Accounting Handbook for Beginners

1. Introduction to Accounting

Definition and Purpose

Accounting is the process of recording, analyzing, and reporting financial transactions. It is crucial for businesses and individuals to track and understand their financial activities.

Accounting provides accurate financial information for decision-making, resource allocation, and strategic planning. It helps stakeholders assess financial health and make informed choices.

Financial planning, risk identification, and regulatory compliance are also important aspects of accounting. It enables budgeting, goal setting, and monitoring progress. Accounting promotes transparency and accountability.

Accounting is essential for sound financial management, decision-making, financial planning, and regulatory compliance.

History and Evolution

Accounting has evolved throughout history.

In ancient times, basic accounting methods were used to track economic transactions.

The Renaissance introduced double-entry bookkeeping, revolutionizing accounting. Industrialization in the 19th century made accounting crucial for managing complex finances. Accounting standards and principles were established. In the 20th century, technology advancements like computers and software transformed accounting.

Today, accounting is essential for businesses and individuals, with specializations like managerial and forensic accounting.

Accounting has progressed from simple record-keeping to sophisticated systems that provide valuable financial information for decision-making, compliance, and planning.

Key Principles of Accounting

The fundamental principles that underlie accounting practices are crucial for maintaining accurate and reliable financial statements. These principles, including the accrual basis of accounting, consistency, and conservatism, play a vital role in guiding the recording and reporting of financial transactions.

- Accrual Principle: The principle of accrual accounting states that revenue and expenses should be recognized when they are incurred, regardless of when cash is exchanged.

- Conservatism Principle: The principle of accounting for beginners v2 advises accountants to choose the option that is least likely to overstate assets and income, promoting prudence in financial reporting to avoid overestimating profits or assets.

- Consistency Principle: Consistency in accounting methods and procedures is crucial for meaningful comparisons of financial information between different periods, enhancing the reliability and comparability of financial statements.

- Materiality Principle: In financial statements, only transactions or items that have a significant impact on decision-making should be disclosed, while immaterial items can be omitted.

- Matching Principle: The principle of matching expenses with revenues ensures that costs associated with generating revenue are recognized in the same period, leading to accurate financial reporting.

- Objectivity Principle: Financial statements should be based on objective evidence and verifiable data, with accountants minimizing bias and subjective judgment in their preparation.

- Prudence Principle: The conservatism principle in accounting, also known as the principle of caution, highlights the importance of recognizing potential losses as soon as they are probable, while potential gains should only be recognized when realized.

- Revenue Recognition Principle: Revenue should be recognized when earned and realizable, not necessarily when cash is received, to accurately reflect the company’s performance.

- Going Concern Principle: Financial statements are prepared with the assumption of the business’s ongoing operation, valuing assets at historical cost and not immediately requiring long-term obligations to be due.

- Cost Principle: The historical cost principle, also known as accounting for beginners, states that assets should be recorded at their original acquisition cost, providing a reliable basis for accounting, even though it may not reflect their current market value.

2. Understanding Financial Statements

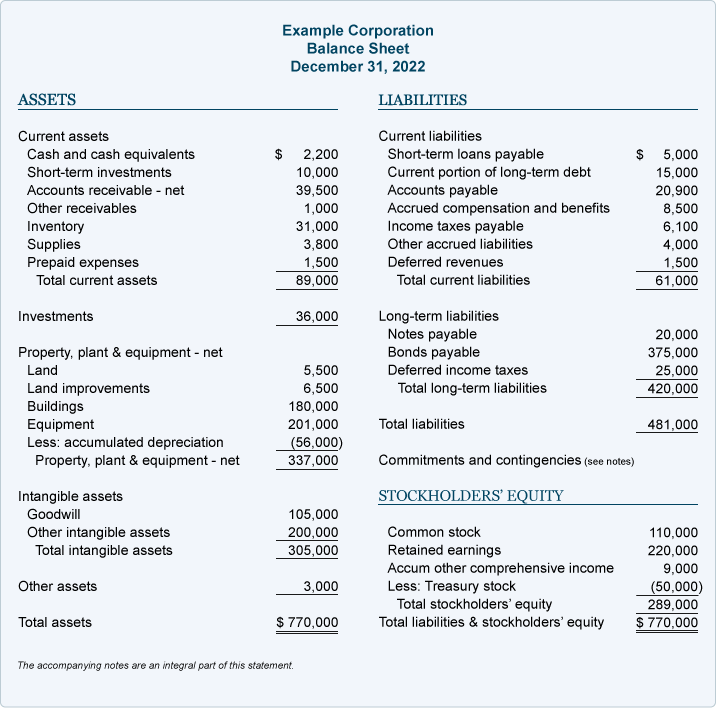

Balance Sheet

A balance sheet is a financial statement that shows the financial position of a business at a specific point in time. It consists of three main components: assets, liabilities, and equity.

- Assets: Assets are the resources owned by the business that have economic value. They can be tangible assets like cash, inventory, or property, as well as intangible assets like patents or trademarks. Assets represent what the business owns and can include both current assets (those that can be converted into cash within a year) and non-current assets (those with a longer-term value).

- Liabilities: Liabilities are the obligations or debts of the business. They represent what the business owes to creditors or other external parties. Liabilities can include loans, accounts payable, or accrued expenses. Similar to assets, liabilities can be classified as current liabilities (due within a year) or non-current liabilities (due in more than a year).

- Equity: Equity, also known as shareholders’ equity or owner’s equity, represents the residual interest in the assets of the business after deducting liabilities. It is the ownership claim on the business’s assets and is calculated by subtracting total liabilities from total assets. Equity can be further divided into contributed capital (the initial investments made by owners) and retained earnings (the accumulated profits or losses of the business).

The balance sheet provides a snapshot of the financial position of a business by showing the relationship between these three components. It follows the accounting equation: Assets = Liabilities + Equity. This equation must always be in balance, hence the name “balance sheet.” By examining the balance sheet, stakeholders can assess the liquidity, solvency, and overall financial health of the business at a specific point in time.

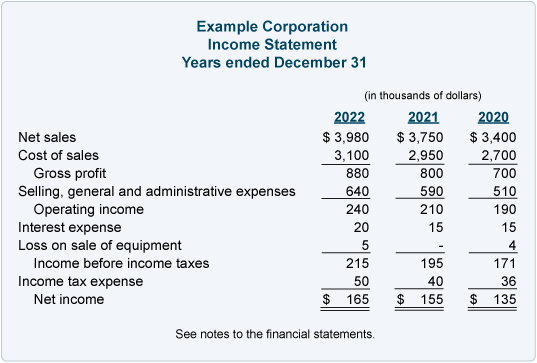

Income Statement

An income statement, also called a profit and loss statement, summarizes a company’s revenue, expenses, and profits over a specific period. It is used by investors, creditors, and stakeholders to evaluate financial performance and profitability..

The income statement begins with the company’s total revenues, which include all income from selling goods or services, interest income, and other operating revenues. This figure represents the total amount of money earned by the company during the specified period.

💡 Revenues are essential because they indicate the company’s ability to generate sales and generate cash flow.

From the total revenues, the cost of goods sold (COGS) is subtracted. COGS includes the direct costs associated with producing or delivering the goods or services sold by the company.

This can include the cost of raw materials, labor, and manufacturing overhead. By subtracting COGS from total revenues, the company obtains its gross profit, which represents the profit generated from the company’s core operations.

After calculating the gross profit, the income statement deducts the operating expenses from the gross profit to arrive at the operating profit, also known as operating income or operating earnings.

Operating expenses include costs such as salaries, rent, utilities, marketing expenses, and other expenses directly related to the day-to-day operations of the business.

💡 The operating profit reflects the profitability of the company’s core business activities and indicates how well the company is managing its expenses.

In addition to the operating profit, the income statement includes other income and expenses that are not directly related to the company’s core operations. This can include interest expenses, gains or losses from investments, or any other non-operating items. These items are accounted for to calculate the net income before taxes (EBIT), which represents the company’s total profit before tax obligations.

Taxes owed by the company are deducted from the net income before taxes to arrive at the net income, also known as the bottom line or net profit. It is a crucial metric for assessing the profitability and financial health of a company.

💡 Net income represents the company’s total profit after all expenses and taxes have been accounted for.

The income statement is a valuable tool for stakeholders to analyze a company’s financial performance, profitability, revenue generation, expense control, and growth prospects. It is essential for decision-making, financial analysis, and assessing overall financial health.

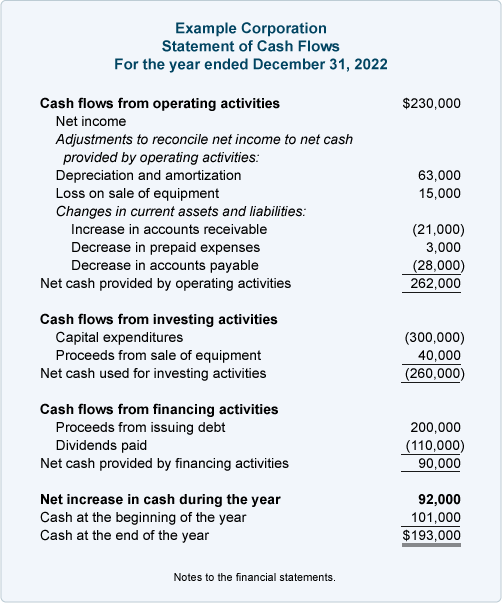

Cash Flow Statement

Although accounting is here for ages cash flow statement is the youngest among the 3 financial statements, some argue the most important one even.

The cash flow statement has its roots in early 20th-century financial analysis, gaining prominence during the Great Depression. However, it wasn’t until the late 20th century that it became standardized. In the 1970s, the AICPA began advocating for its inclusion in financial statements, leading to the issuance of SFAS №95 by the FASB in 1987, mandating its presentation. Since then, it has become an integral part of financial reporting globally, providing crucial insights into a company’s liquidity and cash management.

The cash flow statement is an essential financial statement that provides valuable insights into a business’s liquidity position and cash management. It highlights the inflows and outflows of cash and categorizes them into three main activities: operating, investing, and financing.

- Operating activities refer to the cash flows generated from a company’s core business operations, such as sales revenue, payment to suppliers, and salaries paid to employees. This section shows the cash generated or used in day-to-day operations and indicates the company’s ability to generate cash flow from its primary activities.

- Investing activities involve the cash flows related to the acquisition or disposal of long-term assets, such as property, plant, and equipment, as well as investments in other companies or financial instruments. Cash flows from investing activities include cash spent on capital expenditures or received from the sale of assets. This section provides insights into the company’s investments and its commitment to long-term growth.

- Financing activities represent the cash flows associated with external financing and capital structure changes. This includes cash received from issuing stocks or bonds, as well as cash paid for dividends, debt repayments, or share repurchases. The financing activities section reflects how a company funds its operations and expansion and how it returns value to its shareholders.

Understanding the cash flow statement is crucial for businesses to assess their ability to meet short-term obligations, manage working capital, and evaluate financial health. Positive cash flow from operating activities indicates a healthy business, while investing and financing activities provide insights into capital investments and financing decisions.

Analyzing the cash flow statement helps businesses identify cash flow issues, plan investments, and make informed financing and capital allocation decisions. It is a valuable tool for stakeholders to evaluate a company’s ability to generate and manage cash for sustainable growth and financial stability.

3. The Accounting Cycle

Bookkeeping Basics

Single-entry bookkeeping is a simple method where each financial transaction is recorded once, either as an income or expense. It is commonly used by small businesses or individuals to track their cash flow.

On the other hand, double-entry bookkeeping is a more comprehensive system that records each financial transaction twice, as both a debit and a credit. This method ensures that the accounting equation (Assets = Liabilities + Equity) is always in balance and provides a more accurate and complete picture of a company’s financial position.

Keeping accurate records is crucial for several reasons. It allows businesses to track their income and expenses, monitor cash flow, and assess profitability. Accurate records also help in preparing financial statements, filing taxes, and complying with legal and regulatory requirements.

Accurate records enable businesses to analyze trends, make informed decisions, and identify areas for improvement. They also provide a clear audit trail and support transparency and accountability.

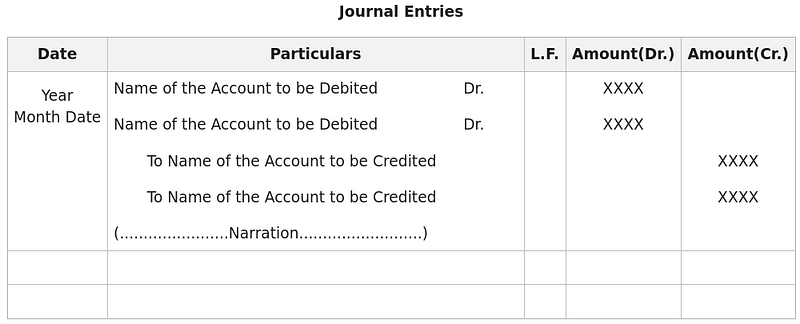

Journal Entries

To record financial transactions using debits and credits

- Determine the accounts involved: Identify the accounts that will be affected by the transaction. For example, if a sale is made, the accounts involved might be “Accounts Receivable” and “Sales Revenue.”

- Determine the account type: Determine whether the accounts are assets, liabilities, equity, revenues, or expenses. This will determine whether the account is increased or decreased by a debit or credit.

- Apply the rules of debits and credits: Assets and expenses increase with debits and decrease with credits. Liabilities, equity, and revenues increase with credits and decrease with debits.

- Record the transaction: Debit the account(s) that increase on the left side of the ledger. Credit the account(s) that increase on the right side of the ledger.

💡 Every transaction must have an equal amount of debits and credits to keep the accounting equation in balance.

Ledger Accounts

Ledger accounts serve as a central repository for organizing financial data in accounting. They are used to record and track individual transactions related to specific accounts, such as assets, liabilities, equity, revenues, and expenses.

The purpose of ledger accounts is to provide a detailed record of each transaction that occurs within a business. Each account has its own ledger, and all transactions related to that account are recorded in the respective ledger. Ledger accounts contain information such as the date of the transaction, the amount, a description of the transaction, and the accounts involved.

By using ledger accounts, businesses can easily track and monitor their financial activities. Ledger accounts allow for the classification and organization of transactions based on their respective accounts. This organization makes it easier to generate financial statements and reports, analyze financial performance, and ensure accuracy in recording and reporting.

Ledger accounts also facilitate the process of preparing trial balances and financial statements at the end of accounting periods. The balances in the ledger accounts are used to compile the trial balance, which is a summary of all the accounts and their respective balances. The trial balance serves as a tool to verify that the total debits equal the total credits and ensures the accuracy of the financial records.

In summary, ledger accounts play a crucial role in organizing financial data by providing a detailed record of each transaction and facilitating the preparation of financial statements. They help businesses monitor their financial activities, analyze performance, and ensure accuracy in recording and reporting transactions.

Trial Balance

To prepare a trial balance

- Collect all the ledger account balances from the general ledger. This includes the balances of all assets, liabilities, equity, revenues, and expenses accounts.

- List the account names and their respective debit or credit balances in a trial balance worksheet or spreadsheet. Debit balances are listed in the left column, while credit balances are listed in the right column.

- Calculate the total of the debit column and the total of the credit column.

- Verify that the total of the debit column equals the total of the credit column. If they are equal, the trial balance is considered balanced.

The trial balance plays a crucial role in ensuring the accuracy of financial records. It serves as a tool to check the equality of debits and credits, which is a fundamental principle in accounting. If the trial balance is balanced, it indicates that the total debits recorded in the ledger accounts equal the total credits recorded. This suggests that the accounting entries have been accurately recorded.

However, it’s important to note that a balanced trial balance does not guarantee the absence of errors. It only ensures that the debits and credits have been recorded correctly. Mistakes such as posting incorrect amounts, omitting transactions, or applying incorrect account balances can still occur. Therefore, the trial balance is typically followed by further steps in the accounting cycle, such as adjusting entries, financial statement preparation, and thorough financial analysis.

The trial balance is a valuable tool in accounting that verifies the accuracy of financial records by checking the equality of debits and credits. It serves as an initial step in preparing financial statements and aids in further analysis and decision-making.

Adjusting Entries

Adjusting entries are necessary at the end of an accounting period to ensure that financial statements accurately reflect the financial position and performance of a business. These entries are made to record transactions or events that occurred during the period but were not initially recorded or were recorded incorrectly.

The main purposes of adjusting entries are:

- Accruals: Adjusting entries are used to recognize revenues and expenses that have been earned or incurred but have not yet been recorded. For example, if a company provides services to a customer in December but does not receive payment until January, an adjusting entry is made to recognize the revenue in December.

- Prepayments: Adjusting entries are also used to account for prepayments or expenses paid in advance. For example, if a company pays rent for the next three months in advance, an adjusting entry is made to allocate the rent expense over the three-month period.

- Depreciation: Adjusting entries are made to record the depreciation of assets. Depreciation is the process of allocating the cost of an asset over its useful life. By making adjusting entries for depreciation, the company can match the cost of the asset with the revenue it generates over time.

- Accrued Expenses: Adjusting entries are used to record expenses that have been incurred but not yet paid. For example, if a company receives an electricity bill at the end of the month but has not yet made the payment, an adjusting entry is made to recognize the expense.

- Accrued Revenues: Adjusting entries are made to record revenues that have been earned but not yet received. For example, if a company provides consulting services to a client but has not yet billed the client, an adjusting entry is made to recognize the revenue.

By making these adjusting entries, the financial statements reflect the correct amounts of revenue, expenses, assets, liabilities, and equity. This ensures that the financial statements provide an accurate representation of the company’s financial performance and position at the end of the accounting period.

💡 Real-Life Scenario: The most common adjusting entry is for accounting and audit expenses for the year-end. This entry ensures that the cost is allocated to the correct year it is related to, rather than being recorded based on when the invoice is received, which often occurs in the following year when the audit is performed.

Financial Statement Preparation

To compile the adjusted trial balance into the final financial statements

Prepare the Income Statement

Start by transferring the revenue and expense account balances from the adjusted trial balance to the income statement. Calculate the net income by subtracting total expenses from total revenues.

- Start with the company’s total revenues, which include all income from selling goods or services, interest income, and other operating revenues.

- Subtract the cost of goods sold (COGS) from the total revenues. COGS includes the direct costs associated with producing or delivering the goods or services sold by the company.

- From the gross profit, deduct the operating expenses to arrive at the operating profit, also known as operating income or operating earnings. Operating expenses include costs such as salaries, rent, utilities, and marketing expenses.

- Include any other income and expenses that are not directly related to the company’s core operations.

- Calculate the net income before taxes (EBIT) by subtracting taxes owed by the company from the net income before taxes.

- Finally, deduct the taxes owed to arrive at the net income, also known as the bottom line or net profit.

Prepare the Statement of Retained Earnings

If applicable, prepare the statement of retained earnings. Begin with the opening balance of retained earnings and adjust it for net income or loss from the income statement, dividends, and any other relevant transactions. Calculate the closing balance of retained earnings.

- Beginning Retained Earnings: Start with the beginning balance of retained earnings, which can be obtained from the previous period’s financial statements.

- Add Net Income or Subtract Net Loss: Add the net income or subtract the net loss for the current period. Net income represents the company’s total revenue minus expenses, while a net loss indicates that expenses exceed revenue.

- Subtract Dividends: Subtract any dividends or distributions paid to shareholders during the period. Dividends are a portion of the company’s earnings distributed to shareholders.

- Add or Subtract Other Adjustments: Add or subtract any other adjustments that affect retained earnings, such as prior period adjustments or changes in accounting policies.

- Ending Retained Earnings: Calculate the ending balance of retained earnings by adding or subtracting the net income or loss, dividends, and other adjustments from the beginning retained earnings.

Prepare the Balance Sheet

Transfer the asset, liability, and equity account balances from the adjusted trial balance to the balance sheet. Organize the accounts based on their classification and calculate the total assets, total liabilities, and total equity. Ensure that the accounting equation (Assets = Liabilities + Equity) is in balance.

- Assets: Assets are resources owned by a business with economic value. This includes tangible assets (e.g., cash, inventory, property) and intangible assets (e.g., patents, trademarks). Assets can be classified as current (short-term) or non-current (long-term).

- Liabilities: Liabilities are the debts of the business, including loans, accounts payable, and accrued expenses. They can be classified as current liabilities (due within a year) or non-current liabilities (due in more than a year).

- Equity: Equity is the ownership claim on a business’s assets. It is calculated by subtracting liabilities from assets. Equity can be divided into contributed capital (initial investments by owners) and retained earnings (accumulated profits or losses).

Prepare the Cash Flow Statement

If required, prepare the cash flow statement using information from the adjusted trial balance, additional supporting schedules, and other relevant data. Categorize cash flows into operating, investing, and financing activities..

- Operating activities Cash flow refers to the money generated or used in a company’s core operations. It includes sales revenue, payments to suppliers, and employee salaries. This section shows the company’s ability to generate cash flow from its main activities.

- Investing activities This section covers cash flows related to acquiring or selling long-term assets, like property, equipment, and investments in other companies or financial instruments. It includes cash spent on capital expenditures and received from asset sales. It provides insights into the company’s investments and commitment to long-term growth.

- Financing activities This section represents cash flows related to external financing and changes in capital structure. It includes cash received from issuing stocks or bonds, and cash paid for dividends, debt repayments, or share repurchases. It shows how a company funds its operations, expands, and returns value to shareholders.

Review and Analyze the Financial Statements

Carefully review the financial statements for accuracy, consistency, and compliance with accounting standards. Analyze the financial statements to assess the financial performance, liquidity, and overall financial health of the business.

Financial ratios are widely used for financial analysis. Some common financial ratios include:

Liquidity Ratios: These ratios measure a company’s ability to meet short-term obligations and assess its liquidity. Examples include the current ratio and the quick ratio.

- Current Ratio = Current Assets / Current Liabilities

- Quick Ratio: (Current Assets — Inventory) / Current Liabilities

- Cash Ratio: Cash and Cash Equivalents / Current Liabilities

Profitability Ratios: Profitability ratios evaluate a company’s ability to generate profits from its operations. Examples include the gross profit margin, operating profit margin, and net profit margin.

- Gross Profit Margin = (Gross Profit / Revenue) * 100

- Net Profit Margin = (Net Income / Revenue) * 100

- Return on Assets (ROA) = (Net Income / Total Assets) * 100

- Return on Equity (ROE) = ``(Net Income / Shareholders’ Equity) * 100

- Return on Investment (ROI) = (Net Profit / Total Investment) * 100

- Operating Profit Margin = (Operating Profit / Revenue) * 100

Return on Investment (ROI) Ratios: ROI ratios measure the return on investment for shareholders and investors. Examples include return on assets (ROA) and return on equity (ROE).

- ROI = (Net Profit / Investment Cost) * 100

- Net Profit = Total Revenue — Total Expenses

- Investment Cost = Initial Investment + Additional Investments

Debt Ratios: These ratios assess a company’s level of debt and its ability to meet long-term obligations. Examples include the debt-to-equity ratio and the interest coverage ratio.

- Debt-to-Equity Ratio = Total Debt / Total Equity

- Debt Ratio = Total Debt / Total Assets

- Equity Ratio = Total Equity / Total Assets

- Debt-to-EBITDA Ratio = Total Debt / EBITDA

Efficiency Ratios: Efficiency ratios measure how effectively a company is utilizing its assets and resources. Examples include the inventory turnover ratio and the accounts receivable turnover ratio.

- Inventory Turnover Ratio = Cost of Goods Sold / Average Inventory

- Accounts Receivable Turnover Ratio = Net Credit Sales / Average Accounts Receivable

- Accounts Payable Turnover Ratio = Cost of Goods Sold / Average Accounts Payable

- Asset Turnover Ratio = Net Sales / Average Total Assets.

Market Value Ratios: Market value ratios assess the market’s perception of a company’s value. Examples include the price-to-earnings ratio (P/E ratio) and the market-to-book ratio.

- Price-to-Earnings (P/E) Ratio = Market Price per Share / Earnings per Share (EPS)

- Price-to-Book (P/B) Ratio = Market Price per Share / Book Value per Share

- Price-to-Sales (P/S) Ratio = Market Price per Share / Sales per Share

- Dividend Yield = (Dividends per Share / Market Price per Share) * 100%

- Dividend Payout Ratio = (Dividends per Share / Earnings per Share) * 100%

Disclose Supplementary Information

Consider including supplementary information or notes to the financial statements to provide additional details or explanations about specific transactions, accounting policies, or significant events.

Finalize and Distribute the Financial Statements

Once the financial statements are reviewed and approved, finalize them by ensuring all necessary adjustments and disclosures are included. Distribute the finalized financial statements to relevant stakeholders, such as management, shareholders, lenders, and regulatory authorities.

It is important to note that the specific steps and requirements for compiling financial statements may vary based on accounting standards, industry regulations, and the specific needs of the organization. Consulting with accounting professionals or referring to relevant accounting guidelines can provide further guidance in preparing accurate and compliant financial statements.

4. Basic Accounting Concepts and Terms

Assets

Assets are resources owned or controlled by a company that have economic value and are expected to provide future benefits. They can be tangible physical items, such as property or equipment, or intangible items, such as patents or goodwill. Assets are typically categorized as current or non-current (long-term) based on their liquidity and expected conversion to cash within one year. Here are some examples:

Current Assets

These are assets expected to be converted into cash or used up within one year.

- Cash and Cash Equivalents: Physical currency, bank account balances, and highly liquid investments with maturities of three months or less.

- Accounts Receivable: Amounts owed to the company by customers for goods or services sold on credit.

- Inventory: Goods held for sale in the ordinary course of business, including raw materials, work-in-progress, and finished goods.

- Short-term Investments: Marketable securities or other investments with maturities of one year or less.

Non-current Assets

These are assets expected to provide economic benefits beyond one year.

- Property, Plant, and Equipment (PP&E): Land, buildings, machinery, vehicles, and other tangible assets used in operations.

- Intangible Assets: Non-physical assets with no inherent physical form, such as patents, trademarks, copyrights, and goodwill.

- Long-term Investments: Investments in securities, real estate, or other entities intended to be held for more than one year.

- Deferred Tax Assets: Future tax benefits resulting from temporary differences between accounting and tax rules.

Liabilities

Liabilities are obligations or debts owed by a company to external parties, representing claims against its assets. Like assets, liabilities can be current or non-current, depending on their maturity and timing of repayment. Here are some examples:

Current Liabilities

These are obligations expected to be settled within one year.

- Accounts Payable: Amounts owed to suppliers or vendors for goods or services purchased on credit.

- Short-term Borrowings: Loans or credit lines with maturities of one year or less.

- Accrued Expenses: Expenses incurred but not yet paid, such as wages, utilities, or taxes.

- Current Portion of Long-term Debt: The portion of long-term debt due within the next year.

Non-current Liabilities

These are obligations with maturities beyond one year.

- Long-term Debt: Loans, bonds, or other borrowings with maturities exceeding one year.

- Deferred Tax Liabilities: Future tax obligations resulting from temporary differences between accounting and tax rules.

- Lease Obligations: Payments due under operating leases or finance leases.

- Pension Obligations: Obligations related to employee pension plans or other post-employment benefits.

Equity

Equity represents the residual interest in the assets of a company after deducting its liabilities. It reflects the ownership interest of shareholders in the company’s assets and represents the company’s net worth. Equity can be divided into several components, including:

- Common Stock: Shares issued to investors in exchange for ownership rights in the company.

- Additional Paid-in Capital: Amounts received from investors in excess of the par value of common stock.

- Retained Earnings: Accumulated profits or losses retained in the company after dividends have been paid to shareholders.

- Treasury Stock: Shares of the company’s own stock that it has repurchased and is holding in treasury.

- Accumulated Other Comprehensive Income: Unrealized gains or losses on certain financial instruments or other items that are not included in net income.

5. Introduction to Managerial Accounting

Managerial accounting, also known as management accounting, is a branch of accounting focused on providing internal stakeholders within an organization with relevant financial and non-financial information for decision-making, planning, controlling, and performance evaluation. Unlike financial accounting, which primarily deals with reporting to external parties such as investors, creditors, and regulators, managerial accounting is geared towards aiding managers in making informed business decisions to achieve organizational goals.

Budgeting

Budgeting is a critical aspect of financial management that plays a vital role in planning and control. It involves setting financial goals, estimating income and expenses, and allocating resources to achieve those goals.

Budgeting Overview:

- Budgeting is critical for financial management, aiding in planning and control.

- It involves setting financial goals, estimating income and expenses, and resource allocation.

Role in Planning:

- Provides a roadmap for financial activities and resource needs.

- Helps prioritize spending and make informed decisions.

Role in Control:

- Serves as a benchmark for measuring actual performance.

- Allows identification of deviations and corrective actions.

Facilitates Coordination:

- Ensures alignment of departments and teams in financial goals.

- Promotes communication, transparency, and accountability.

Overall Importance:

- Crucial for goal setting, resource allocation, and performance monitoring.

- Enhances financial stability, efficiency, and long-term success.

Budgeting Approaches

There are several approaches to budgeting that organizations can adopt based on their specific needs, objectives, and operational characteristics. Here are some common budgeting approaches

Incremental Budgeting:

- In incremental budgeting, the current budget is adjusted based on changes from the previous period.

- It involves making small adjustments or increments to the existing budget rather than starting from scratch.

- This approach is simple and less time-consuming but may perpetuate inefficiencies or overlook significant changes.

Zero-Based Budgeting (ZBB):

- Zero-based budgeting requires each department to justify its entire budget from scratch, starting with a base of zero.

- All expenses must be justified regardless of whether they were included in previous budgets.

- It encourages cost-consciousness, promotes efficient resource allocation, and can lead to better decision-making.

- However, it can be time-consuming and may require significant effort to implement.

Activity-Based Budgeting (ABB):

- Activity-based budgeting links budgeting to the organization’s activities and processes.

- It involves identifying activities, determining the cost drivers associated with each activity, and allocating resources accordingly.

- ABB focuses on the cost of activities rather than traditional cost centers, providing more accurate cost information for decision-making.

- It helps align budgets with strategic objectives and improves resource allocation efficiency.

Flexible Budgeting:

- Flexible budgeting adjusts the budget based on changes in activity levels or other external factors.

- It allows for variations in revenue and expenses by incorporating flexible parameters or ranges.

- Flexible budgets are particularly useful in dynamic environments where activity levels may fluctuate significantly.

- This approach provides managers with greater flexibility in responding to changes and helps improve budget accuracy.

Rolling Budgets:

- Rolling budgets extend the budgeting horizon beyond the traditional fiscal year, typically covering multiple periods, such as quarters or months.

- As one period ends, a new period is added, ensuring that there is always a fixed budget horizon.

- Rolling budgets facilitate continuous planning and allow organizations to adapt more quickly to changing conditions.

- They provide a forward-looking perspective and encourage ongoing performance evaluation and adjustment.

Participative Budgeting:

- Participative budgeting involves input from various levels of the organization, including department heads, managers, and employees.

- It encourages collaboration, engagement, and ownership of the budgeting process among stakeholders.

- Participative budgeting can lead to more accurate budget estimates, increased motivation, and better acceptance of budget targets.

- However, it may be more time-consuming and require effective communication and coordination.

Each of these budgeting approaches has its advantages and disadvantages, and organizations may choose to combine or adapt them to suit their specific circumstances and objectives. The key is to select the approach that aligns best with the organization’s goals, culture, and operational requirements.

Cost Analysis

Cost analysis, also known as cost accounting or cost management, is the process of examining and evaluating the costs associated with producing goods or services within an organization. It involves analyzing various cost components, identifying cost drivers, and understanding how costs behave under different circumstances.

- The primary purpose of cost analysis is to understand and control the costs of production, distribution, and selling of goods or services.

- It helps managers make informed decisions about pricing, resource allocation, product mix, and process improvement.

Cost Components

- Direct Costs: Costs directly attributable to producing a specific product or service, such as raw materials, labor, and direct overhead.

- Indirect Costs: Costs that are not directly traceable to a specific product or service but contribute to overall production costs, such as factory rent, utilities, and administrative expenses.

- Fixed Costs: Costs that remain constant regardless of production levels, such as rent, insurance, and salaries.

- Variable Costs: Costs that vary in proportion to changes in production levels, such as raw materials, direct labor, and sales commissions.

Cost Analysis Techniques

- Cost-Volume-Profit (CVP) Analysis: Examines the relationship between costs, volume, and profits to determine breakeven points, pricing strategies, and profit targets.

- Variance Analysis: Compares actual costs to budgeted or standard costs to identify discrepancies and investigate the causes of variations.

- Activity-Based Costing (ABC): Allocates indirect costs to products or services based on the activities that drive those costs, providing a more accurate understanding of cost drivers.

- Marginal Costing: Focuses on analyzing the contribution margin of products or services by subtracting variable costs from sales revenue, helping in pricing decisions and product mix optimization.

Benefits

- Cost Control: Enables organizations to identify cost-saving opportunities, eliminate waste, and improve efficiency.

- Decision-Making: Provides managers with relevant cost information for making strategic, tactical, and operational decisions.

- Performance Evaluation: Helps assess the profitability and cost-effectiveness of products, services, departments, or projects.

- Resource Allocation: Guides allocation of resources to maximize profitability and achieve organizational goals.

- Competitive Advantage: Allows organizations to set competitive prices, optimize product offerings, and enhance overall competitiveness in the market.

Cost analysis is essential for effective cost management and strategic decision-making within organizations. By understanding their cost structures and drivers, businesses can optimize operations, improve profitability, and maintain a competitive edge in the marketplace.

Performance Measurement

Evaluating a business’s financial health and operational efficiency requires the use of various metrics and indicators that provide insights into different aspects of its performance.

Financial Health Metrics:

- Profitability Ratios: These ratios measure a company’s ability to generate profits relative to its revenue, assets, or equity.

- Examples: Return on Equity (ROE), Return on Assets (ROA), Gross Profit Margin, Net Profit Margin.

- Liquidity Ratios: These ratios assess a company’s ability to meet its short-term obligations using its liquid assets.

- Examples: Current Ratio, Quick Ratio (Acid-Test Ratio).

- Solvency Ratios: These ratios evaluate a company’s long-term financial stability and its ability to meet long-term obligations.

- Examples: Debt-to-Equity Ratio, Interest Coverage Ratio.

Operational Efficiency Indicators:

- Inventory Turnover: Measures how quickly a company sells its inventory and replenishes it.

- Days Sales Outstanding (DSO): Indicates the average number of days it takes for a company to collect payment from its customers.

- Accounts Payable Turnover: Measures how quickly a company pays its suppliers.

- Asset Turnover: Evaluates how efficiently a company utilizes its assets to generate revenue.

- Operating Cash Flow Ratio: Compares a company’s operating cash flow to its net sales to assess its ability to generate cash from its operations.

Growth Metrics:

- Revenue Growth Rate: Measures the percentage increase or decrease in a company’s revenue over a specific period.

- Customer Acquisition Cost (CAC): Calculates the average cost of acquiring a new customer.

- Customer Lifetime Value (CLV): Estimates the total revenue a company can expect from a single customer over their lifetime.

- Market Share: Indicates the percentage of total market sales a company captures.

Efficiency and Productivity Indicators:

- Employee Productivity: Measures the output per employee, such as revenue per employee or units produced per hour.

- Capacity Utilization Rate: Evaluates how effectively a company is utilizing its production capacity.

- Supply Chain Cycle Time: Measures the time it takes for a product to move through the supply chain from production to delivery.

Risk Management Metrics:

- Beta Coefficient: Measures a stock’s volatility relative to the overall market.

- Volatility: Indicates the degree of variation in a company’s stock price over time.

- Credit Rating: Assesses a company’s creditworthiness and likelihood of defaulting on its debt obligations.

These metrics and indicators provide a comprehensive view of a business’s financial health, operational efficiency, growth prospects, and risk profile. By regularly monitoring and analyzing these metrics, businesses can identify areas of strength, areas needing improvement, and potential risks, enabling them to make informed decisions and drive performance improvement initiatives.

6. Regulatory Environment and Ethics

Accounting Standards

International Financial Reporting Standards (IFRS)

- Developed and maintained by the International Accounting Standards Board (IASB), IFRS is a set of accounting standards used by companies in over 140 countries worldwide.

- IFRS aims to provide a common language for financial reporting, making it easier for investors, analysts, and regulators to compare financial statements across different countries.

- IFRS emphasizes principles-based standards, which provide broad guidelines for reporting transactions and allow for more judgment and interpretation by preparers.

- Key features of IFRS include the focus on fair value measurement, the principle of substance over form, and the use of comprehensive income.

- While IFRS is widely adopted globally, some countries may permit or require adjustments to accommodate local legal or regulatory requirements.

Generally Accepted Accounting Principles (GAAP)

- GAAP refers to the accounting standards, principles, and procedures used in the United States for financial reporting purposes.

- GAAP is established by various standard-setting bodies, including the Financial Accounting Standards Board (FASB) for private companies and the Governmental Accounting Standards Board (GASB) for governmental entities.

- GAAP is rules-based, providing specific guidelines and requirements for financial reporting, which are often more detailed and prescriptive compared to IFRS.

- Key features of GAAP include the historical cost principle, revenue recognition criteria, and specific rules for various industries and transactions.

- While GAAP is primarily used in the United States, many other countries have adopted or converged their accounting standards with IFRS, although some differences may still exist between GAAP and IFRS.

In summary, while both IFRS and GAAP aim to establish consistent and reliable financial reporting standards, they differ in their approach, scope, and application. IFRS is principles-based and used globally, promoting comparability and transparency in financial reporting across borders. GAAP, on the other hand, is rules-based and specific to the United States, providing detailed guidance for financial reporting within the U.S. regulatory framework.

Ethical Considerations

Ethical responsibilities are paramount for accountants as they play a critical role in ensuring the integrity and transparency of financial information. Here’s a discussion of the ethical responsibilities of accountants and the impact of ethical dilemmas on businesses and stakeholders

Ethical Responsibilities of Accountants

- Integrity and Honesty: Accountants are expected to uphold the highest standards of integrity and honesty in their professional conduct. This includes accurately representing financial information and avoiding misleading or deceptive practices.

- Confidentiality: Accountants must maintain the confidentiality of client information and financial data. They should not disclose confidential information to unauthorized parties unless required by law or professional standards.

- Objectivity and Impartiality: Accountants should maintain objectivity and impartiality in their professional judgments and decisions. They should avoid conflicts of interest and refrain from actions that could compromise their independence or impartiality.

- Professional Competence and Due Care: Accountants are expected to possess the necessary knowledge, skills, and expertise to perform their duties competently. They should stay updated on relevant accounting standards, laws, and regulations and exercise due care in their work.

- Professional Behavior: Accountants should conduct themselves in a professional manner and adhere to ethical codes of conduct established by professional organizations, such as the American Institute of Certified Public Accountants (AICPA) or the International Federation of Accountants (IFAC).

Impact of Ethical Dilemmas on Businesses and Stakeholders

- Reputation Damage: Ethical lapses or scandals involving accountants can tarnish the reputation of businesses and erode trust among stakeholders, including investors, customers, and the public.

- Financial Losses: Ethical breaches can lead to financial losses for businesses, including legal fees, fines, penalties, and damage to shareholder value. Misstatements or fraudulent practices can also result in financial restatements and loss of investor confidence.

- Legal and Regulatory Consequences: Ethical violations may result in legal and regulatory scrutiny, investigations, and enforcement actions. This can lead to legal liabilities, fines, sanctions, and regulatory intervention, impacting the financial and operational stability of businesses.

- Employee Morale and Retention: Ethical dilemmas can undermine employee morale and engagement, leading to decreased productivity, increased turnover, and challenges in attracting and retaining talent.

- Stakeholder Trust and Relationships: Ethical lapses can damage trust and relationships with stakeholders, including customers, suppliers, lenders, and employees. This can affect business partnerships, customer loyalty, and overall stakeholder confidence in the organization.

Adherence to ethical principles is essential for accountants to maintain trust, integrity, and professionalism in their roles. Ethical dilemmas can have far-reaching consequences for businesses and stakeholders, highlighting the importance of ethical awareness, accountability, and ethical decision-making in the accounting profession.

7. Using Accounting Software

Overview of Accounting Software

Accounting software is crucial for businesses and individuals to manage their finances efficiently, automate tasks, and ensure accuracy in their financial reports. There are several popular options available, catering to a wide range of needs, from small businesses to large enterprises, and even individuals seeking to keep track of their personal finances. Here’s an overview of some popular accounting software options:

1. QuickBooks

- Target Users: Small to medium-sized businesses.

- Key Features: Invoice management, expense tracking, payroll processing, and financial reporting. QuickBooks also offers cloud-based solutions and integrates with numerous third-party applications.

- Platforms: Desktop and online.

2. Xero

- Target Users: Small to medium-sized businesses.

- Key Features: Real-time financial reporting, invoicing, bill payments, inventory management, and payroll. Xero is cloud-based and emphasizes ease of use and integration with a wide range of third-party apps.

- Platforms: Online.

3. FreshBooks

- Target Users: Freelancers, small businesses, and project-based businesses.

- Key Features: Simplified invoicing, expense tracking, time tracking, and project management. FreshBooks is designed for service providers who need easy-to-use, cloud-based accounting software.

- Platforms: Online.

4. Sage 50cloud

- Target Users: Small to medium-sized businesses.

- Key Features: Accounting, inventory management, project management, payroll, and payment processing. Sage 50cloud combines the reliability of desktop software with cloud mobility.

- Platforms: Desktop with cloud integration.

5. Wave

- Target Users: Small businesses and freelancers.

- Key Features: Free financial software offering invoicing, accounting, and receipt scanning. Wave is particularly attractive for small businesses looking for affordable, basic accounting solutions.

- Platforms: Online.

6. Zoho Books

- Target Users: Small to medium-sized businesses.

- Key Features: Invoicing, expense tracking, inventory management, and workflow automation. Zoho Books is part of the Zoho suite, offering extensive integration with other Zoho products and third-party applications.

- Platforms: Online.

7. Microsoft Dynamics 365

- Target Users: Medium to large enterprises.

- Key Features: Financial reporting, supply chain management, sales and service management, and project management. Microsoft Dynamics 365 is a comprehensive ERP and CRM solution that integrates deeply with other Microsoft products.

- Platforms: Online and desktop for some components.

8. SAP Business One

- Target Users: Small to medium-sized enterprises.

- Key Features: Financial management, sales and customer management, purchasing and inventory control, and business intelligence. SAP Business One is designed for businesses that need a robust, scalable solution.

- Platforms: Desktop and cloud (through partners).

9. Quicken

- Target Users: Individuals and households.

- Key Features: Personal finance management, budgeting, investment tracking, and bill management. Quicken offers desktop and cloud-based financial management tools tailored to personal use.

- Platforms: Desktop and online.

10. Mint

- Target Users: Individuals.

- Key Features: Free personal finance and budgeting software. Mint helps users track their spending, create budgets, monitor investments, and provides credit score information.

- Platforms: Online and mobile app.

Each of these accounting software options has its own set of features, advantages, and target users. The choice between them depends on specific business needs, the size of the organization, and personal preferences for cloud-based versus desktop applications.

Benefits of Using Software

Accounting software plays a vital role in modern business operations by streamlining financial processes, reducing errors, and providing valuable insights through advanced reporting features. Here’s a detailed look at how these benefits unfold:

Streamlining the Accounting Process

- Automation of Routine Tasks: Accounting software automates repetitive tasks such as invoicing, bill payments, and payroll processing. This automation not only saves time but also reduces the likelihood of human error in data entry and calculations.

- Integration with Other Systems: Many accounting solutions can integrate with other business systems like banking, e-commerce, and customer relationship management (CRM) platforms. This integration facilitates real-time data exchange, ensuring that financial records are always up to date without manual intervention.

- Improved Data Management: With digital record-keeping, businesses can organize and store financial data more efficiently. Accessing historical financial information becomes easier, supporting better decision-making and faster response to audits or inquiries.

Reducing Errors

- Accuracy in Calculations: Software reduces errors in financial calculations through precise algorithms, ensuring that tasks like tax calculations, payroll, and expense tracking are done correctly.

- Consistency: Accounting software ensures that all financial data is recorded and processed consistently, following the same rules and formats, which minimizes discrepancies and improves the reliability of financial data.

- Real-time Error Detection: Many programs offer real-time alerts for inconsistencies or errors, such as duplicate entries or deviations from budgeted amounts. Early detection allows for immediate corrections, preventing small errors from becoming bigger issues.

Providing Valuable Insights through Reporting Features

- Customizable Reports: Users can generate a variety of financial reports (e.g., profit and loss statements, balance sheets, cash flow statements) tailored to their specific needs. This customization enables businesses to focus on key metrics that matter most to their operations.

- Trend Analysis and Forecasting: Advanced reporting features include trend analysis and forecasting tools that help businesses predict future financial performance based on historical data. This predictive insight supports strategic planning and decision-making.

- Accessible Financial Overview: Dashboards provide a real-time overview of a company’s financial health, displaying key metrics such as outstanding invoices, expenses, and cash flow at a glance. This accessibility helps business owners and financial managers make informed decisions quickly.

- Compliance and Audit Readiness: By maintaining accurate and up-to-date financial records, accounting software helps businesses comply with regulatory requirements and tax laws. The software can also streamline the audit process by organizing financial data and supporting documents in an easily accessible format.

Accounting software enhances the efficiency and accuracy of financial management practices. By leveraging automation, integration, and advanced reporting capabilities, businesses can not only save time and reduce errors but also gain deeper insights into their financial performance, enabling better strategic planning and growth management.

8. Practical Tips for Beginners

For beginners venturing into the world of accounting, whether for personal finance management or handling a small business’s finances, starting on the right foot is crucial.

Staying Organized

- Digital Record-Keeping: Use accounting software or cloud-based services to keep your financial records digitized. This approach not only reduces physical clutter but also makes it easier to search and retrieve information when needed.

- Regular Updates: Make it a habit to update your financial records regularly. This could mean daily, weekly, or monthly, depending on your activities. Regular updates prevent backlogs and help you stay on top of your finances.

- Categorize Transactions: Organize your transactions into categories (e.g., utilities, payroll, inventory purchases). This practice simplifies tracking expenses and income, making it easier to understand where your money is going.

- Backup Your Data: Ensure you have regular backups of your financial data, preferably in multiple locations (e.g., cloud storage and an external hard drive). This safeguards against data loss due to technical failures or cyber incidents.

Learning Resources

- Books: Start with foundational books such as “Accounting For Dummies” by John A. Tracy, which offers a broad overview of basic accounting principles in an accessible format. For those interested in personal finance, “The Total Money Makeover” by Dave Ramsey provides a strong foundation for managing personal finances.

- Online Courses: Platforms like Coursera, Udemy, and Khan Academy offer courses ranging from introductory accounting to more specialized topics. Look for courses with high ratings and reviews to ensure quality learning.

- Websites and Blogs: Websites like Investopedia, AccountingCoach, and the AICPA (American Institute of Certified Public Accountants) offer a wealth of free articles, tutorials, and resources for both beginners and advanced learners.

- Networking and Forums: Join online forums (e.g., Reddit’s r/accounting or r/personalfinance) and professional networks (like LinkedIn groups) to ask questions, share experiences, and get advice from peers and professionals.

- Recognizing the Need: If you find yourself overwhelmed by tax regulations, complex financial transactions, or planning for business growth, it might be time to seek professional advice. Additionally, if you’re spending more time on accounting than on your business or personal goals, consider outsourcing.

- Choosing the Right Professional: Look for certified professionals, such as Certified Public Accountants (CPAs) or certified financial planners (CFPs), depending on your needs. Check their qualifications, experience, and client reviews.

- Consultations: Start with a consultation to discuss your needs and expectations. Many professionals offer free initial consultations, which can help you gauge whether they’re the right fit for you.

- Referrals and Research: Ask for referrals from colleagues, friends, or family members who have used similar services. Research local professionals online and pay attention to their areas of expertise and client feedback.