4 Strategies To Help You Get Over Bad Money Habits

Bad money habits undermine your hard work and will keep you poor

Like with anything, small habits result in significant outcomes. For example, people who do not have good daily habits around brushing and flossing their teeth are more likely to have poor dental hygiene. Poor dental hygiene results in expensive visits to the dentist, lowered social status, and can ultimately lead to heart disease. The small daily habit of teeth brushing directly impacts the quality of one’s life in both the short and long term. Similarly, our money habits directly impact our ability to live long, abundant, and free lives.

Bad Habit #1: Not Having a Budget

Most people don’t have a written, functional, or well-maintained budget. I have worked with people who run the gamut when it comes to budgeting practices, and here are a few of the reasons that I’ve heard from people with poor budgeting practices:

- “I keep a mental budget” or “I have an idea of where my money is going”

- “I don’t have time to budget.”

- “I wrote down a budget, but I haven’t updated it.”

- “It’s hard for me to stay within my budget.”

- “I’m not very good with spreadsheets.”

Each of the above statements represents the wrong way to think about a budget. Instead of thinking about budgets as some stagnant, inflexible, cumbersome, time-consuming chore, it is better to think of budgets as a necessary tool that, once established, can save you time and money and lead to freed mental capacity and less stress. Budgets should be written down, easy to maintain, adaptable, and thorough enough to account for your spending habits. Once a good budget is created, it becomes easy to maintain and will provide an accurate snapshot of your overall financial health at a glance.

Strategy: Adopt and Maintain a Monthly Budget

You can adopt this monthly budget or Google one that suits your needs and stylistic preferences. While you can use an old-fashioned pen and paper to budget your money, it’s easier and more efficient to use a digital spreadsheet or a budgeting app. Digital budgets will contain designated fields and built-in formulas to identify overages and shortfalls with minimal effort.

Bad Habit #2: Having Vague Long Term Goals

Most people don’t have clear, well-defined long-term financial goals. I have worked with people at various stages of life who don’t have a good idea of how much their hopes and dreams cost and therefore don’t have an idea of how to plan accordingly. Here are a few mindsets I’ve encountered from my money mindset coaching clients:

- I want to go to college, but I don’t know how much it costs.

- We plan to have children but have never thought about developing a saving plan to help us comfortably afford children.

- I don’t know when I’ll retire, nor do I know how much I need to save to retire comfortably.

Going to college, starting a family, and retiring are common long-term goals but are rarely financially planned. People often begin thinking about college, children, and retirement 2–5 years before the event, which is not enough time to prepare adequately. Long-term plans are for events more than 5 years away. Early planning around a clear goal helps to make the goal more accomplishable.

Strategy: Develop SMART money goals and a backward plan

SMART is an acronym standing for Specific, Measurable, Achievable, Realistic, and Time-bound. For example, early-career professionals at the age of 25 making $50K per year can set SMART goals around retiring. Their goal might sound like this, “I plan to retire at age 65, with a paid-off home, and $4.5K monthly income to live off of. $3K of my retirement income will come from 401K disbursements and $1.5K will come from social security.” To plan backward, this person should use online retirement and social security calculators to help determine specific saving goals, investment growth rates, and years required to achieve their goal.

Bad Habit #3: Focused on the Wrong Education

We are all taught to go to school, get a good job, work hard for 30–40 years, and then retire. This is excellent advice for an economic system that relies on masses of cheap and unorganized labor to work for the benefit of the wealthy minority. For the ruling few to maintain power in an oligarchic stratified capitalist state, inexpensive labor is critical; that’s why public schools, which are both free and essentially mandatory in the US, don’t teach financial literacy but instead socialize children to believe that they must work hard for other people for the majority of their lives. Most Americans follow this narrative and spend 40 years laboring at jobs that pay them less than their value, and if they’re lucky, they’ll enjoy a few years of retirement with decent health.

Because of their public-school training and the dominant social zeitgeist, many working and middle-class kids grow up dreaming of becoming doctors, lawyers, engineers, professors, therapists, accountants, or something of the like. If they secure a professional job with a middle or high salary, they consider themselves successful. With this logic at play, they focus all their educational energy on developing a professional skillset and spend insufficient time learning about financial literacy. Unfortunately, the risk of investing all of one’s education into securing a professional job is the possibility of becoming a high earner that is also deeply in debt. High incomes without sufficient financial literacy often lead to inflated lifestyles that entrap many professionals into survival mode instead of allowing them to have a life of true abundance. In this article, I write about the perils of earning a high income while having low financial literacy.

Strategy: Supplement Academics with Financial Literacy

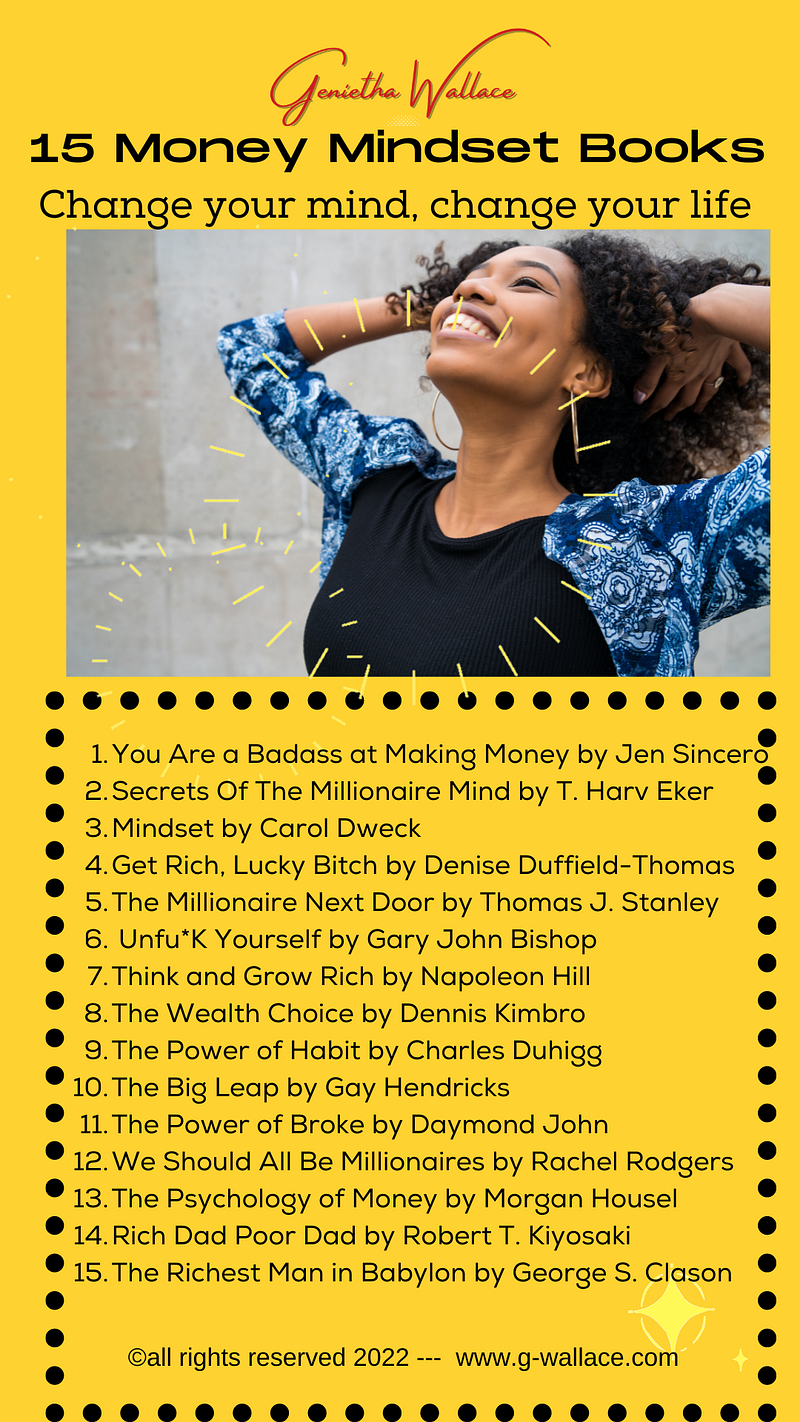

Invest in your financial literacy at the same rate as your professional skills. Add personal finance books to your reading list, take courses in money management, participate in business workshops, and get mentors who can help illuminate the path to financial success. Diversify your educational focus, and make room in the curriculum of your life to learn about the 7 levels of wealth. Avoid falling into the trap of becoming a high-paid professional with little understanding of how the economic system is designed to keep the majority working for less than the value they produce in the world..

Bad Habit #4: Thinking Negatively About Money

Some people self-sabotage by investing their energy into negative money thoughts instead of investing into abundance thinking. Here are a few negative money mindsets I’ve encountered in my money mindset coaching:

- Money doesn’t grow on trees

- Money is the root of all evil

- Prioritizing money will prevent me from________(fill in the blank, i.e., spending time with family, doing the things I love, etc.)

These negative thoughts are based on scarcity thinking, inaccurate projections of evil, and lack of financial knowledge. None of these beliefs are wholly authentic and, unfortunately, they reinforce a self-fulfilling and self-defeating pattern of under-performance and discontent.

Strategy: Change Your Mindset and Get Support

Changing your money mindset is very difficult because of the intrinsic nature of limiting beliefs. Therefore, it’s not advisable to go at it alone. I encourage people to follow social media accounts that reinforce abundance thinking, surround themselves with friends and family who have positive money thoughts, and read books on how to change a mindset. Changing one’s mindset requires practice and constant effort, however with effort, you will notice your money mindset begin to shift, and so too will the amount of abundance in your life.

Final Thoughts:

Bad money habits, like any other bad habit, compound when they aren’t dealt with. The longer we wait to identify our bad money habits, the greater the negative impact they have on our lives. A little time and energy invested to change our habits will pay multiple types of dividends for decades to come.

If you enjoy reading content like this, consider subscribing to my feed. Also, if you are not a Medium member and you would like to gain unlimited access to the platform, consider using my referral link right here to sign up. It’s $5 a month and you get unlimited access to my articles and many others like mine. Thanks.

Note: I’m not a financial advisor, I write for educational/entertainment purposes only. Nothing in this or any of my other articles constitutes financial or legal advice.

A version of this article was previously published on www.G-Wallace.com