The True Inflation Number is Frightening

It’s more than the 2% we’re led to believe

Understanding inflation is crucial to bettering your finances. It impacts your earnings, spending, and investment returns, which all result in a change to your purchasing power.

It’s worth looking into true inflation and its impact, and not just the CPI number. Investigating the effects of true inflation can change the way you think about money.

What is CPI?

CPI stands for Consumer Price Index. CPI is often used interchangeably with inflation because CPI measures the change in prices over time that consumers pay for goods and services.

The bureau of labor statistics defines CPI as,

The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services

The issue with using CPI to gauge inflation is that it is a basket of goods and services. It is what is included and not included in this basket that causes issues for me.

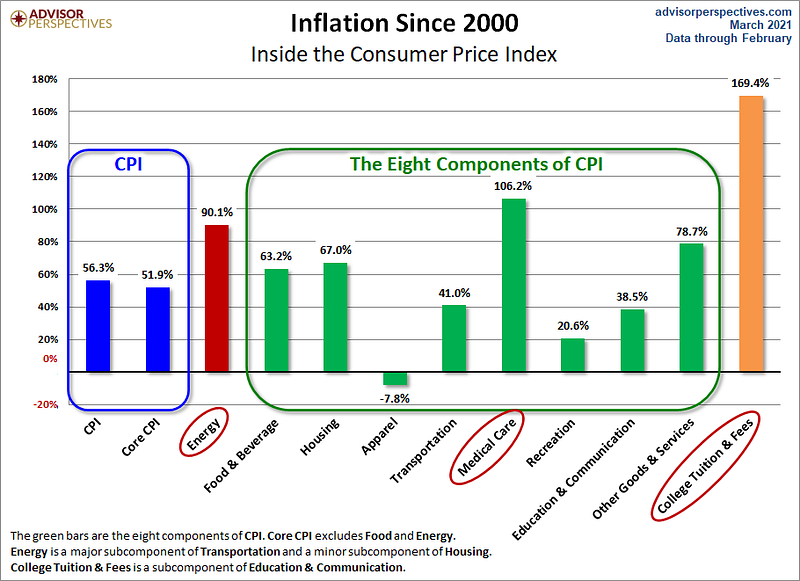

CPI puts expenditures into 8 majors groups: food and beverages, housing, apparel, transportation, medical care, recreation, education and communication, and other goods and services.

It does not include investment items, such as stocks, bonds, real estate, and life insurance.

Below is a graphic that shows how inflated each component is since 2000.

How inflation impacted investment items

We’re paying 56.3% more overall for items since 2000. That isn’t as terrible as it sounds, especially considering that was 21 years ago.

But none of these components have increased as much as investment items such as real estate and stocks, which are not included in inflation (CPI) calculations.

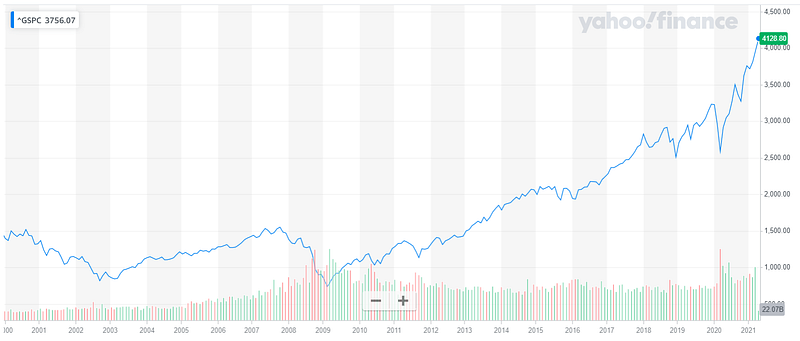

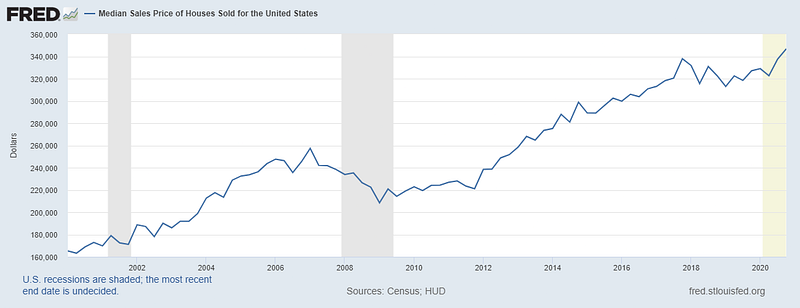

Below are the charts for the S&P 500 since Jan 1, 2000 and the Median Sales Price of Houses Sold for the United States since Q1 2000.

Since 2000, the S&P 500 is up 181% (from $1,469.25 to $4,128.80) and the average home price is up 110% (from $165,300 to $346,800.)

So if these two categories were included in CPI’s calculation, inflation would be much higher each year.

I want to reiterate this: We should consider inflation to be higher than the CPI number. Once I started thinking of inflation in this light, it changed how I viewed my wage or investment increases.

I don’t know what the “true” CPI number would be if you include investment items. But if your employer increases your salary 2–3% annually, are you really staying ahead of inflation or are you losing purchasing power?

And how happy will you be with your investment returns? If your goal is to just beat inflation, how can you now know the true inflation number? If your goal is to have a 6% return after accounting for inflation (ex. earning 8% but 2% inflation brings your real return to 6%) how can you calculate that with this new inflation number?

Lastly, one of the big issues in society today; the growing wealth of the top 10%.

It's no secret the rich own a large portion of stocks and real estate. And these investments have grown considerably in recent years, increasing the wealth of the rich. I personally have no problem with the rich getting richer; if real estate and stocks are the simple strategies to get rich, we all follow suit.

However, the more investments someone holds, the more their wealth increases. If that’s the case, your purchasing power should not be measured just against CPI but against CPI and the increase in investment assets.

The Federal Reserve

Jerome Powell and the federal reserve are arguably the most important people in the world. They control the United States monetary system. And since the US went off the gold standard in 1971, they have had more of an impact than ever.

The Fed, directly or indirectly, inflates the prices of investment assets. As a result, “the rich get richer.”

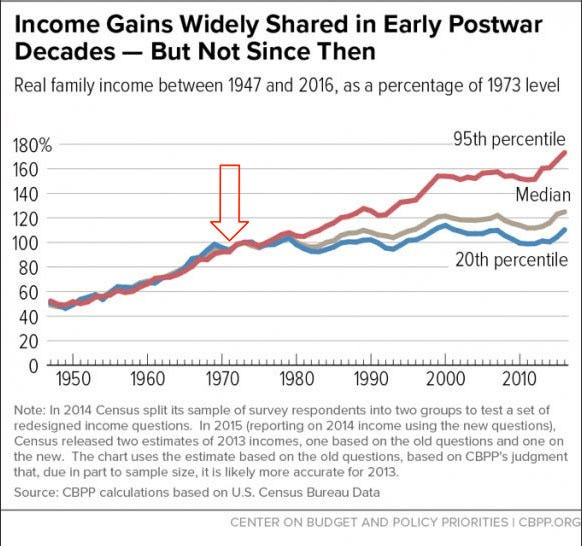

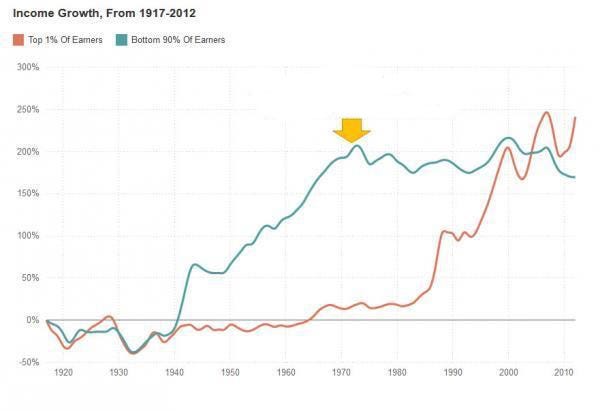

A while back I stumbled across a website, https://wtfhappenedin1971.com/

It provides a variety of graphs displaying the impact going off the gold standard has had on the economy. Two of the best graphs show the impact it has had on income by percentile.

Other considerations and final thought

Tim Denning is one of my favorite writers on Medium; I recommend checking out some of his investing and economic-related work if you aren’t familiar with him. But he had a great article a few months back showing that the average inflation over the last 5 years is between 8.1% and 12.9% and the worst part, inflation was 20% in 2020.

This new administration isn’t too worried about inflation as taught in the old-fashion economic theory. Biden’s theory is that pumping out stimulus programs will have greater benefits than the negatives associated with increased inflation and decreased purchasing power.

We’ve seen how markets have responded to the past three stimulus programs, as the S&P keeps reaching record highs and rewards those invested.

‘Correlation does not imply causation’ but it seems the more money the government prints, the better the stock market does. The new infrastructure bill, as well as other stimulus bills released in coming months and years, may help propel us into the new roaring twenties.

As they say, if you can’t beat ’em, join 'em. So I’m pumping money into the market in hopes that this record run will continue for many years.

Update: After Jerome Powell’s recent interview on 60 minutes I stand by my belief that the market will offer solid returns as Powell repeatedly assured that the Federal Reserve will “do everything we can to support the economy for as long as it takes.”

And for further reading on how the Federal Reserve enriches the wealthy, “Why the Federal Reserve Sucks.”

The above references an opinion and is for information purposes only. It is not investment advice.