Adjusting To And Surviving (Sticky) Inflation.

The Problem

Inflation is broadly defined as the price of goods and services going up over time. Thus, the purchasing power of the dollar (what $1 dollar can buy) consistently decreases over time.

As Nobel Prize, Libertarian economist Milton Friedman once opined:

“Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.”

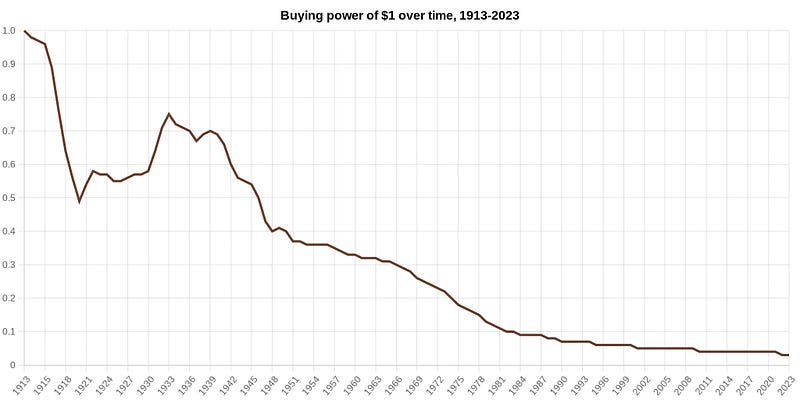

In fact, the dollar in your pocket has decreased nearly 100% in value since the founding of the Federal Reserve in 1913. #EndTheFed

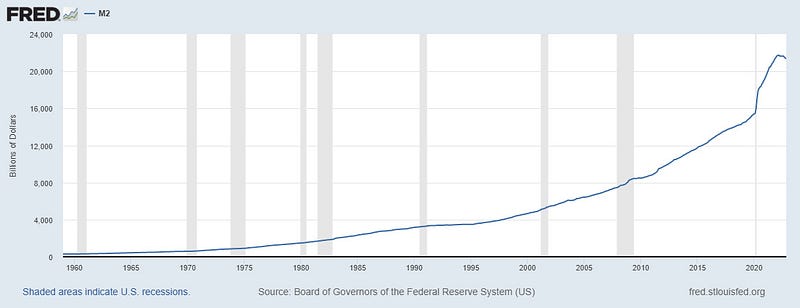

And to Friedman’s point about a “rapid increase in the quantity of money”…

Combine this massive increase in money supply since 2020, an incredible 42% increase in only 22 months, with government ordered closure of business and commerce, and you get this.

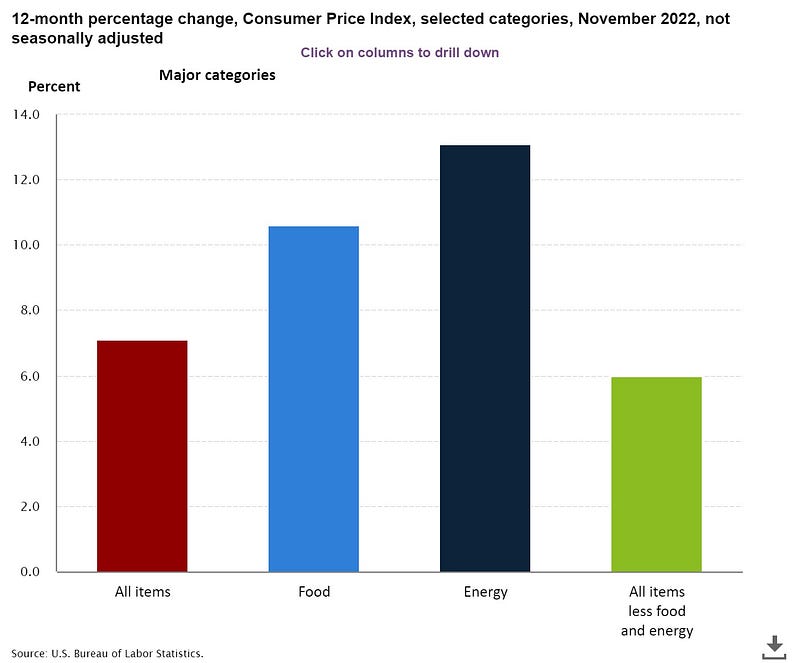

Never mind that anyone that looks at that official chart, and buys goods and services in the real economy on a daily basis, might cock their head at the PCI (Nov: 7.1 percent over the last 12 months) and PCE (Nov 22: 5.5 %) numbers and think, that’s all?…

Yes, inflation is coming down, thankfully. But, a return to the Federal Reserve’s arbitrary target of 2% may take more than 1 year, if we are even that lucky.

So, with that in mind, let’s dig in…

Given that “inflation is always and everywhere” it makes sense for us to focus on personal cost centers, as we all buy different things at different amounts, to a great extent.

Here is a breakdown of my household’s top 3 spending categories for 2022.

Housing: $21,275

Food (Grocery and Restaurants): $18,131

Misc. Shopping (everyday living minus utilities and energy): $12,564

You can use budget tracking features from Mint and Personal Capital to calculate your own major cost centers.

Once and only when you know where the bulk of your money is going, you’re in a position to make changes to reduce your costs.

Housing

I recently worked with my mortgage lender to lower my escrow withholdings, saving me over $1200 a year. Make sure you aren’t overpaying on taxes, etc.

Another strategy is to contact your insurance agent and make sure you are not over insured. Often a competing quote or making small changes to your coverage can add up to big savings.

Food

My wife and I are looking for ways to still eat well (meat and plants) while spending less. This includes buying in bulk and only things on sale, taking advantage of Prime discounts at Whole Foods, trying again with places like Aldi, and cutting back on snacks, treats, etc. Even spending $20 to $30 less per week on food can really add up.

Shopping

Finally, we are taking a hard look at our “Shopping” category. Target is a dangerous place. If you consciously adopt a “Need/Love” vs “Like/Want” approach to your spending, major gains can be had when you spend money.

Most all of what we buy beyond securing shelter, food, energy and transportation is a “Like/Want”.

Conclusion

Remember, “inflation is always and everywhere”, and we are likely dealing with higher than normal inflation for quite some time yet. Take active steps to reduce your outlays and the next year or two can be easier to navigate financially.

Thanks for reading. Be good stewards of your earnings.