30Y in 30D • Y16: The Total Cost of Ownership of Your House

Potential risks — costs that catch new homeowners by surprise. How much does your house really cost? Hint: it’s not just the sales price.

Related and recent articles

(Full list of “30 Years in 30 Days” Series articles at bottom of this page.) • 30Y in 30D, Y15: Simple Question, Complex Answer — The True Purchase Price of Your Home • 30Y in 30D, Y14: What Kind of People Are Getting Loans for Houses Right Now? • 30Y in 30D, Y11: Dream Home or Financial Freedom? Rethinking the True Cost of Stretching • 30Y in 30D • Year 10: A Tale of Two Eras — Home Buying in 1972 and 2023 • 30Y in 30D • Year 3: Early Extra Payments Are Magical • Kickstarting “30 Years in 30 Days” — Decades of Mortgage Wisdom in 1 Month • It’s Open Enrollment Season for Medicare Advantage Which Means It’s Open Hunting Season on Senior Citizens • Has U.S. Healthcare Really Become a Mob Protection Racket?

(Subscribe to receive email notifications when I post new articles in this series and on other topics.)

Introduction

In the previous article, we looked at the “The True Purchase Price of Your Home.”

The Total Cost of Ownership of a House is different.

The “True Cost of Purchasing a House” is part of the “Total Cost of Ownership.”

But only a part.

The Total Cost of Ownership of a house goes beyond just the purchase price of your house.

Quick exercise for today

The median purchase price of a house in Cincinnati, Ohio is $235,000. If a homebuyer gets a 30-year, 8% fixed-rate mortgage for the full $235,000, what is your best guess for the “total 30-year cost” of that house?

Is it $400,000? $600,000? $650,000? A lot more? A lot less?

Write your guess down, and then compare it to what we will see the 30-year cost ends up being by the end of this article.

The Total Cost of Ownership

The Total Cost of Ownership of your house includes all the things that you (1) have to pay for along the way and (2) might choose to pay for along the way.

“Have to buy or pay for” items generally include:

- Property taxes

- Homeowner’s insurance

- Mortgage insurance (PMI) if you have put down less than a 20% down payment

- Utilities costs

- Home Maintenance & Repairs

- HOA Dues if you live in, say, a gated community or a condo building with HOA dues.

Optional items include:

- Furnishing & Decoration

- Landscaping/Gardening

“Smart to pay for” items include:

- Home-specific Emergency Fund

Today we’re looking at typical costs for a median-priced house in Cincinnati, Ohio. The median house price in Cincinnati is $235,000.

If you live near cities Boston or San Francisco or Seattle or New York City, your median priced house will certainly be higher than the $235,000 median house price in Cincinnati. And if you happen to live in Kokomo, IN or Waterloo, Iowa, your median price will be lower.

I’m going to focus today only on the must-have items and the one “smart to have” item. If you’re someone who expects to have substantial furnishing expenses or landscaping/gardening expenses, you will want to add those categories to your own spreadsheet.

For some of these costs where there was an exact number, I used that exact number.

For example, the state property tax in Ohio of 1.56% per year.

For costs where there was a “typical range” as opposed to an exact number, I took the midpoint of the range.

Your mileage not only may vary…it will vary depending on your prices for homeowners insurance, mortgage insurance (PMI), utilities, etc.

And speaking of PMI, since the requirement for that goes away once your equity in the house reaches 20%, we have to factor that in. For simplicity’s sake at the moment, though, I am treating PMI as an expense that will go all the way through the 30-year payoff period instead of ending right around the end of the 14th year (i.e., when equity in the house hits the 20% level.)

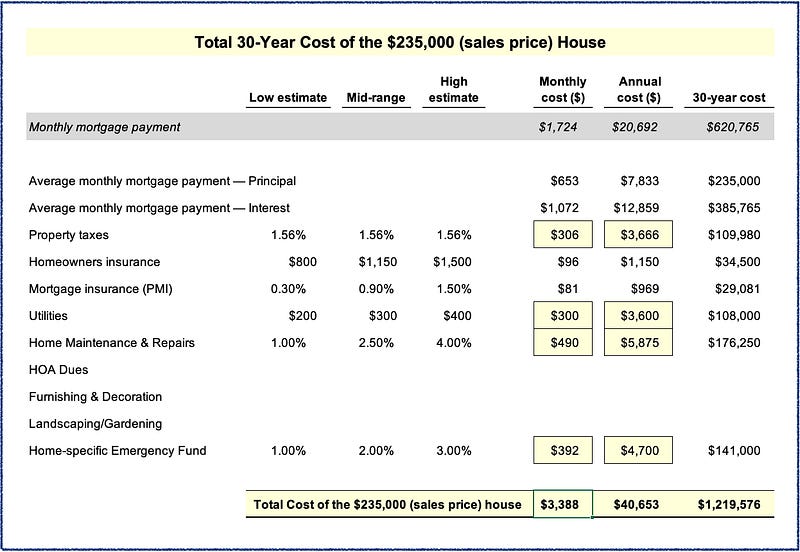

Here’s what the numbers look like.

My takeaways from this table

- The single biggest expense overall — and it’s not even close — is the Total Interest Paid. The second biggest expense is the principal repayment (although “Home Maintenance & Repairs) is close behind it.

- Besides the monthly mortgage payment (principal + interest), there are 4 house-related expenses that are large enough to demand our attention: (1) property taxes; (2) utilities; (4) home maintenance and repairs; and (4) a home-specific emergency fund. If you’re going to try to save money on your house — AFTER having done what you can to save money on “Total Interest Paid” — these 4 items are a good place to start.

- When you look at the TOTAL cost of owning this median house in Cincinnati, it’s roughly TWICE the cost of the monthly mortgage payment. Your reaction to this might be, “Jeff, this can’t possibly be true. The mortgage payment each month was already feeling too expensive to me…but you’re telling me that the actual total cost is TWICE that…?” Go through these expenses line by line and see which ones apply or don’t apply to you. I think you’re going to find that I was conservative on the estimates and that your actual “total cost of ownership” might be more than twice as much as your monthly mortgage payment.

- Remember that I didn’t include amounts for HOA dues; furnishing & decoration; or landscaping/gardening even though the typical homebuyer will probably have expenses in at least one of these areas. As a matter of fact, I was talking the night before last with someone I’ve known forever. This guy bought his first house in early 2022, and while he was fortunate enough to lock in a 30-year fixed mortgage rate of 3.25%, he is feeling now as though he overbought some and stretched himself more than he is comfortable with. (See: “Dream Home or Financial Freedom? Rethinking the True Cost of Stretching”) And he is also struggling with the decision about whether and when to buy furniture — he has a couple rooms in the new house that are still empty except for the carpet.

- The PMI number shown is $29,081 for the 30-year cost. However, PMI in this example only gets paid until near the end of Year 14. That is when you reach the point where your equity in the house reaches 20%, and you stop being required to have PMI — so the monthly PMI payments stop at that point. To keep things simple here, I spread out those “almost-14 years” worth of monthly payments over the 30–year life of the mortgage in the spreadsheet table above.

- Finally, my gut feel on the Homeowners Insurance estimate of $1,150 per year is that: (1) it is probably low; and (2) depending on what happens vis-a-vis climate change in Ohio and in other states, you would be at risk of your insurance company significantly increasing insurance premiums in the future or even deciding — for whatever reason — to leave the state and stop providing insurance. If I were doing the budgeting here, I would probably add at least 50% to that homeowners insurance number to start banking money for any difficulties in getting or retaining insurance in the future. So instead of $1,150 per year, I would probably budget at least $1,600 or $1,700 per year.

I hope the above list of expenses:

- gives you a framework that makes it easy for you to create your own to budget list;

- gets you thinking clearly about your total cost of ownership.

- helps you make smart decisions about how to maximize value and minimize cost when it comes to your house;

- and most importantly, helps you save hundreds of thousands of dollars.

Finally, how does this Total Cost of Ownership compare to the hypothetical offer to sell that our Cincinnati homebuyer “received” in the previous article?

Recap from previous article:

You bought a house for $235,000 in mid-2023. Standard 30-year mortgage for the entire $235,000 — nothing fancy or exotic here.

Your family and you live in the house for the next 30 years. Life is good. (…or at least as good as it’s going to be in a time of dramatic climate change…but hey, that’s a topic for another day.)

In mid-2053 — just weeks after you finally finish paying off your mortgage (yay!) — someone comes along and offers to buy your house for $352,500.

Your wife and you have just retired, and you were already thinking about downsizing your home, so this is great timing. You accept the offer as is.

And you pat yourself on the back for making a 50% profit on your house. ($352.5K / $235K = 150%.)

But the previous article taught us that for people who use a mortgage for the purchase, we have to also include the Total Interest Paid. For this house, the Total Interest Paid was $385,700.

And that meant the total cost to purchase this house was $620,700.

So that offer to buy the house for $352,500 didn’t represent a 50% gain on your investment in the house.

Rather, it represented a loss of $268,200 ($352,500 — $620,700 = –$268,200) — and that would work out to a 43% loss on your 30-year investment in the house.

But wait — if we look at the Total Cost of Ownership of the house, the gain/loss number changes…

…and not for the better.

Now we know the Total Cost of Ownership of this house is actually $1,219,600.

So that $352,500 offer from someone who wants to buy your house (30 years in the future) represents a loss of $867,000 . . . which is a 71% loss on your investment in the house!

Thoughts…?

Reactions…?

Thank you for reading, subscribing, clapping, and sharing — I appreciate your time and attention.

Related and recent articles

• 30Y in 30D, Y16: The Total Cost of Ownership of Your House • 30Y in 30D, Y15: Simple Question, Complex Answer — The True Purchase Price of Your Home • 30Y in 30D, Y14: What Kind of People Are Getting Loans for Houses Right Now? • 30Y in 30D, Y13: What Does It Take to Pay Off a 30-Year Mortgage in 15 Years? • 30Y in 30D, Year 12: CBS News’ Version of (Not) Helping You Save on Mortgage Interest • 30Y in 30D, Year 11: Dream Home or Financial Freedom? Rethinking the True Cost of Stretching • 30Y in 30D • Year 10: A Tale of Two Eras — Home Buying in 1972 and 2023 • 30Y in 30D • Year 9: Visualizing Savings — Mortgage Charts that Matter • 30Y in 30D • Year 8: The Mechanics of Mortgage Interest — What Really Matters • 30Y in 30D • Year 7: The Big Payoff of Early Extra Payments • 30Y in 30D • Year 6: Mortgage Power Play with a Single $100 Extra Payment • 30Y in 30D • Year 5: Are Car Buyers Smarter than Homebuyers? • 30Y in 30D • Year 4: Accelerate Payoff Via Extra Monthly Payments • 30Y in 30D • Year 3: Early Extra Payments Are Magical • 30Y in 30D • Year 2: Rapid Progress on the 30-Year Mortgage •30Y in 30D • Year 1: Starting Strong on the Mortgage Journey • Kickstarting “30 Years in 30 Days” — Decades of Mortgage Wisdom in 1 Month • A Friend Texted to Ask “Who I Favored” for 2024 but Hated My Answer • Has U.S. Healthcare Really Become a Mob Protection Racket?

(Subscribe to receive email notifications when I post new articles in this series and on other topics.)