A Play on Underbuilt Housing In America: Builders FirstSource (BLDR)

Investment Thesis

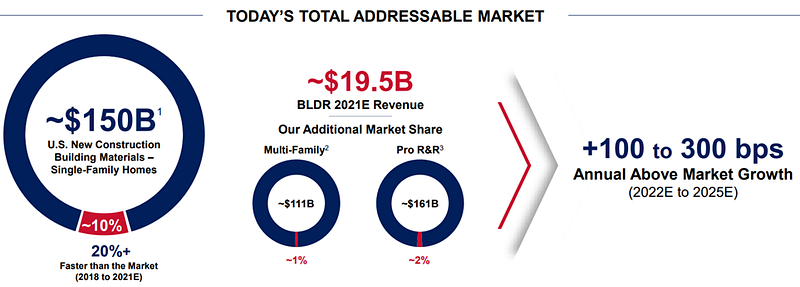

Based on data showing that the U.S. is experiencing a housing shortage, I believe that the homebuilding boom will continue as homebuilders work to meet demand while experiencing challenges with supply chain, labor, and higher cost of materials. Builders FirstSource, the largest homebuilding materials supplier, is a great way to gain exposure to a booming industry as it is a less capital-intensive business in comparison to homebuilders. Given its market share growth surpassing overall market growth, focus on vertical integration, excellent free cash flow generation, strong balance sheet, and numerous macro tailwinds, Builders FirstSource has a strong value proposition and is worth gaining exposure to.

Industry Overview

Builders FirstSource is a homebuilding material manufacturer and supplier. Some of its competitors include Cornerstone Building Brands (CNR), Louisiana-Pacific (LPX), and Huttig Building Products (HBP). These companies build and sell home building products such as windows, roofs, wall panels, stairs, insulation, etc.

Macro Tailwinds

· 45 million millennials in prime first-time home buying ages of 26 to 35 in 2022.[1]

· Gap between single-family home construction and household formation grew to 5.24 million homes as of June 2021.[2]

· Between 2015 and 2020, the average rate of household formation was 1.5 million households per year, while the average rate of home completion was 806,000 homes per year.[3]

If building and household formations were to continue at this rate, the gap between these metrics would never close.

· Assuming household formations continue at current 5-year average, the average rate of home completion would have to triple to close the gap in home completions and household formations in 5 to 6 years.

· Currently, housing inventory is still down 40% from pre-COVID levels, contributing to price appreciation.[4]

· Homebuilding during the past year stalled due to increased costs of materials. Elevated home prices priced some buyers out of the market. As supply chains begin to decongest, cost of materials will come back down, and home sales growth should be more moderate in the next few years.

· “With economic growth expected to sustain the purchasing power of eager homebuyers, we expect the median home sales price to continue to increase, rising 2.9% in 2022, a notably more moderate pace. As builders ramp up production to meet demand, home buyers will grapple with higher monthly costs due to rising prices and rising mortgage rates. Affordability challenges will keep prices from advancing at the same pace we saw in 2021 even as ongoing supply-demand dynamics mean prices continue to grow nationwide.”[5]

· Nearly 75% of homeowners are considering at least home-improvement project in the next year.[6]

Company Overview

Business Model

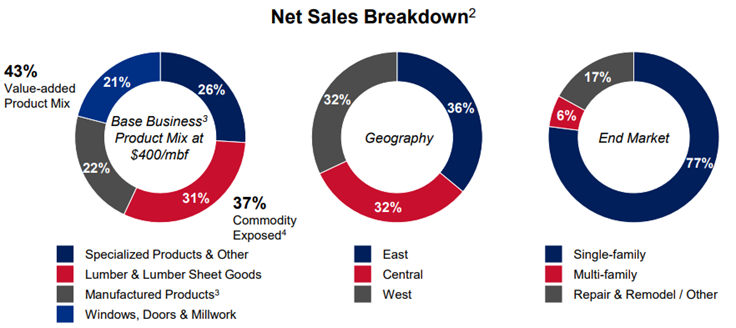

Builders FirstSource operates 580 locations in 42 states and offers an integrated solution to customers by providing five product categories and two services:

· Lumber & Lumber Sheet Goods

· Manufactured Products

· Windows, Doors & Millwork

· Gypsum, Roofing & Insulation

· Sliding, Metal, and Concrete

· Distribution Services

· Installation Services

Builders FirstSource’s customer base includes:

· Large production builders

· Small custom homebuilders

· Multi-family builders

· Repair/remodeling contractors

Approximately 91% of U.S. single-family housing permits in 2020 were issued in geographical areas in which Builders FirstSource operates.

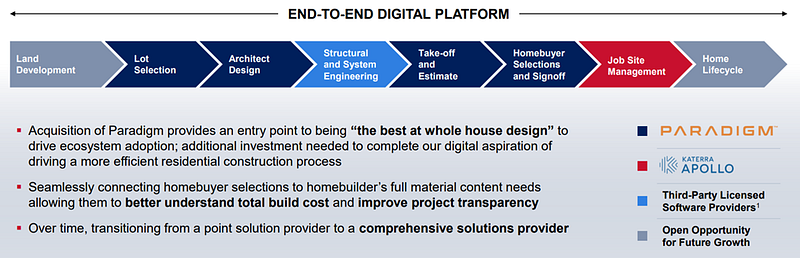

While the homebuilding industry is quite fragmented, Builders FirstSource is developing a vertically integrated approach that allows them to compete through comprehensive product lines, value-added services, and an end-to-end digital platform. Their investments in its digital platform will be discussed in more specificity later.

In addition, Builders FirstSource’s use of offsite manufacturing allows them to save time and costs for customers.

- 223 hours of labor saved per house

- 14.5 cubic yards of less waste per house

- 5,600 board feet (27%) saved per house

- 2.5 days saved in framing time per house

Competition

Builders FirstSource’s competition is mainly smaller, privately-owned local businesses that do not have the same resources available as Builders FirstSource. For instance, Builders FirstSource has wide access to capital, sophisticated IT systems and larger control over its own supply-chain. Since Builders FirstSource is the largest customer for most of its suppliers, it has significant purchasing leverage. In FY2020, no purchases from any single supplier represented more than 6% of total materials purchases. This diversification in suppliers allows Builders FirstSource to source materials without reliance on any single supplier.

Strategy for Expansion/Growth

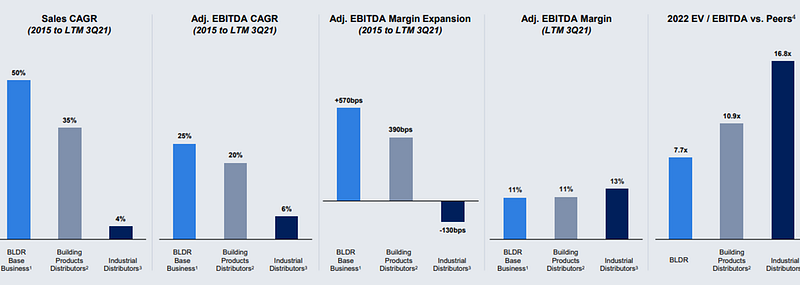

When I think about Builders FirstSource, it really is the textbook example of GARP (growth at a reasonable price). It’s growing revenue at a 23.2% CAGR (compounded annual growth rate) over the past five years and growing net income at a 62% CAGR over the same period.

There are three main sources of growth for Builders FirstSource in the future.

· Macroeconomic Tailwinds

· Mergers and Acquisitions (M&A)

· Expansion in Digital Platforms

We’ve already gone over the macro tailwinds in the homebuilding industry, so I’ll go over Builders FirstSource opportunities in M&A and digital expansion.

Mergers and Acquisitions (M&A)

Builders FirstSource has been a M&A monster. Their main goal with acquisitions is to expand their geographical reach, add more value-add products/services and further technological advancement. In the words of their CEO, Dave Flitman:

“Moving forward, we will continue to reinvest in our business to accelerate organic growth while actively pursuing accretive tuck-in M&A opportunities to improve our mix and build scale in key growth markets. We firmly believe the strength of our balance sheet and cash flow generation will allow us to remain a disciplined consolidator in this industry.” — Dave Flitman, BLDR CEO

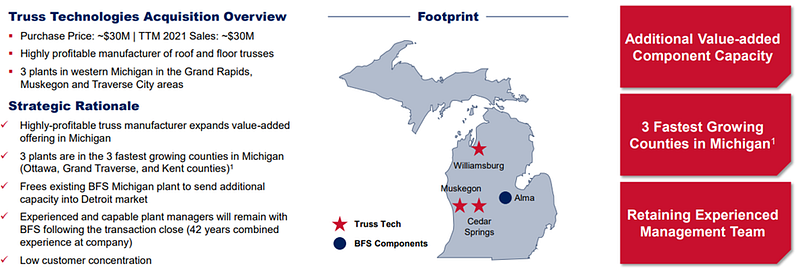

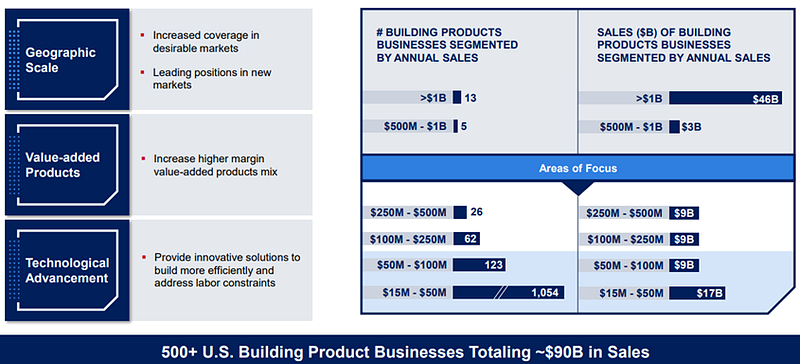

As seen below, Builders FirstSource owns a massive number of businesses. Granted, most of these businesses are small, most of the homebuilding businesses are locally operated, which gives Builders FirstSource the opportunity to gain regional market dominance.

Expansion in Digital Platforms

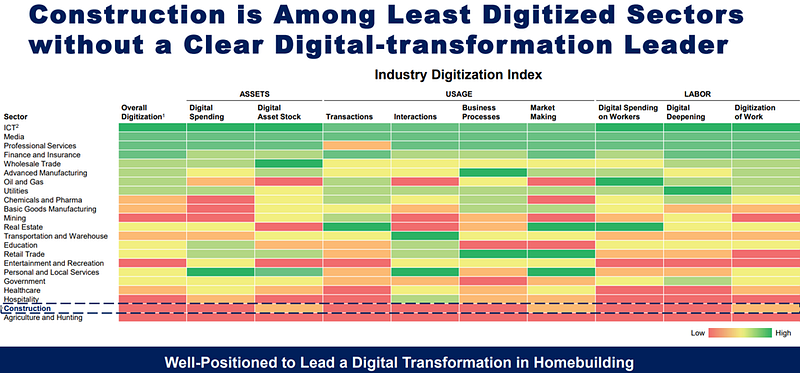

As seen in the table above, the construction industry is one of the least digitized sectors and lacks a true ‘leader’ in digitization. Over the coming years, Builders FirstSource aims to:

· Uniquely positioned to be the driver of digital transformation

· Be at the center of the homebuilding ecosystem

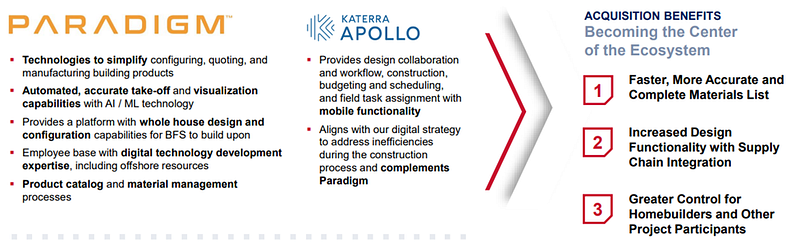

Builders FirstSource aims to accelerate their digital transformation through two acquisitions: Paradigm and Katerra Apollo.

Paradigm is a software solutions provider that will be able to:

“Create a better home buying experience, but they will also benefit Builders FirstSource’s customers and supply partners by ensuring better alignment and integration throughout the homebuilding project lifecycle. Acquiring Paradigm will provide tools to make it even easier to do business with Builders FirstSource.

Establishing digital solutions leadership for the homebuilding industry is expected to drive growth and efficiency for Builders FirstSource’s distribution network by enabling it to align with customers efficiently and seamlessly and better support the entire homebuilding construction process.” — Acquisition Press Release

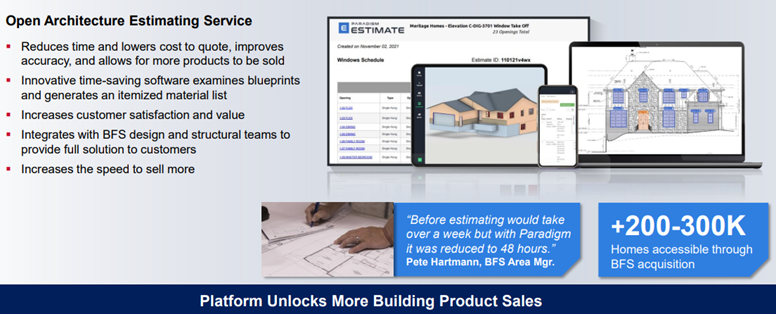

The main two sources of value-add for the Paradigm acquisition is its quoting software and virtual home design software. Paradigm’s quoting software allows omni-channel solutions that integrates dealer sales, online sales, in-store sales, and in-home sales. This will increase capital efficiency while also reducing SG&A (selling, general, and administrative expenses).

On the other hand, the home visualization software will accelerate the sales cycle, and lower the cost to quote a project since the software is integrated with the quoting software.

According to a study by Google, 67 percent of homebuyers said they want a virtual tour. More than 70 percent of new construction buyers in a Zillow study said 3D tours, rather than still photographs, would help them feel better about a space — up from 51 percent a year ago.

The same Zillow study also found 56 percent of new construction buyers felt they wasted time looking at properties they would have dismissed had they fully understood the floor plan. And 74 percent of new construction buyers agreed or somewhat agreed that “a dynamic floor plan allowing them to connect photos to a specific part of the house would help them determine if the home is right for them.”

The goal here is to improve the customer relationship and make a typically complicated process as smooth as possible. Paradigm’s virtual design software allows homebuyers to choose interior and exterior features online, 3D walkthroughs, virtual neighborhood tours, and lot selection in real-time.

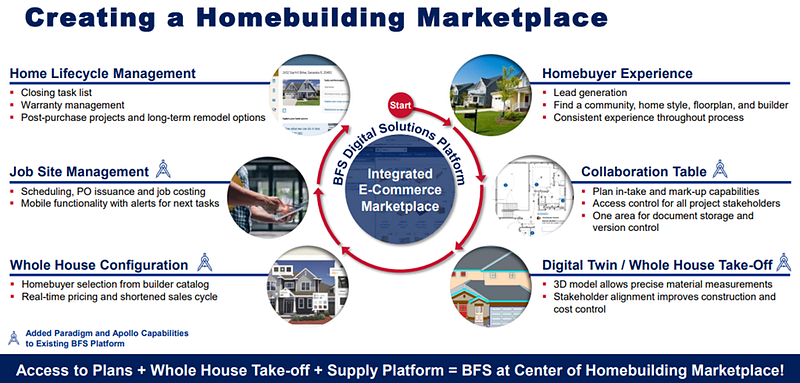

The ultimate goal with these digital platform acquisitions is to build a vertically integrated e-commerce marketplace in addition to their current product/service offerings. I believe that Builders FirstSource is well-positioned to make this a reality.

By expanding its digital platforms, Builders FirstSource will be able to improve:

Homebuyer Experience

· Ability to visualize design ideas

· Design dream home online with an extensive product offering

· Immediately able to gauge cost implications of different design choices

Homebuilder Experience

· Shorter design cycle with fewer manual tasks and reduced cost

· Increased efficiency in construction and less material waste

Supply Partner Experience

· Lower cost channel for bringing products to market

· Ability to reach and influence homebuyers through visualization software

· Operation efficiencies

· Improved business insights

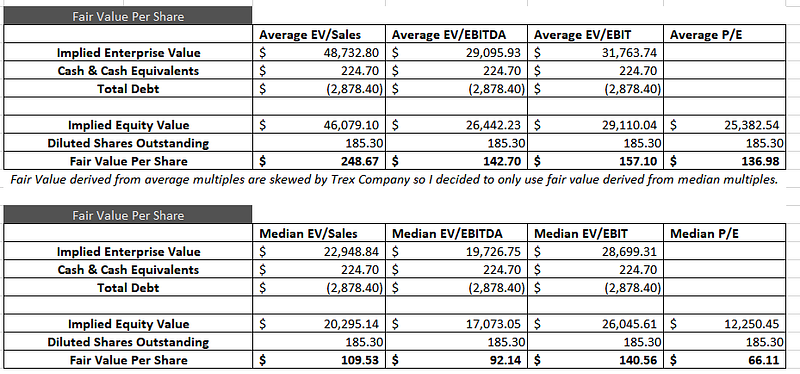

Valuation and Financial Overview

In my comparable companies analysis, given BLDR’s growth rate guidance and its first-mover advantage in construction digitization, I believe BLDR is cheap given the numerous growth verticals. Add on a projected free cash flow of $6 billion from 2021–2025 and a current market cap of ~$12.4 billion…

As of market close on March 14th, BLDR is trading at 5.79x forward EV/EBITDA and 7.51x forward earnings.

BLDR’s capital efficiency is impressive as well with 43.6% Return on Common Equity, 22.2% Return on Capital, and 13.2% Return on Total Assets.

A quick look at BLDR’s balance sheet shows us that it has been working hard to reduce its leverage. In a rising interest rate environment, this is great news. Management is also aggressively reinvesting into the business while aggressively repurchasing shares, which will increase shareholder value and contribute to increased EPS growth. With a $1b repurchasing program planned in 2022, this is equivalent to roughly 7.2% of the current market cap.

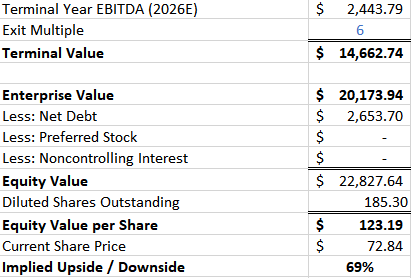

I have linked my DCF and Comps here. Based on my projections, I believe there is significant upside in Builders FirstSource over the years to come. Let me know what your thoughts on the housing market and Builders FirstSource in the comments! Thanks for reading :)