved over 2 times as much as Bill and close to 2 times as much as Susan by age 65.

Even more remarkable is that Susan, who only saved for 10 years, will have out-saved Bill who tried to play “catch-up” with his savings for 30 years! (Business Insider)

Millennials aren’t saving today and they aren’t going to be able to play “catch-up” later.

A Solution for Millennials: Digit; an automatic savings app that analyzes your linked accounts and determines a safe amount to transfer between $5-$50 every few days to a savings account.

Thanks for reading! If you’re enjoying this post, I think you would enjoy my new book Disrupting Yourself.

I’m offering a very limited time Medium discount on the Kindle version here: Disrupting Yourself Special Offer (if you prefer paperback: Disrupting Yourself Paperback)

And if you’re looking to learn more about Product Management or become a better Product Manager, I would pick up a copy of my book: Building Digital Products (New 2nd Edition!)

2. Millennials Pay Very High Rents

It’s an old Financial Advisor rule of thumb that you shouldn’t pay more than 30% of your take-home pay for housing. For a Millennial earning $60k/year pre-tax, this means that they should spend no more than $1,125/month in rent. But Millennials aren’t just ignoring this rule, they’re destroying it.

In San Francisco, Millennials are paying, on average, an absolutely unsustainable 79% of their salary for rent. In Los Angeles, it is 61%. In Boston, 56%. In Seattle, 51% (The Street). It’s starting to become more clear exactly why Millennials don’t have any money to save.

A Solution for Millennials: This one is old fashion. Live with roommates! Either split a 1BR with a significant other or shack up with several roommates in a house. It’s the only way to still live in a desirable area of the city (a big want for Millennials), while not breaking the bank (at least too badly).

3. Millennials Have Almost No Investments

As we mentioned in the #1 Financial Fail, savings are almost non-existent for my generation. If savings rates are bad for this generation than investing rates are [insert word for bad * infinity].

Nearly 4 in 5 millennials are not investing in the stock market (BusinessWire). While lack of money is a top barrier to investment (41%), there also appears to be a trust boundary, as a large portion of the Millennial generation matured during the 2008–2009 financial crisis. Over 1/3 of Millennials would actually trust an app with their money more than a traditional investment firm.

Why is this so scary?

Because as we mentioned before, the impact of not saving and not investing in the 25–35 age range can be devastating for retirement. Additionally, long-term investing is one of the only ways that you can grow your net worth consistently above the rate of inflation.

Two Solutions for Millennials: Acorns and Robinhood.

Similar to Digit, Acorns provides an automated investing app that takes “change” left over from every transaction made by a linked credit or debit card and transfers that amount to an investment account with simple investing options.

Robinhood provides completely fee-free investing in the stock market in an app-first format that’s great for both Millennials and new investors.

4. Millennials Subscribe to Everything

While subscriptions certainly can be convenient, it’s also incredibly easy to forget about them. Even the most savvy penny pinchers usually lack clear insight into the total amount of subscription expenses they have each and every month.

From Spotify to Netflix, from Trunk Club to Amazon Prime, Millennials absolutely love subscriptions. The reason is simple, Millennials care about high-quality products and much less about ownership (see previous examples for car and home ownership). 1 in 4 Millennials has either cut the TV cord or never owned cable.

A Solution for Millennials: Use TrueBill to quickly and easily track your subscriptions and even cancel those that you don’t use. TrueBill is the Mint for subscriptions. P.S., if you don’t use Mint, check that out too!

5. Millennials Pay the Minimum Payment for Student Loans (or even worse, miss payments!)

According to a recent survey, approximately 59% of Millennials have “no idea” when they will be able to pay off their student loans (Value Walk). The average student loan debt of a Millennial is over $41k.

For this amount of debt, if your minimum payment is $300/month, with a 6% interest rate, it will take you over 19 years to pay off your loans!

This type of debt can be crippling and will keep Millennials paying high rents instead of saving, investing, and owning.

A Solution for Millennials: Pay more than the minimum payment. In fact, you should be diverting all additional income to your student loans, prioritizing those (generally private loans) with significantly higher interest rates.

The limited exception to this strategy is if your company offers a 401k “match”, which is essentially free money that you should take maximum advantage of.

Millennials Need to Act Fast

As with almost every generation prior, Millennials are re-writing the rules.

They’re rewriting the rules for media, politics, family values, and finance. With finance specifically, my generation is doing some things right, but quite a few things wrong.

Hey Millennials!

We need to act fast if we want to reverse some of the trends I’ve highlighted.

We need to pay down debt, we need to save, we need to invest, and we need to reduce spending beyond our means. Retirement seems like an abstract concept to us (again, as it did to prior generations), but it will be here before we know it.

Check out my first book, Building Digital Products at www.buildingdigitalproducts.com

More About Alex Mitchell

Check out Alex’s Book: Building Digital Products

Amazon: https://www.amazon.com/Building-Digital-Products-Ultimate-Handbook/dp/1522824936

Digital Download: https://gum.co/CLccb

Disclosure: Some of the links in this post are affiliate links, meaning that at no additional cost to you, I earn a commission if you click them and purchase a product.