A Minimalistic and Sustainable Investment Approach for Millenials

The path to financial independence with passive investing that considers its environmental impact

Independent from or dependent on your monthly income — what would you choose?

To me, the idea of working full-time for 40 years until 67 (quite possibly longer) and then retiring is not something I strive to accomplish. I imagine having enough money and time but not being able to make use of it due to a lack of health to be the worst kind of prison for me.

I would rather be happy with less but be able to spend more time doing the things I enjoy (well, the best case would be to get paid for that as well, of course.) Those activities might be traveling, spending time with friends and family, surfing, helping others, doing sports, reading, and writing. I dream of not being forced to go to work anymore. Luckily, there exists a concept to counter the work-then-retire approach to life. This concept is known under the FIRE movement:

“The FIRE (Financial Independence, Retire Early) movement is a lifestyle movement whose goal is financial independence and retiring early.”

“Financial independence is the status of having enough income to pay one’s living expense for the rest of one’s life without having to be employed or dependent on others.”

— Wikipedia

Note that we are talking about financial independence and not financial freedom. Financial freedom is reached when your income covers not only your living expenses but also all the luxuries you fancy, and, therefore, is much harder to attain.

What follows is a set of rules and techniques you need to implement to become financially independent. And the best is: these rules and procedures are available to everyone, and you do not need specific skills to apply them.

The Hamster Wheel and How to Get Out

The basic rule for becoming financially independent is quite simple and common sense:

You have to spend less that you earn and save the difference.

That’s it. That’s the trick.

What sounds quite easy, is quite hard due to our lifestyle inflation. Often when our income grows, we think we deserve more — a bigger car, the newest iPhone, a new laptop, or even a bigger house. That often leads straight into consumer debt, aka the worst kind of debt because it has no financial return.

This is the reality of the hamster wheel: We buy sh*t we don’t need with money we don’t have to impress people we don’t like. Then we have to work more to get back the money that we didn’t have, and the cycle begins again.

So how to get out of the hamster wheel?

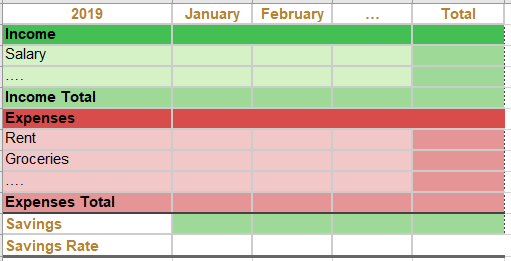

Start a Book of Household Accounts

First things first: You need to have an overview of how much money is coming in and how much money is going out. My approach is a Google Drive Spreadsheet.

The first column shows the different income and expense categories, and each column shows the month. After adding all income streams and expenses, you can calculate the savings and then the savings rate.

Then every week, you go over your receipts and online banking accounts put in what you paid and add it up. The grocery cell after three runs to the store could look like this =30+20+45, showing that you spend 95 bucks on groceries in January so far.

This simple and easy technique has saved me plenty of money already because it finally shows where my money goes. For example, I learned that I spend more money eating out than on groceries and cooking at home. This was the first habit I had my eyes on to save more money.

Trust me, the first month will be eye-opening, and it will make fun to see where you can save some more to drive up your savings rate.

The savings rate ultimately determines how fast you will reach financial independence.

How much money do you need?

Once you got the basics down, spend less than you earn, and you save the rest, you can start thinking about what amount of money you need to be financially independent.

The short answer is: you will need 25 times your yearly expenses.

The work Determining Withdrawal Rates Using Historical Data from William Bengen is fundamental for this rule of thumb. He determined that 4% is the safe withdrawal rate (adjusted for inflation) from an investment portfolio that invests 50% in stocks and 50% in medium-term government bonds.

So, if you can spend 4% of your wealth every year (this is 1/25th of your fortune), you will need 25 times your annual expense in your account to cover them year after year for 30 years.

Imagine you need $1,500 a month to cover your necessary expenses — that would 12*1,500 = $ 18,000 a year. According to the 4% rule, you will need an investment portfolio of $450,000 to quit your job and live financially independent.

Depending on where you live, that is probably the price of a lovely house and car. So we can argue that the goal of financial independence is achievable. Here you can find a calculator that helps you calculate when you can be financially independent.

Of course, we calculate here with a rule of thumb based on historical data from William Bengen in his Trinity Study. Future developments in financial markets might be different. But note a few things:

- You can always adjust your expenses when the value of your portfolio drops.

- Financial independence does not mean you will never work anymore. It means you do not have to work anymore. But if sh*t hits the fan and your portfolio loses significantly in value, you can still go back to work and increase your income.

- As millennials, we have time on our side. If the value of your portfolio drops by 30–50% in a significant financial crisis, we can sit it out until the market recovers. Additionally, you can be happy to buy your shares at meager prices.

How do you get there?

By now, you should have understood that to reach financial independence, you’ll need to spend less than you earn, save the rest and, that you will need about 25 times your yearly expenses.

Make saving easy — automate it.

It is hard to look after your money when there is always something shiny, something new you want to buy. So, the easiest way to save yourself from spending the money is to automate the saving.

When your salary comes in, you set an automatic transfer that transfers a set amount of your savings account. That’s the money you can instantly access when you get in trouble, or other unforeseen circumstances happen. A good rule of thumb is to save for 3–6 months’ worth of salary. If you earn $2,000, you should have $6,000–12,000 in your savings account before starting to invest.

When you are ready to invest, you can put another automation in your banking account that transfers part of what you want to save into your investment account.

Investing is hard — so why not do it automated and passively.

The investment world is enormous, and you would need to do some severe self-study and read some books to understand futures, dividends, fonds, bonds, and so on.

Before starting to invest, you need to decide two things:

- When do you want to retire? This determines your time horizon in which you can go without the money you invest. My goal is to retire at age 45, which means I have a 19-year time horizon.

- How much risk can you take? This determines what financial products you should consider. If you are more into risk and you think you can handle volatility well, you should invest heavily in stocks. If not, you should take a more conservative approach and look into less risky products like bonds.

Then you have to start implementing, and you have two choices again:

- Get yourself an independent financial advisor: Note that this should never be your bank. They will sell you whatever will fill their pockets. Financial advice should never be free; otherwise, it’s just a sales talk.

- Learn and become a do-it-yourself investor: That’s what I did and what made me choose to invest in ETFs (Exchange Traded Funds) passively.

ETFs are investment funds that track the development of a stock index. You can, for example, buy an ETF that represents the S&P 500 or the MSCI World. There are plenty of online banks that offer ETF saving schemes — mine is flatex from Germany. When choosing an online bank, you should look into trading costs for ETFs, and if they allow ETF saving plans that do not cost you any transfer costs.

The advantages of ETFs are huge:

- With little money, you get access to invest in many companies, which diversifies your portfolio heavily and thereby makes it less risky. With some ETFs, you invest your money in 3.000 different companies all over the world. The probability that all go bankrupt is quite low.

- They are very cheap. While you might pay 1–2 % for an actively managed fund, most ETFs are very affordable, often with a total expense ratio of 0,5% or less.

- Historical data shows that only a few fond managers manage to beat the market by stock picking. Thus, ETFs are a great way to “let your money work” while paying the same as traditional fonds in the long-term.

- You can start investing in ETFs monthly, starting at $25 with some online banks.

- ETFs can be bought automatically (which saves you transaction costs), and if you want to sit out a month or more, that’s also no problem at all.

Social Impact Investment — think about your future.

When choosing the ETFs you want to invest in as millennials, you should also consider your future. Do you want to invest in coal and oil and other climate change inducing industries?

Luckily, there are ways to adapt to your investment strategy. For example, if you want to invest in the MSCI World, you also have the option to go for the MSCI World ESG. ESG stands for Environmental, Social, and Governance. Thereby you leave out oil, tobacco, or weapon-producing companies that do not meet the ESG standards.

There are thousands of different ETFs for all kinds of industries. For example, one ETF that I invest in consists of companies that build sustainable energy solutions. This approach is riskier because it’s less diversified. However, I think that if in 19 years sustainable energy sources not become mainstream, I will have other problems than some money lost.

Your System in Place

If you have made it until here, congrats. You know now: how to budget your money, how much you need to retire early, how to automate your savings, and how to automate your investments. You are a passive investor now.

If you have used the calculator above, you might have noticed that financial independence is achievable. But to be able to retire at the age of 40, you will need to save a lot of money in your portfolio.

This is now a question of lifestyle. Do you always want the new and shiny things that advertising is telling you to buy? Then you will have to work your whole life until the average retirement age.

If you choose to opt-out of the hamster wheel, by adopting a more minimalistic or even frugalistic approach to living more productive with less, you will have an excellent chance to become financially independent earlier and live on your terms.

By the way, a robust investment portfolio or some money on the bank means you have the option to adopt a part-time job or take a year off the job. Financial independence does not necessarily force you to retire early (in fact, that might even be boring to retire early). But to conclude, there are plenty of options available by not being dependent on a monthly income anymore.

Please note that these are my personal views on how to reach financial independence, and they are not professional investment advice.