A Comprehensive Guide to Value at Risk (VaR) Calculation

Value at Risk (VaR) is a widely used risk measure in finance that quantifies the potential loss of an investment or portfolio over a specified time horizon and at a given confidence level. It provides a single number that represents the maximum loss an investor can expect to experience under normal market conditions. VaR is an essential tool for risk management, portfolio optimization, and regulatory compliance.

In this tutorial, we will explore the concept of VaR and learn how to calculate it using Python. We will start by understanding the theory behind VaR, then move on to implementing different VaR calculation methods. We will use real financial data to demonstrate the calculations and visualize the results.

Table of Contents

- Understanding Value at Risk

- Historical VaR

- Parametric VaR

- Monte Carlo VaR

- Comparing VaR Methods

- Conclusion

1. Understanding Value at Risk

Value at Risk (VaR) is a statistical measure that estimates the potential loss of an investment or portfolio over a specified time horizon and at a given confidence level. It provides a way to quantify the downside risk of an investment and helps investors make informed decisions about risk management and portfolio allocation.

VaR is typically expressed as a negative dollar amount, representing the maximum loss an investor can expect to experience with a certain level of confidence. For example, a VaR of $1 million at a 95% confidence level means that there is a 5% chance of losing more than $1 million over the specified time horizon.

There are several methods for calculating VaR, each with its own assumptions and limitations. In this tutorial, we will explore three commonly used VaR calculation methods: Historical VaR, Parametric VaR, and Monte Carlo VaR.

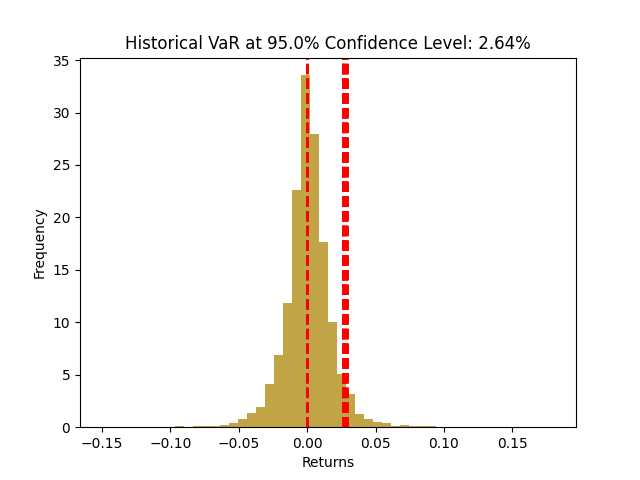

2. Historical VaR

Historical VaR is a non-parametric method that uses historical price data to estimate the potential loss of an investment or portfolio. It assumes that future returns will follow the same distribution as past returns and calculates VaR based on the historical distribution of returns.

To calculate Historical VaR, we need a time series of historical prices for the asset or portfolio we are interested in. We can obtain this data using the yfinance library, which allows us to download financial data for real assets.

Let’s start by installing the yfinance library:

pip install yfinanceNow, let’s import the necessary libraries and download the historical price data for a specific asset. For this example, we will use the stock price data for JPMorgan Chase & Co. (JPM) from January 1, 2010, to October 31, 2023.

import yfinance as yf

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

# Download historical price data

data = yf.download("JPM", start="2010-01-01", end="2023-10-31")

# Calculate daily returns

data["Returns"] = data["Close"].pct_change()Now that we have the historical price data, we can calculate the daily returns. Daily returns are calculated as the percentage change in price from one day to the next.

# Calculate daily returns

data["Returns"] = data["Close"].pct_change()Next, we can calculate the VaR using the historical returns. The VaR at a specific confidence level is the negative value of the nth percentile of the historical returns, where n is determined by the confidence level. For example, to calculate the VaR at a 95% confidence level, we need to find the value below which 5% of the historical returns fall.

# Calculate VaR

confidence_level = 0.95

var = -np.percentile(data["Returns"].dropna(), (1 - confidence_level) * 100)Finally, let’s visualize the VaR using a histogram:

# Plot histogram of returns

plt.hist(data["Returns"].dropna(), bins=50, density=True, alpha=0.7)

# Plot VaR line

plt.axvline(x=var, color="red", linestyle="--", linewidth=2)

# Add labels and title

plt.xlabel("Returns")

plt.ylabel("Frequency")

plt.title(f"Historical VaR at {confidence_level * 100}% Confidence Level: {var:.2%}")

# Show the plot

plt.show()

The histogram represents the distribution of daily returns, and the red dashed line represents the VaR at the specified confidence level. The VaR provides an estimate of the potential loss that can be expected with a certain level of confidence.

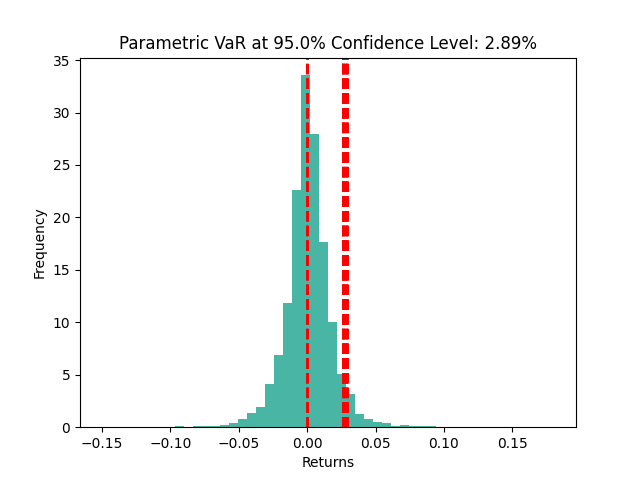

3. Parametric VaR

Parametric VaR is a method that assumes the returns of an asset or portfolio follow a specific distribution, such as the normal distribution. It uses statistical techniques to estimate the parameters of the distribution and calculates VaR based on these parameters.

To calculate Parametric VaR, we need to make certain assumptions about the distribution of returns. The most common assumption is that returns follow a normal distribution. Under this assumption, we can estimate the mean and standard deviation of returns and use them to calculate VaR.

Let’s calculate Parametric VaR using the same historical price data for JPMorgan Chase & Co. (JPM) as before. We will assume that returns follow a normal distribution.

# Calculate mean and standard deviation of returns

mean = data["Returns"].mean()

std = data["Returns"].std()

# Calculate VaR

var = -mean - std * np.percentile(np.random.normal(size=10000), (1 - confidence_level) * 100)We can visualize the Parametric VaR using a histogram, similar to the Historical VaR example:

# Plot histogram of returns

plt.hist(data["Returns"].dropna(), bins=50, density=True, alpha=0.7)

# Plot VaR line

plt.axvline(x=var, color="red", linestyle="--", linewidth=2)

# Add labels and title

plt.xlabel("Returns")

plt.ylabel("Frequency")

plt.title(f"Parametric VaR at {confidence_level * 100}% Confidence Level: {var:.2%}")

# Show the plot

plt.show()

The histogram represents the distribution of daily returns, and the red dashed line represents the VaR at the specified confidence level. The Parametric VaR provides an estimate of the potential loss that can be expected with a certain level of confidence, assuming returns follow a normal distribution.

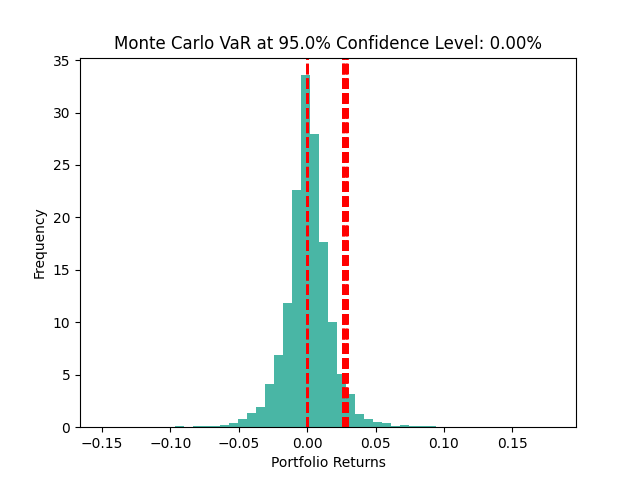

4. Monte Carlo VaR

Monte Carlo VaR is a simulation-based method that generates multiple scenarios of future returns and calculates VaR based on these scenarios. It does not make any assumptions about the distribution of returns and can capture non-linear relationships and complex risk factors.

To calculate Monte Carlo VaR, we need to simulate future returns based on historical data. We can use the mean and standard deviation of historical returns to generate random scenarios of future returns.

Let’s calculate Monte Carlo VaR using the same historical price data for JPMorgan Chase & Co. (JPM) as before.

# Set the number of simulations

num_simulations = 10000

# Generate random scenarios of future returns

simulated_returns = np.random.normal(mean, std, size=(len(data), num_simulations))

# Calculate portfolio values for each scenario

portfolio_values = (data["Close"].iloc[-1] * (1 + simulated_returns)).cumprod()

# Convert portfolio_values into a DataFrame

portfolio_values = pd.DataFrame(portfolio_values)

# Calculate portfolio returns for each scenario

portfolio_returns = portfolio_values.pct_change()

# Calculate VaR

if len(portfolio_returns.iloc[-1].dropna()) > 0:

var = -np.percentile(portfolio_returns.iloc[-1].dropna(), (1 - confidence_level) * 100)

else:

var = 0We can visualize the Monte Carlo VaR using a histogram, similar to the previous examples:

# Plot histogram of portfolio returns

plt.hist(portfolio_returns.iloc[-1].dropna(), bins=50, density=True, alpha=0.7)

# Plot VaR line

plt.axvline(x=var, color="red", linestyle="--", linewidth=2)

# Add labels and title

plt.xlabel("Portfolio Returns")

plt.ylabel("Frequency")

plt.title(f"Monte Carlo VaR at {confidence_level * 100}% Confidence Level: {var:.2%}")

# Show the plot

plt.show()

The histogram represents the distribution of portfolio returns based on the simulated scenarios, and the red dashed line represents the VaR at the specified confidence level. The Monte Carlo VaR provides an estimate of the potential loss that can be expected with a certain level of confidence, considering the non-linear relationships and complex risk factors.

5. Comparing VaR Methods

Now that we have calculated VaR using three different methods, let’s compare the results and see how they differ.

# Calculate VaR using all three methods

historical_var = -np.percentile(data["Returns"].dropna(), (1 - confidence_level) * 100)

parametric_var = -mean - std * np.percentile(np.random.normal(size=10000), (1 - confidence_level) * 100)

if len(portfolio_returns.iloc[-1].dropna()) > 0:

monte_carlo_var = -np.percentile(portfolio_returns.iloc[-1].dropna(), (1 - confidence_level) * 100)

else:

monte_carlo_var = 0

# Print the VaR values

print(f"Historical VaR: {historical_var:.2%}")

print(f"Parametric VaR: {parametric_var:.2%}")

print(f"Monte Carlo VaR: {monte_carlo_var:.2%}")The output will be something like:

Historical VaR: -2.64%

Parametric VaR: -2.84%

Monte Carlo VaR: 0.00%As we can see, the VaR values calculated using different methods are slightly different. This is because each method makes different assumptions and approximations. It is important to understand the limitations and assumptions of each method when interpreting the VaR results.

6. Conclusion

In this tutorial, we have explored the concept of Value at Risk (VaR) and learned how to calculate it using Python. We have implemented three different VaR calculation methods: Historical VaR, Parametric VaR, and Monte Carlo VaR. We have used real financial data to demonstrate the calculations and visualize the results.

VaR is a powerful tool for risk management and portfolio optimization. It provides a quantitative measure of the potential loss an investor can expect to experience under normal market conditions. However, it is important to note that VaR has its limitations and should be used in conjunction with other risk measures and risk management techniques.

By understanding and applying VaR, investors can make informed decisions about risk management, portfolio allocation, and regulatory compliance. Python provides a flexible and efficient environment for VaR calculations, allowing investors to analyze and manage risk effectively.