4 Lessons on When to Sell $400,000 Worth of Stock in an Unpredictable Market

Tools and pearls of wisdom for framing and managing risk; knowing when to sell stock and when to hold; and keeping emotions at bay.

Related

• Is the Stock Market Really in a Bear Market? Maybe. Maybe Not. • When Is a Stock Market Crash Not Really a Stock Market Crash? • MBA Guide to Dealing with Higher Mortgage Interest Rates, Part 2 — How Much Money Will You Save?

Recent

• The Deafening Silence on Stock Buybacks from Centrist Democrats • 2 Reasons Populations Are Collapsing in Developed Countries • 3 Key Facts Everyone Is Missing About Biden’s Student Loan Debt Relief

Potential to Change the Way You Think

• Why Are Fundamental Human Values Critically Important for Successful, Enduring Brands? • Life Expectancy vs. Healthcare Costs in the U.S. (and Japan, Germany, France, Spain, Portugal, etc.) • (1a/9) “Top-Down” Makes More Sense Than “Left-Right” in the U.S.

My friend, Matt emailed me on a Friday afternoon. He had just “come into” 4,500 shares of stock in a hot software company, Siebel Systems — a $450,000 windfall!

A startup company he used to work for had been acquired by Siebel. It was entirely unexpected, but Matt’s stock from the startup would be converted into Siebel stock and was going to be worth something.

Matt wanted to ask for my advice about buying stock options as insurance in case Siebel’s stock price went down. The Siebel stock would be deposited into his brokerage account three days later on Monday morning.

We made plans to meet for lunch on that Monday.

But it was clear to me that he had asked the wrong question.

Quick background

Matt (not his real name) had just finished graduate school a few years earlier. He still had $40,000 in student loan debt, and he had no real assets other than his bi-weekly paycheck.

By that time we were planning lunch, the “dot-com bubble” in tech stocks was 9 months into popping and deflating. Since its all-time intraday high in mid-March 2000, the NASDAQ had dropped by 43%. High-flying tech stocks were regularly seeing their valuations slashed during those 9 months.

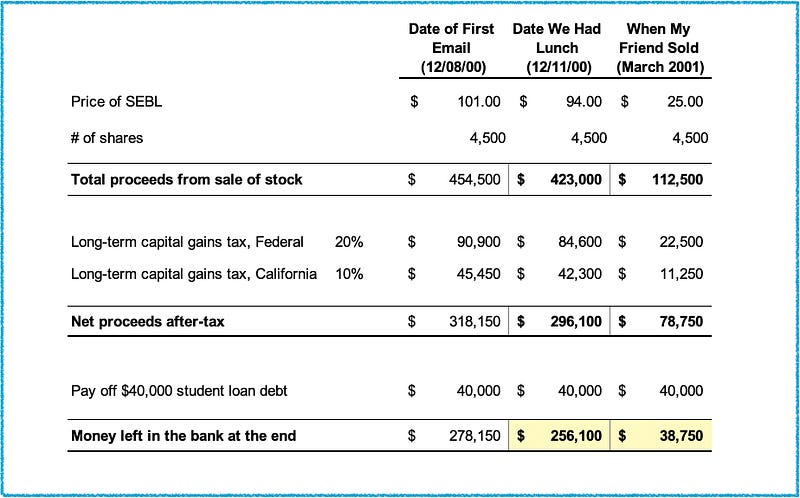

The day we had lunch — Monday — Siebel stock closed around $94, down $7 from Friday’s close of $101.

That meant that as of Friday’s close of market, Matt’s 4,500 shares of SEBL were worth $454,000. And by the time we were in the middle of lunch (on the west coast) and the market had closed, his 4,500 shares were worth about $424,000.

Given the drop, Matt was even more interested in buying put options for “insurance” in case the stock went down.

My initial analysis

By the second half of 2000, all it took for a stock to fall overnight by 30% or more was missing earnings estimates by as little as a penny.

Quarterly earnings for SEBL stock were due to be released several days after our lunch. It had been a tough 9 months for tech stocks, and there seemed to be real potential for Siebel stock to go down.

Prior to our lunch, I took a look at the pricing for Siebel put options. There were two immediate problems.

- Only short-term options were available — no more than 6–9 months into the future. The protection wouldn’t be for very long, and then Matt would need to buy puts all over again.

- The second problem was that the pricing of the options was quite expensive even on the March options.

The recommendation I planned to give to Matt at lunch on Monday

Sometimes in life, it’s hard to see through the fog in a given the situation and know what the right answer is.

This was not one of those times. This time it was easy to see the right answer:

(1) Sell it all and (2) do so as soon as the stock was in his brokerage account and he was able to sell.

- Don’t worry about the price.

- Don’t try to micro-time it or wait a few days or weeks to see what would happen.

- Sell. it. all. now.

Knowing when to sell and when to hold

People tend to have good instincts about when to buy.

But they struggle with decisions about whether and when to sell.

Part of the reason is that once you own stock or another asset, it’s easy for your emotions to get tangled up in decisions about selling or holding.

The emotion of wanting your stock to go up and to not look like a fool if you sell at a loss makes it difficult to approach this decision with a clear head.

A mental trick to remove emotion from a “sell or hold” decision

The most useful mental tool I’ve figured out to help make the “sell or hold” decision is to imagine that you are 100% in cash and considering buying the position that you already hold now.

Essentially, transform the decision from (1) a “sell or not” decision that you are going to struggle with into (2) a “buy or not” decision that you can probably be more clear-headed about.

So if Matt didn’t already have those 4,500 shares that would cost $423,000 to buy on the day that we had lunch and if he had the cash sitting in his bank account, would he feel compelled to make that purchase? Would he really, really feel compelled to buy?

1. If the answer is “yes, he would feel compelled to buy that stock today,” then it probably makes sense to go ahead and continue to just hold the position. In other words, don’t sell.

2. But if the answer is, “Hell, no! If I had cash in the bank right now, there is no way I would go and buy that stock today at this price!” then that is at least a yellow flag to consider selling. And it might actually be a loud siren to go and get out of the stock as quickly as possible.

Now let’s apply this mental tool to Matt’s situation

When I thought about this from Matt’s perspective, it was clear to me in an instant that if he had $40,000 in student loan debt and $470,000 in the bank, there was no chance — ZERO chance — that he would take all of that money and:

- not only put it all in the stock market which had been doing lousy for the past nine months,

- not only put all of it into a single sector of the stock market,

- but go and put all of that money into a single stock.

Nobody in their right mind would do that.

The only way you might do it is if you had a strong conviction that you were seeing something about that company that the rest of the market wasn’t seeing or was undervaluing.

And Matt had no such strong conviction.

So what happened at lunch on Monday?

We sat down to lunch at the Fog City Diner in San Francisco. Matt reviewed the situation to make sure we were both on the same page.

Then I walked through (1) why I thought it didn’t make sense to buy options and (2) why it made sense to sell all of his stock at the market open the next morning.

You can imagine my shock when his answer back to me was, “but if I sell, I’ll lose $31,000 from where the stock was on Friday! I can’t sell!”

My appetite for food evaporated. Lunch just became a lot less enjoyable.

Matt was a finance major at one of the top business schools in the U.S. So I assumed that we were going to discuss this from a business/intellectual perspective and in a cold-blooded, ruthless way about whether to sell or hold.

I probably shouldn’t have assumed that because . . . well, I’ll let a classic TV scene explain why:

None of what I am describing here would be surprising to a person with a background in behavioral finance. Anchoring your price is actually a natural thing to do.

But in this case, I was really worried for Matt that this could end up being devastating for him.

Bottom line, by the time we had finished lunch, he was convinced that buying options for price insurance did not make sense, but he was also planning to hold the stock and wait for it to drift higher.

So what happened next with the stock? How did things turn out?

It wasn’t good. No happy ending here.

From the $94 range, the stock drifted lower — not higher — over the next several days down to the $78 range.

One week after the day we had lunch, quarterly earnings came out.

I don’t remember whether it was that the actual earnings disappointed or that the next quarter’s guidance didn’t meet expectations, but the stock dropped another 19% overnight — all the way down to the $63 range.

At this point, Matt really couldn’t bear to sell.

He was emotionally anchored to that $101 price. Or at this point, the anchor might have slipped down to $94. Either way, he definitely couldn’t bring himself to sell at $63.

A month later in mid-January 2001, SEBL bounced back up to an intraday high of $83.66. The 4,500 shares were worth $376,500 shares at that moment.

But my friend was thinking that if the stock made it back up that high, then it was sure to keep going back up into the $90s.

Except that it didn’t.

From that $83.66 high mark, SEBL started a downward zig-zag over the next 2 months that gradually — but inexorably — took it down to the mid-$20s by the middle of March.

On March 15, 2001, the stock closed at $25.75.

When the stock broke through the $30 level a few days before that, Matt finally started to sell some of the shares. And he ended up selling the rest of it over the next few weeks. My best guess is that he ended up selling those 4,500 shares at an average price in the mid-20’s. Let’s call it $25.

For the purposes of this conversation, it doesn’t matter whether it was $25 or $28 or $22. The important part is that anything below $30 is far below the $94 level SEBL was at on the day we had lunch.

Here’s what the numbers looked like

If we assume federal and California long-term capital gains tax rates of 20% and 10% respectively, that’s 30% that would get taken out before paying off the $40,000 in student loan debt. If the average sales price was $25 per share, that would leave him with a total of $38,750.

If Matt had instead sold everything at $94, then after taxes and after paying off the student loan, he would have been left with $256,000 in his bank account.

Lessons Learned

Lesson #1. Take the emotion out of a “Sell or hold?” decision by flipping it and turning it instead into a “Buy or not?” decision.

Lesson #2. Focus on the biggest picture(s) and big picture risks before you focus on anything smaller.

Ask “whether there is a bigger picture” to consider, and keep asking it until you are sure that you are looking at the biggest relevant picture for your situation.

In Matt’s case, there were 2 big pictures:

- He didn’t fully, truly consider the risk of seeing the stock price drop 50–70% from the mid-90s. Based on the stock market over the previous 9 months, that large a loss was a real possibility. Matt’s worry about the risk of leaving 7% on the table prevented him from fully considering the risk of losing 50% or more.

- The amount of money he could have taken off the table the day we had lunch was enough to moderately change his life. Paying off his student loan debt would leave a big nest egg. The stock going up 7% back to the $101 level was NOT going to change his life qualitatively beyond what the $94 sale price would already do. “Changing your life” is a different thing than “doing incrementally better.”

Lesson #3. Hold your emotions at bay. Be ruthless and coldblooded. Don’t second-guess yourself after you execute on your decision.

Lesson #4. It’s hard for people to set aside emotion that causes you to anchor (as Matt did) until after you have been burned at least once.

Sometimes it takes more than once. But it’s almost always less expensive to learn this lesson from someone else’s experience.

Related

• Is the Stock Market Really in a Bear Market? Maybe. Maybe Not. • When Is a Stock Market Crash Not Really a Stock Market Crash? • MBA Guide to Dealing with Higher Mortgage Interest Rates, Part 2 — How Much Money Will You Save?

Recent

• The Deafening Silence on Stock Buybacks from Centrist Democrats • 2 Reasons Populations Are Collapsing in Developed Countries • 3 Key Facts Everyone Is Missing About Biden’s Student Loan Debt Relief

Potential to Change the Way You Think

• Why Are Fundamental Human Values Critically Important for Successful, Enduring Brands? • Life Expectancy vs. Healthcare Costs in the U.S. (and Japan, Germany, France, Spain, Portugal, etc.) • (1a/9) “Top-Down” Makes More Sense Than “Left-Right” in the U.S.

Want me to cover a topic? Please post suggestions in the comments, and I’ll use your input to help prioritize my writing and research.

If you appreciate my writing, please share it on social media.

Want unlimited access to all Medium articles? Become a member!

Again, thank you for reading, subscribing, clapping, and sharing — your time and attention are deeply appreciated!