A Tax Break for the Little Ones: The Kiddie Tax and How It Works

The what, why, and how

Why care about the kiddie tax?

Well, the first $2,200 of a dependent child’s investment income has the potential to be taxed at a rate much lower than yours, the parent’s tax rate.

For parents who want to transfer wealth to the child, kiddie tax acts as a double-edged sword, motivating (yeah! enjoy the lower rate!) and discouraging (watch out, the parent’s rate will be applied once over the threshold) at the same time.

This article will first bust some common myths about the kiddie tax and then move on to the calculation.

What is the Kiddie Tax? Does it Apply to You?

Kiddie tax applies to the unearned income of your dependent children. The main point is that the unearned income of children greater than $2,200 (for the year 2021) will be taxed at the parents’ rate. The kiddie tax was designed to discourage wealthy families from taking advantage of children’s lower tax rates by transferring assets to the next generation.

If you are interested in the details, please read Topic №533 from the IRS.

Here I will explain the specifications in an easier-to-digest manner.

There is a couple of myths relating to the kiddie tax.

Myth №1: Age

The word “kiddie” gives us the impression that this rule is only relevant for very young children.

In fact, the kiddie tax has a much higher age ceiling: 19 or 24.

- Age ceiling 1: child under age 19 (not including 19) at the end of the tax year who is living with a parent. If your child who lives with you turns 19 in November 2021, the Kiddie tax is no longer relevant for the year 2021. OR

- Age ceiling 2: child who is a full-time student (older than 19 and younger than 24)

Also, the child must be a dependent, and at least one of the parents was alive.

Myth №2: Earned income and unearned income

The kiddie tax only applies to unearned income. Earned income such as wages and salaries is always taxed at the child’s rate (after considering the standard deduction).

Unearned income here means interest, dividends, and realized capital gains, which generally appear when parents open a custodial account (UTMA/UGMA) for the kid.

How to remember this? Go back and think about the purpose of the kiddie tax. The goal is to discourage excessive wealth transfer, not about kids cutting lawns to make some income.

How to calculate the kiddie tax?

If the child only has unearned income (no earned income), the calculation (at least for exams) is very straightforward.

Example 1: Bella, a 12-year-old daughter of the Lee family, had $3,000 of unearned income in year 2021. Bella had no earned income this year.

(Apparently, the 12-year-old Bella has more investment wisdom than me this year.)

The first $1,100 of Bella’s unearned income is untaxed (standard deduction for unearned income).

The next $1,100 would be taxed at Bella’s tax rate. The specific rate depends on the type of unearned income, which is beyond the scope of this discussion.

The remaining $800 ($3,000 — $1,100 — $1,100) is taxed at Bella’s parent’s tax rate, which is more likely to be higher than Bella’s rate.

So the total taxable (unearned) income in this case is $1,900 ($1,100 and $800 or $3,000 — $2,200).

If the child has both earned income (EI) and unearned income (UI), things can get a tiny little bit more complicated due to deductions.

Example 2: Lisa, a 17-year-old daughter, had $3,000 of unearned income and $2,500 earned income from walking neighbors’ dogs.

How much of Lisa’s income will be taxed at her parent’s rate?

$800. Easy, the steps are the same as in Example 1 since earned income is never taxed at the parent’s rate. It’s irrelevant here.

What is Lisa’s standard deduction?

When a child only has unearned income, the standard deduction is $1,100. In other words, the first $1,100 of unearned income is not taxed.

Once we add earned income into the mix, the standard deduction for a dependent child changes to “the greater of: (1) $1,100, or (2) your earned income plus $350 (but the total can’t be more than the basic standard deduction for your filing status).” See the source page for details.

Mathematically, I prefer to write it out like this: max(1,100, EI +350, 12,550).

For Lisa’s case, her standard deduction (SD) would be $2,500 + $350 = $2,850, since $2,850 is greater and $1,100.

How much of Lisa’s income will be taxed at Lisa’s tax rate?

Lisa’s taxable income is $2,650 (EI + UI — SD, which is $3,000 + $2,500 — $2,850 in our case). Out of the $2,650, $800 is taxed at the parent’s rate (see Example 1), and the remainder $1,850 is taxed at Lisa’s rate.

Should you open a custodial brokerage account for your child?

I wrote about different options for contributing to your child’s education funds in my previous post.

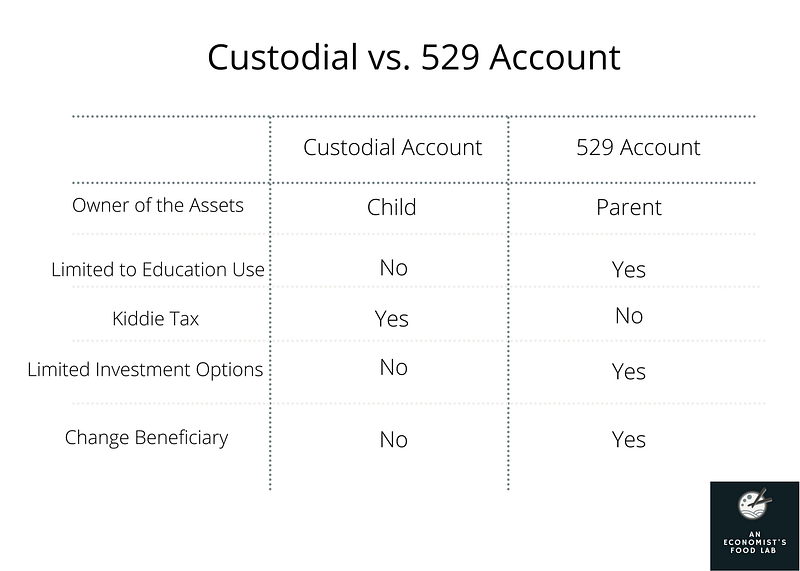

A custodial account is one of the common methods to help your child out financially. Is this the best way to save for education? That depends on your specific purpose and situation. Here I point out a few major differences between a custodial account (UTMA/UGMA) and the popular 529 account. See the table below for a summary.

A custodial account can also serve as a great educational tool if you want to teach your child about investment and saving. That’s how I plan to use this account for.

This article is for informational purposes only. It should not be considered Financial or Legal Advice. Consult a financial professional before making any important financial decisions.

Please consider signing up for Medium using my affiliate link if you would like to read more of my articles. Thank you for supporting my writing!😄