70%+ Automated Returns-15M Bull Reversal-NQ Futures

This article will present the code to execute a simple 15m candle reversal patten on Nasdaq futures using Python. The pattern essentially detects selling exhaustion in the market, leaving a higher probability of price moving in the other direction. The criteria for the reversal pattern is as follows: a bearish candle must precede a bullish candle with a lower low, a lower high and a close within the body of the bear candle. Then, the code runs a simulation that enters a trade one tick above the high of the signal candle with a 35-tick profit/loss; i.e. a 1:1 Risk Reward Ratio with no time limit. This means whenever the signal is generated, the trade order will remain open until price reaches this level.

// Pine Script for implementing in TradingView

//@version=4

study("Candlestick Patterns", shorttitle="CP", overlay=true)

// Identify Bear Candle

bearCandle = close[1] < open[1]

// Check for Bull Candle with specific criteria

bullCandleCriteria = close > open and close > close[1] and close < open[1] and low < low[1] and high < high[1]

// Combine conditions to detect the specified pattern for bear followed by bull

bearBullPattern = bearCandle and bullCandleCriteria

// Plot yellow triangle on the second candle of the bear followed by bull pattern as a signal indicator

plotshape(bearBullPattern, style=shape.triangleup, location=location.belowbar, color=color.red, size=size.small)I have also generated plots to show which time of day this strategy works best and worst, as well as the daily win/loss percentage. Lastly, I wanted to test if there was a significant success rate for this setup with respect to an 8-period Exponential Moving Average.

I coded all of this into Google Colab using Python and collected data from TradingView. The dataset is over 20000 periods long, spanning 10 months 2023–05–01 00:00:00 to 2024–03–13 20:15:00.

!pip install yfinance pandas matplotlib mplfinance

# Mounting T Data Sets from Google Drive

from google.colab import drive

drive.mount('/content/drive')

# Path to your file, e.g., "My Drive" is the root directory of your Google Drive

file_path = '/content/drive/My Drive/Historical_T_Data/NQ_15M_ETH.csv'

import pandas as pd

df = pd.read_csv(file_path, header = None)

# Define the conditions for the original signal pattern

def detect_signal_pattern(df):

# Identify Bear Candle

df['bearCandle'] = df[4] < df[1]

# Check for Bull Candle with specific criteria

bull_candle_condition = (

(df[3] < df[3].shift(1)) &

(df[2] < df[2].shift(1)) &

(df[4] < df[1].shift(1)) &

(df[4] > df[4].shift(1))

)

df['bullCandle'] = bull_candle_condition

# Combine conditions to detect the original signal pattern

df['signalPattern'] = df['bearCandle'].shift(1) & df['bullCandle']

return df

# Define the conditions for the opposite signal pattern

def detect_opposite_signal_pattern(df):

# Identify Bull Candle

df['bullCandleOpposite'] = df[4] > df[1]

# Check for Bear Candle with specific criteria

bear_candle_condition = (

(df[3] > df[3].shift(1)) &

(df[2] > df[2].shift(1)) &

(df[4] > df[1].shift(1)) &

(df[4] < df[4].shift(1))

)

df['bearCandleOpposite'] = bear_candle_condition

# Combine conditions to detect the opposite signal pattern

df['oppositeSignalPattern'] = df['bullCandleOpposite'].shift(1) & df['bearCandleOpposite']

return df

# Load your dataset into a DataFrame (replace this with your actual dataset)

# Assuming your dataset is already loaded into df

# Apply the indicator functions to your dataset

df = detect_signal_pattern(df)

df = detect_opposite_signal_pattern(df)

# Print the modified DataFrame with signal pattern columns

print(df)

import pandas as pd

# Function to apply the strategy and calculate performance metrics

def apply_strategy(df):

# Initialize variables for performance metrics

total_trades = 0

total_winning_trades = 0

total_losing_trades = 0

# Iterate over rows in the DataFrame

for index, row in df.iterrows():

# Check if there is a bull signal

if row['bullCandle']:

# Convert values to numeric

high = pd.to_numeric(row[2])

# Take long position one tick above the high of the bull signal candle

entry_price = high + 0.01

# Increment total trades count

total_trades += 1

# Initialize variables to track price movement

max_high = entry_price

min_low = entry_price

# Iterate over subsequent rows to track price movement

for next_index, next_row in df.iloc[index+1:].iterrows():

# Convert values to numeric

next_high = pd.to_numeric(next_row[2])

next_low = pd.to_numeric(next_row[3])

# Update max_high and min_low

max_high = max(max_high, next_high)

min_low = min(min_low, next_low)

# Check if price rises by 35 ticks first

if max_high - entry_price >= 35 * 0.01:

total_winning_trades += 1

break

# Check if price drops by 35 ticks first

elif entry_price - min_low >= 35 * 0.01:

total_losing_trades += 1

break

# Calculate win rate percentage

win_rate_percentage = (total_winning_trades / total_trades) * 100 if total_trades != 0 else 0

# Print performance metrics

print("Total Trades Taken:", total_trades)

print("Number of Winners:", total_winning_trades)

print("Number of Losers:", total_losing_trades)

print("Win Rate Percentage:", win_rate_percentage)

# Load your dataset into a DataFrame (replace this with your actual dataset)

# Assuming your dataset is already loaded into df

# Apply the strategy and calculate performance metrics

apply_strategy(df)Total Trades Taken: 1080 Number of Winners: 758 Number of Losers: 322 Win Rate Percentage: 70.185%

import pandas as pd

# Function to apply the strategy and return winning and losing trades

def get_trades(df):

winning_trades = []

losing_trades = []

# Iterate over rows in the DataFrame

for index, row in df.iterrows():

# Check if there is a bull signal

if row['bullCandle']:

# Convert values to numeric

high = pd.to_numeric(row[2])

# Take long position one tick above the high of the bull signal candle

entry_price = high + 0.01

# Initialize variables to track price movement

max_high = entry_price

min_low = entry_price

# Iterate over subsequent rows to track price movement

for next_index, next_row in df.iloc[index+1:].iterrows():

# Convert values to numeric

next_high = pd.to_numeric(next_row[2])

next_low = pd.to_numeric(next_row[3])

# Update max_high and min_low

max_high = max(max_high, next_high)

min_low = min(min_low, next_low)

# Check if price rises by 35 ticks first

if max_high - entry_price >= 35 * 0.01:

winning_trade_data = {'EntryPrice': entry_price, 'ExitPrice': max_high}

winning_trade_data.update(row) # Add original row data

winning_trades.append(winning_trade_data)

break

# Check if price drops by 35 ticks first

elif entry_price - min_low >= 35 * 0.01:

losing_trade_data = {'EntryPrice': entry_price, 'ExitPrice': min_low}

losing_trade_data.update(row) # Add original row data

losing_trades.append(losing_trade_data)

break

# Create DataFrames for winning and losing trades

winning_trades_df = pd.DataFrame(winning_trades)

losing_trades_df = pd.DataFrame(losing_trades)

return winning_trades_df, losing_trades_df

# Load your dataset into a DataFrame (replace this with your actual dataset)

# Assuming your dataset is already loaded into df

# Get winning and losing trades

winning_trades_df, losing_trades_df = get_trades(df)

# Print winning trades DataFrame

print("Winning Trades:")

print(winning_trades_df)

# Print losing trades DataFrame

print("\nLosing Trades:")

print(losing_trades_df)

import pandas as pd

# Function to tally winning trades in each hour

def tally_winning_trades_by_hour(winning_trades_df):

# Convert the 'date' column to datetime with timezone awareness

winning_trades_df['date'] = pd.to_datetime(winning_trades_df[0], utc=True)

# Convert to local timezone (adjust as per your data)

winning_trades_df['date'] = winning_trades_df['date'].dt.tz_convert('Europe/London')

# Extract hour from the timestamp

winning_trades_df['hour'] = winning_trades_df['date'].dt.hour

# Group the trades by hour and count the number of winning trades in each hour

hourly_counts = winning_trades_df.groupby('hour').size()

return hourly_counts

# Assuming winning trades DataFrame is already loaded and named winning_trades_df

# Tally winning trades in each hour

hourly_counts = tally_winning_trades_by_hour(winning_trades_df)

# Print the hourly counts

print("Winning Trades Tally by Hour:")

print(hourly_counts)

#########

import pandas as pd

import matplotlib.pyplot as plt

# Function to tally winning trades in each hour

def tally_winning_trades_by_hour(winning_trades_df):

# Convert the 'date' column to datetime with timezone awareness

winning_trades_df['date'] = pd.to_datetime(winning_trades_df['date'], utc=True)

# Convert to local timezone (adjust as per your data)

winning_trades_df['date'] = winning_trades_df['date'].dt.tz_convert('Europe/London')

# Extract hour from the timestamp

winning_trades_df['hour'] = winning_trades_df['date'].dt.hour

# Group the trades by hour and count the number of winning trades in each hour

hourly_counts = winning_trades_df.groupby('hour').size()

return hourly_counts

# Assuming winning trades DataFrame is already loaded and named winning_trades_df

# Tally winning trades in each hour

hourly_counts = tally_winning_trades_by_hour(winning_trades_df)

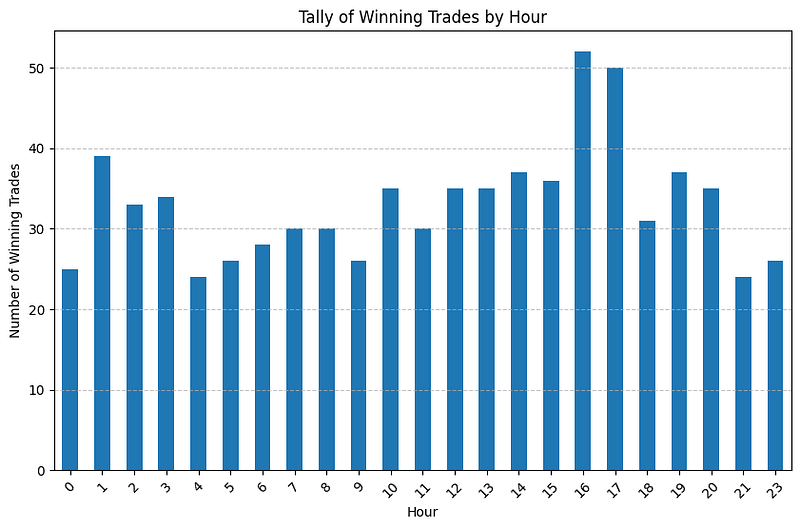

# Plot a bar chart

hourly_counts.plot(kind='bar', figsize=(10, 6))

plt.title('Tally of Winning Trades by Hour')

plt.xlabel('Hour')

plt.ylabel('Number of Winning Trades')

plt.xticks(rotation=45)

plt.grid(axis='y', linestyle='--', alpha=0.7)

plt.show()

import pandas as pd

# Function to tally losing trades in each hour

def tally_losing_trades_by_hour(losing_trades_df):

# Convert the 'date' column to datetime with timezone awareness

losing_trades_df['date'] = pd.to_datetime(losing_trades_df[0], utc=True)

# Convert to local timezone (adjust as per your data)

losing_trades_df['date'] = losing_trades_df['date'].dt.tz_convert('Europe/London')

# Extract hour from the timestamp

losing_trades_df['hour'] = losing_trades_df['date'].dt.hour

# Group the trades by hour and count the number of losing trades in each hour

hourly_counts = losing_trades_df.groupby('hour').size()

return hourly_counts

# Assuming losing trades DataFrame is already loaded and named losing_trades_df

# Tally losing trades in each hour

hourly_counts_losing = tally_losing_trades_by_hour(losing_trades_df)

# Print the hourly counts

print("Losing Trades Tally by Hour:")

print(hourly_counts_losing)

import matplotlib.pyplot as plt

# Plot a bar chart for losing trades by hour

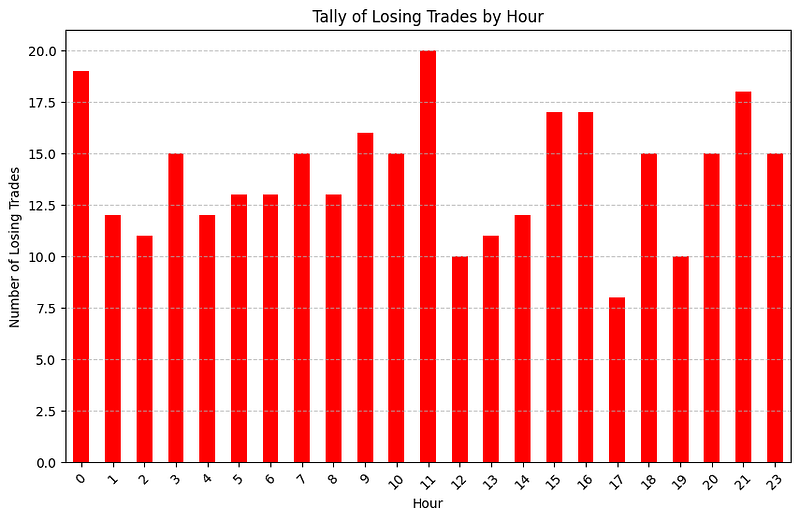

hourly_counts_losing.plot(kind='bar', figsize=(10, 6), color='red')

plt.title('Tally of Losing Trades by Hour')

plt.xlabel('Hour')

plt.ylabel('Number of Losing Trades')

plt.xticks(rotation=45)

plt.grid(axis='y', linestyle='--', alpha=0.7)

plt.show()

import pandas as pd

# Function to tally winning trades by day of the week

def tally_winning_trades_by_day(winning_trades_df):

# Convert the 'date' column to datetime with timezone awareness

winning_trades_df['date'] = pd.to_datetime(winning_trades_df['date'], utc=True)

# Convert to local timezone (adjust as per your data)

winning_trades_df['date'] = winning_trades_df['date'].dt.tz_convert('Europe/London')

# Extract day of the week from the timestamp

winning_trades_df['day_of_week'] = winning_trades_df['date'].dt.day_name()

# Group the trades by day of the week and count the number of winning trades for each day

daily_counts = winning_trades_df.groupby('day_of_week').size()

return daily_counts

# Function to tally losing trades by day of the week

def tally_losing_trades_by_day(losing_trades_df):

# Convert the 'date' column to datetime with timezone awareness

losing_trades_df['date'] = pd.to_datetime(losing_trades_df['date'], utc=True)

# Convert to local timezone (adjust as per your data)

losing_trades_df['date'] = losing_trades_df['date'].dt.tz_convert('Europe/London')

# Extract day of the week from the timestamp

losing_trades_df['day_of_week'] = losing_trades_df['date'].dt.day_name()

# Group the trades by day of the week and count the number of losing trades for each day

daily_counts = losing_trades_df.groupby('day_of_week').size()

return daily_counts

# Assuming winning trades and losing trades DataFrames are already loaded and named winning_trades_df and losing_trades_df respectively

# Tally winning trades by day of the week

daily_counts_winning = tally_winning_trades_by_day(winning_trades_df)

# Tally losing trades by day of the week

daily_counts_losing = tally_losing_trades_by_day(losing_trades_df)

# Print the daily counts for winning trades

print("Winning Trades Tally by Day of the Week:")

print(daily_counts_winning)

print()

# Print the daily counts for losing trades

print("Losing Trades Tally by Day of the Week:")

print(daily_counts_losing)

import matplotlib.pyplot as plt

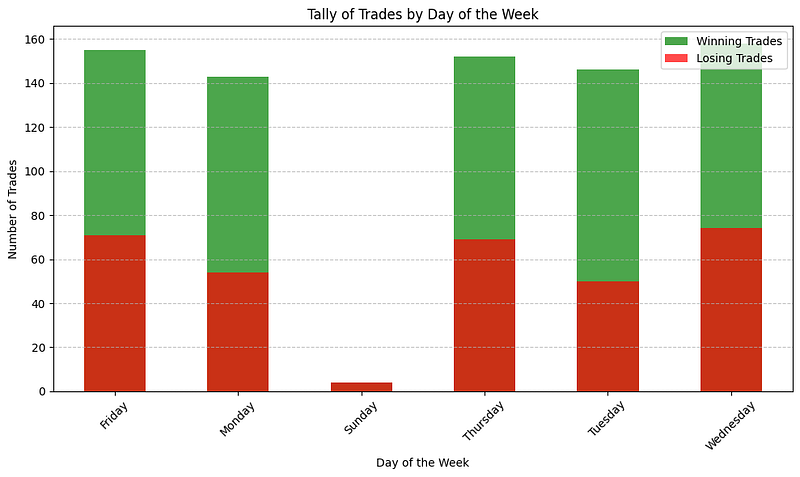

# Plot a bar chart for winning trades by day of the week

plt.figure(figsize=(10, 6))

daily_counts_winning.plot(kind='bar', color='green', alpha=0.7, label='Winning Trades')

# Plot a bar chart for losing trades by day of the week

daily_counts_losing.plot(kind='bar', color='red', alpha=0.7, label='Losing Trades')

# Customize the plot

plt.title('Tally of Trades by Day of the Week')

plt.xlabel('Day of the Week')

plt.ylabel('Number of Trades')

plt.legend()

plt.xticks(rotation=45)

plt.grid(axis='y', linestyle='--', alpha=0.7)

plt.tight_layout()

# Show the plot

plt.show()

# Convert the 'EMA' column to numerical values

df['EMA'] = pd.to_numeric(df[6], errors='coerce')

# Check if the buy price is above or below the EMA for each trade

df['buy_price_above_EMA'] = df['entry_price'] > df['EMA']

# Now calculate the percentage of winners where the price is above and below the EMA

winners_above_EMA = df[df['signalPattern'] & df['buy_price_above_EMA']]

winners_below_EMA = df[df['signalPattern'] & ~df['buy_price_above_EMA']]

percentage_winners_above_EMA = (len(winners_above_EMA) / len(df[df['signalPattern']])) * 100

percentage_winners_below_EMA = (len(winners_below_EMA) / len(df[df['signalPattern']])) * 100

# Print the percentages

print("Percentage of winners where the price is above EMA:", percentage_winners_above_EMA)

print("Percentage of winners where the price is below EMA:", percentage_winners_below_EMA)Percentage of winners where the price is above EMA: 51.67 Percentage of winners where the price is below EMA: 48.33