Algorithmically Identifying Stock Price Support & Resistance in Python

7 Essential Methods to Discover Key Price Levels in Stock Prices

1. Introduction

Support and resistance levels are foundational concepts in the world of trading, acting as critical signposts for making informed decisions. These levels help traders predict future breakout or breakdown scenarios. Traders typically discern these levels through manual observation and charting, however, with modern algorithmic techniques traders can now identify these crucial levels with enhanced precision and speed. The purpose of this article is to introduce you to 7 different techniques worth knowing in Python:

- Rolling Midpoint Range

- Fibonacci Retracement

- Swing Highs and Lows

- Pivot Point Analysis

- K-Means Price Clustering

- Volume Profiler

- Regression Modelling

2. Basics of Support and Resistance

Support and resistance highlight the areas where a stock’s price typically halts its upward or downward trajectory. While the support level acts as a cushion, suggesting significant buying interest, the resistance level emerges as a barrier, indicative of prevailing selling sentiment. An algorithmic approach ensures higher accuracy but also dynamically responds to market shifts, bestowing traders with an enhanced, data-driven edge in their decision-making processes.

3. Python Implementation Techniques

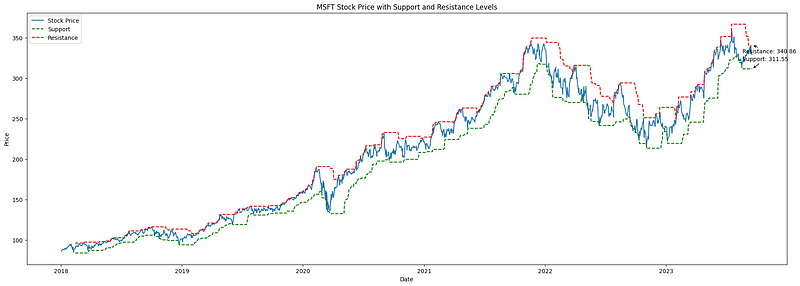

3.1 Rolling Midpoint Range

The Rolling Midpoint Range method employs moving averages and price range evaluations over a designated interval to highlight potential support and resistance areas. This approach fundamentally revolves around the rolling window concept:

- Determine High and Low: For each stock price point, a certain number of previous data points are considered. Within this window (e.g., 30 days), the highest and lowest prices are identified.

- Establish the Midpoint: This midpoint is calculated by taking the average of the identified high and low values.

- Set Support and Resistance Levels: Support is deduced from the midpoint by subtracting half of the price range (difference between the determined high and low). Conversely, resistance is inferred by adding half of this range to the midpoint.

import numpy as np

import pandas as pd

import yfinance as yf

import matplotlib.pyplot as plt

def find_levels(data, window):

high = data['High'].rolling(window=window).max()

low = data['Low'].rolling(window=window).min()

midpoint = (high + low) / 2

diff = high - low

resistance = midpoint + (diff / 2)

support = midpoint - (diff / 2)

return support, resistance

# Download historical stock prices

symbol = "MSFT"

start_date = '2018-01-01'

end_date = '2023-12-30'

data = yf.download(symbol, start=start_date, end=end_date)

window = 30

# Calculate support and resistance levels

support, resistance = find_levels(data, window)

# Plot the stock price, support, and resistance lines

fig, ax = plt.subplots(figsize=(24, 8))

ax.plot(data.index, data['Close'], label='Stock Price')

ax.plot(data.index, support, label='Support', linestyle='--', color='green')

ax.plot(data.index, resistance, label='Resistance', linestyle='--', color='red')

ax.set_xlabel('Date')

ax.set_ylabel('Price')

ax.set_title(f'{symbol} Stock Price with Support and Resistance Levels')

ax.legend()

# Add annotations for last support and resistance levels

last_support = support.iloc[-1]

last_resistance = resistance.iloc[-1]

ax.annotate(f'Support: {last_support:.2f}', xy=(support.index[-1], last_support),

xytext=(support.index[-1] - pd.DateOffset(days=30), last_support + 10),

arrowprops=dict(facecolor='green', arrowstyle='->'))

ax.annotate(f'Resistance: {last_resistance:.2f}', xy=(resistance.index[-1], last_resistance),

xytext=(resistance.index[-1] - pd.DateOffset(days=30), last_resistance - 10),

arrowprops=dict(facecolor='red', arrowstyle='->'))

plt.show()

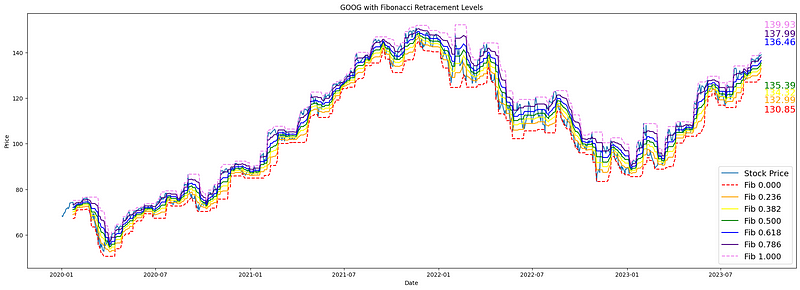

3.2 Fibonacci Retracement

Fibonacci Retracement, grounded in the Fibonacci sequence established by Leonardo Fibonacci in the 13th century, is a pivotal technical analysis tool. It pinpoints potential support and resistance zones, assisting traders in identifying prospective market reversal points. Here’s a concise breakdown:

- Understanding the Tool: Fibonacci retracement levels are horizontal markers on a chart, indicating where price reversals might occur. These levels — 23.6%, 38.2%, 50%, 61.8%, and 78.6% — signify how much of a prior price movement has been retraced. For instance, if a stock ascends from $10 to $20 and then drops to $15, it has retraced 50% of its rise.

- Application in Trading: These percentages are used to create horizontal lines on price charts, suggesting areas where prices might pivot. Such levels, particularly the 61.8% (Golden Ratio), are rooted in the Fibonacci sequence and have shown consistent relevance in influencing stock price behavior.

import yfinance as yf

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

# Get the stock data for ASML.AS

symbol = "GOOG"

stock_data = yf.download(symbol, start="2020-01-01", end="2023-12-17")

# Define the lookback period for calculating high and low prices

lookback_period = 15

# Calculate the high and low prices over the lookback period

high_prices = stock_data["High"].rolling(window=lookback_period).max()

low_prices = stock_data["Low"].rolling(window=lookback_period).min()

# Calculate the price difference and Fibonacci levels

price_diff = high_prices - low_prices

levels = np.array([0, 0.236, 0.382, 0.5, 0.618, 0.786, 1])

fib_levels = low_prices.values.reshape(-1, 1) + price_diff.values.reshape(-1, 1) * levels

# Get the last price for each Fibonacci level

last_prices = fib_levels[-1, :]

# Define a color palette for the Fibonacci levels

colors = ['red', 'orange', 'yellow', 'green', 'blue', 'indigo', 'violet']

# Plot the stock price with the Fibonacci retracement levels and last prices

fig, ax = plt.subplots(figsize=(24,8))

ax.plot(stock_data.index, stock_data["Close"], label="Stock Price")

offsets = [-16, -14, -12, -10, 8, 10, 12]

for i, level in enumerate(levels):

if level == 0 or level == 1:

linestyle = "--"

else:

linestyle = "-"

ax.plot(stock_data.index, fib_levels[:, i], label=f"Fib {level:.3f}", linestyle=linestyle, color=colors[i])

ax.annotate(f"{last_prices[i]:.2f}",

xy=(stock_data.index[-1], fib_levels[-1, i]),

xytext=(stock_data.index[-1] + pd.Timedelta(days=5), fib_levels[-1, i] + offsets[i]),

ha="left", va="center", fontsize=16, color=colors[i])

ax.set_xlabel("Date")

ax.set_ylabel("Price")

ax.set_title(f"{symbol} with Fibonacci Retracement Levels")

ax.legend(loc="lower right", fontsize=14)

plt.show()

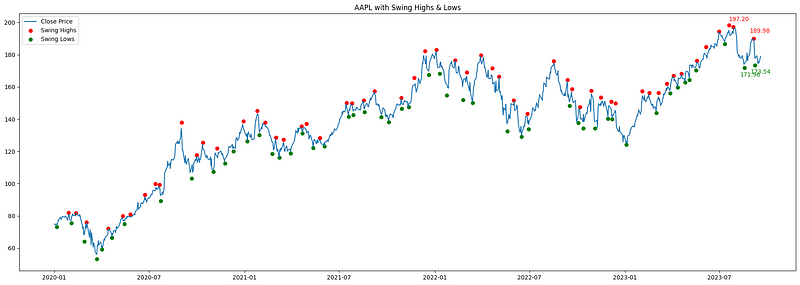

3.3 Swing Highs and Lows

Swing trading focuses on capitalizing on short-term price fluctuations by pinpointing key inflection points on a stock’s chart, known as “swing highs” and “swing lows.” These represent local maxima and minima where a stock’s price has reached a temporary peak or valley and might be poised to reverse its direction.

The methodology involves:

- Identifying Swing Highs: This entails finding points on the stock chart where the price is higher than those immediately surrounding it, suggesting areas of potential resistance.

- Spotting Swing Lows: Conversely, these are points where the stock price is lower than those immediately adjacent, indicating potential support levels.

import yfinance as yf

import pandas as pd

from scipy.signal import argrelextrema

import matplotlib.pyplot as plt

# Download stock data

symbol = "AAPL"

stock_data = yf.download(symbol, start="2020-01-01", end="2023-12-17")

# Identify local maxima (swing highs)

stock_data['Swing_High'] = stock_data['High'][argrelextrema(stock_data['High'].values, np.greater_equal, order=5)[0]]

# Identify local minima (swing lows)

stock_data['Swing_Low'] = stock_data['Low'][argrelextrema(stock_data['Low'].values, np.less_equal, order=5)[0]]

# Find last two non-NaN values for Swing Highs and Swing Lows

last_two_resistances = stock_data['Swing_High'].dropna().tail(2)

last_two_supports = stock_data['Swing_Low'].dropna().tail(2)

# Plotting

plt.figure(figsize=(24,8))

plt.plot(stock_data['Close'], label="Close Price")

plt.scatter(stock_data.index, stock_data['Swing_High'], color='r', label='Swing Highs', marker='o')

plt.scatter(stock_data.index, stock_data['Swing_Low'], color='g', label='Swing Lows', marker='o')

# Annotate the last two resistance and support prices

for date, price in last_two_resistances.items():

plt.annotate(f"{price:.2f}", (date, price), textcoords="offset points", xytext=(10,10), ha='center', color='r')

for date, price in last_two_supports.items():

plt.annotate(f"{price:.2f}", (date, price), textcoords="offset points", xytext=(10,-15), ha='center', color='g')

plt.title(f'{symbol} with Swing Highs & Lows')

plt.legend()

plt.show()

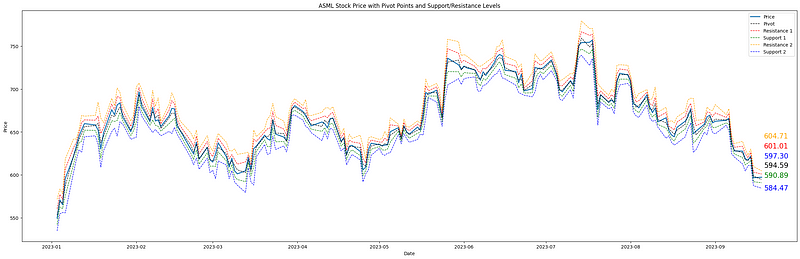

3.4 Pivot Point Analysis

Pivot points are short-term trend indicators used by traders to determine potential support and resistance levels. They are especially popular in day trading. The central pivot point, as well as derived support and resistance levels, are calculated using the high, low, and close prices of a previous period (usually the previous day for day trading).

Methodology:

- Pivot Point (P): It’s the average of the high, low, and close of the previous trading period. Pivot=(High+Low+Close)/3

- First Resistance (R1): It’s calculated by doubling the pivot point and then subtracting the previous low. R1=2×Pivot−Low

- First Support (S1): Derived by doubling the pivot point and then subtracting the previous high. S1=2×Pivot−High

- Second Resistance (R2): Obtained by adding the difference of high and low (the range) to the pivot point. R2=Pivot+(High−Low)

- Second Support (S2): Found by subtracting the range from the pivot point. S2=Pivot−(High−Low)

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import yfinance as yf

def calculate_pivot_points(df):

df['Pivot'] = (df['High'] + df['Low'] + df['Close']) / 3

df['R1'] = 2 * df['Pivot'] - df['Low']

df['S1'] = 2 * df['Pivot'] - df['High']

df['R2'] = df['Pivot'] + (df['High'] - df['Low'])

df['S2'] = df['Pivot'] - (df['High'] - df['Low'])

return df

ticker = 'ASML'

start_date = '2023-01-01'

end_date = '2023-12-31'

data = yf.download(ticker, start=start_date, end=end_date)

df = calculate_pivot_points(data)

df = df.dropna()

fig, ax = plt.subplots(figsize=(30, 9))

ax.plot(df.index, df['Close'], label='Price', linewidth=2)

ax.plot(df.index, df['Pivot'], label='Pivot', linestyle='--', linewidth=1, color='black')

ax.plot(df.index, df['R1'], label='Resistance 1', linestyle='--', linewidth=1, color='red')

ax.plot(df.index, df['S1'], label='Support 1', linestyle='--', linewidth=1, color='green')

ax.plot(df.index, df['R2'], label='Resistance 2', linestyle='--', linewidth=1, color='orange')

ax.plot(df.index, df['S2'], label='Support 2', linestyle='--', linewidth=1, color='blue')

ax.set_title(f'{ticker} Stock Price with Pivot Points and Support/Resistance Levels')

ax.set_xlabel('Date')

ax.set_ylabel('Price')

ax.legend()

# Annotate prices for the last observation

last_date = df.index[-1]

points = {

'Price': df['Close'].iloc[-1],

'Pivot': df['Pivot'].iloc[-1],

'R1': df['R1'].iloc[-1],

'S1': df['S1'].iloc[-1],

'R2': df['R2'].iloc[-1],

'S2': df['S2'].iloc[-1],

}

colors = {

'Price': 'blue',

'Pivot': 'black',

'R1': 'red',

'S1': 'green',

'R2': 'orange',

'S2': 'blue'

}

sorted_points = sorted(points.items(), key=lambda x: x[1])

for i, (label, value) in enumerate(sorted_points):

ax.annotate(f"{value:.2f}", xy=(last_date, value), xytext=(5, i * 15),

textcoords="offset points", fontsize=15, ha='left', va='center', color=colors[label])

plt.show()

3.5 K-Means Price Clustering

KMeans clustering is fundamentally about grouping data points that are statistically close to each other. When applied to stock prices, it groups together price levels that have been frequently visited over a specific time frame. The central positions of these clusters, called centroids, then signify key price levels where significant trading activity has occurred.

KMeans Helps in Identifying Support and Resistance in the Following Way:

- Clustering: By running the KMeans algorithm on the normalized price data (so that values range be values ranging between 0 and 1), it identifies clusters based on proximity. The centroids (or the center) of these clusters, especially in the price dimension, indicate significant levels around which price movements cluster.

- Interpreting Results: The y-coordinates of the centroids (representing price) can be treated as potential support or resistance levels. These are levels around which stock prices have historically shown significant activity.

import yfinance as yf

import numpy as np

import matplotlib.pyplot as plt

from sklearn.cluster import KMeans

# Download stock data

symbol = "AAPL"

stock_data = yf.download(symbol, start="2020-01-01", end="2023-12-17")

# Preparing data for clustering: Normalize time and price to have similar scales

X_time = np.linspace(0, 1, len(stock_data)).reshape(-1, 1)

X_price = (stock_data['Close'].values - np.min(stock_data['Close'])) / (np.max(stock_data['Close']) - np.min(stock_data['Close']))

X_cluster = np.column_stack((X_time, X_price))

# Applying KMeans clustering

num_clusters = 5

kmeans = KMeans(n_clusters=num_clusters)

kmeans.fit(X_cluster)

# Extract cluster centers and rescale back to original price range

cluster_centers = kmeans.cluster_centers_[:, 1] * (np.max(stock_data['Close']) - np.min(stock_data['Close'])) + np.min(stock_data['Close'])

# Plotting

plt.figure(figsize=(28,7))

plt.plot(stock_data['Close'], label="Close Price")

for center in cluster_centers:

plt.axhline(y=center, color='r', linestyle='--')

plt.annotate(f"{center:.2f}", xy=(stock_data.index[-1], center * 1.01), xytext=(5,0), textcoords="offset points", fontsize=15, ha='left', va='center', color='r')

plt.title(f'{symbol} Price Data with KMeans Clustering')

plt.legend()

plt.show()

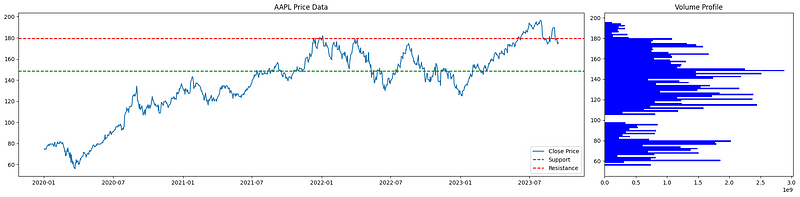

3.6 Volume Profiler

When determining potential key support and resistance levels, it is reasonable to consider the volume of trades occurring at different price levels. The volume profile provides a visual representation of trading activity (volume) at different price levels over a specified time frame. Unlike the volume histogram that plots volume against time, the volume profile plots volume against price, allowing us to identify price levels where a large amount of trading activity has occurred. These high-volume areas often act as significant support or resistance levels because they represent price points where a considerable amount of buying or selling has taken place in the past.

import yfinance as yf

import numpy as np

import matplotlib.pyplot as plt

# Download stock data

symbol = "AAPL"

stock_data = yf.download(symbol, start="2020-01-01", end="2023-12-17")

# Calculate volume profile

price_bins = np.linspace(stock_data['Low'].min(), stock_data['High'].max(), 100)

volume_profile = []

for i in range(len(price_bins)-1):

bin_mask = (stock_data['Close'] > price_bins[i]) & (stock_data['Close'] <= price_bins[i+1])

volume_profile.append(stock_data['Volume'][bin_mask].sum())

# Estimating support and resistance

current_price = stock_data['Close'].iloc[-1]

support_idx = np.argmax(volume_profile[:np.digitize(current_price, price_bins)])

resistance_idx = np.argmax(volume_profile[np.digitize(current_price, price_bins):]) + np.digitize(current_price, price_bins)

support_price = price_bins[support_idx]

resistance_price = price_bins[resistance_idx]

# Plotting

fig, (ax1, ax2) = plt.subplots(nrows=1, ncols=2, figsize=(20, 5), gridspec_kw={'width_ratios': [3, 1]})

ax1.plot(stock_data['Close'], label="Close Price")

ax1.axhline(y=support_price, color='g', linestyle='--', label='Support')

ax1.axhline(y=resistance_price, color='r', linestyle='--', label='Resistance')

ax1.legend()

ax1.set_title(f'{symbol} Price Data')

ax2.barh(price_bins[:-1], volume_profile, height=(price_bins[1] - price_bins[0]), color='blue', edgecolor='none')

ax2.set_title('Volume Profile')

plt.tight_layout()

plt.show()

print(f"Estimated Support Price: {support_price:.2f}")

print(f"Estimated Resistance Price: {resistance_price:.2f}")

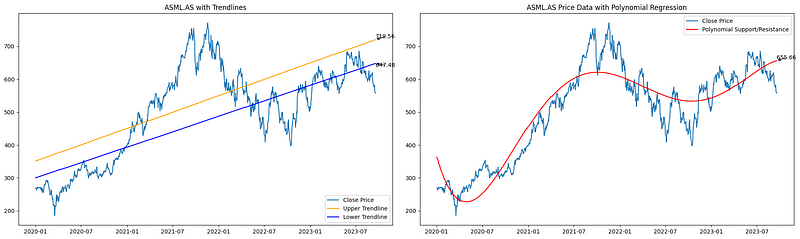

3.7 Linear and Polinomial Regression

Linear regression, applied in the realm of financial markets, offers a simplistic yet effective method to delineate dynamic support and resistance levels. By identifying swing highs and lows — key price points where the market has historically turned — it provides traders with a visual representation of a stock’s potential path, showcasing zones where a stock might find price support or resistance in the future.

Polynomial regression takes a different approach. Rather than straight lines, it draws curve-fitted lines to encapsulate the often non-linear nature of stock price changes. By integrating both these methodologies, traders gain a holistic viewpoint, enabling them to pinpoint possible shifts in market sentiment and zones of buying or selling pressure.

import yfinance as yf

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

from scipy.signal import argrelextrema

from sklearn.preprocessing import PolynomialFeatures

from sklearn.linear_model import LinearRegression

# Specify the ticker

symbol = "ASML.AS"

# Download stock data

stock_data = yf.download(symbol, start="2020-01-01", end="2023-12-17")

# Identify local maxima (swing highs) and minima (swing lows)

swing_highs = argrelextrema(stock_data['High'].values, np.greater_equal, order=5)[0]

swing_lows = argrelextrema(stock_data['Low'].values, np.less_equal, order=5)[0]

# Linear regression for trendlines

upper_m, upper_b = np.polyfit(swing_highs, stock_data['High'].values[swing_highs], 1)

lower_m, lower_b = np.polyfit(swing_lows, stock_data['Low'].values[swing_lows], 1)

stock_data['Upper_Trendline'] = upper_m * np.arange(len(stock_data)) + upper_b

stock_data['Lower_Trendline'] = lower_m * np.arange(len(stock_data)) + lower_b

# Preparing data for polynomial regression

X = np.array(range(len(stock_data))).reshape(-1, 1)

y = stock_data['Close'].values

# Polynomial regression

poly = PolynomialFeatures(degree=5)

X_poly = poly.fit_transform(X)

poly_regressor = LinearRegression()

poly_regressor.fit(X_poly, y)

y_pred = poly_regressor.predict(X_poly)

# Plotting

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(20,6))

ax1.plot(stock_data['Close'], label="Close Price")

ax1.plot(stock_data['Upper_Trendline'], label="Upper Trendline", color="orange")

ax1.plot(stock_data['Lower_Trendline'], label="Lower Trendline", color="blue")

# Annotate last prices for Trendlines

ax1.annotate(f"{stock_data['Upper_Trendline'].iloc[-1]:.2f}",

xy=(stock_data.index[-1], stock_data['Upper_Trendline'].iloc[-1]),

xytext=(stock_data.index[-1], stock_data['Upper_Trendline'].iloc[-1] + 5),

arrowprops=dict(arrowstyle='->'))

ax1.annotate(f"{stock_data['Lower_Trendline'].iloc[-1]:.2f}",

xy=(stock_data.index[-1], stock_data['Lower_Trendline'].iloc[-1]),

xytext=(stock_data.index[-1], stock_data['Lower_Trendline'].iloc[-1] - 10),

arrowprops=dict(arrowstyle='->'))

ax1.set_title(f'{symbol} with Trendlines')

ax1.legend(loc = "lower right")

ax2.plot(stock_data['Close'], label="Close Price")

ax2.plot(stock_data.index, y_pred, color='r', label="Polynomial Support/Resistance")

# Annotate last price for Polynomial Regression

ax2.annotate(f"{y_pred[-1]:.2f}",

xy=(stock_data.index[-1], y_pred[-1]),

xytext=(stock_data.index[-1], y_pred[-1] + 5),

arrowprops=dict(arrowstyle='->'))

ax2.set_title(f'{symbol} Price Data with Polynomial Regression')

ax2.legend()

plt.tight_layout()

plt.show()

4. Conclusion

Support and resistance levels serve as the cornerstones of technical analysis. Throughout this article, we delved into various methods ranging from the traditional pivot points to more advanced techniques such as K-means clustering and polynomial regression. The versatility of these methods offers traders a holistic view of potential price barriers.

Every method comes with its imperfections; support and resistance should be seen as zones rather than precise points. Furthermore, the accuracy of these techniques is deeply intertwined with the quality of the data they rely upon. In essence, while no single method promises infallibility, together they equip traders with a robust toolkit to navigate the markets more confidently.