30Y in 30D, Y14: What Kind of People Are Getting Loans for Houses Right Now?

Who exactly is able to afford a house mortgage these days in the U.S.? A question from a reader sparks thoughts.

Related and recent articles

(Full list of “30 Years in 30 Days” Series articles at bottom of this page.) • 30Y in 30D, Y11: Dream Home or Financial Freedom? Rethinking the True Cost of Stretching • 30 Years in 30 Days • Year 10: A Tale of Two Eras — Home Buying in 1972 and 2023 • 30 Years in 30 Days • Year 3: Early Extra Payments Are Magical • Kickstarting “30 Years in 30 Days” — Decades of Mortgage Wisdom in 1 Month • It’s Open Enrollment Season for Medicare Advantage Which Means It’s Open Hunting Season on Senior Citizens • Has U.S. Healthcare Really Become a Mob Protection Racket?

(Subscribe to receive email notifications when I post new articles in this series and on other topics.)

This was the question from Hanako in response to the previous article in this series, 30Y in 30D, Y13: What Does It Take to Pay Off a 30-Year Mortgage in 15 Years?:

“I am curious… what kind of people are getting loans for a house right now? It just seems impossible…”

This is an excellent question, and the more that I thought about this, the more angles to the story kept jumping out.

Here is the first piece — a general overview to start us on the topic of “Who Is Buying Houses in the U.S. in Late 2023?”

Part 1. What kinds of houses are getting built?

Let’s break this up into two pieces: (1) the perspective of homebuilders and (2) the perspective of homebuyers.

From the perspective of homebuilders

What kinds of new houses are homebuilders building these days and putting onto the market?

The short answer is, “not many starter homes.”

And that’s a problem because generally speaking, “starter homes” are what first-time buyers in the U.S. look for.

BusinessInsider didn’t pull any punches in early 2023 when they proclaimed that “First-time homebuyers are pretty much screwed in 2023.” As they noted:

- Starter homes are typically more affordable houses that are purchased by new home buyers.

- However, these entry-level homes are disappearing from the market as builders focus on more lucrative projects.

- Their absence has made it difficult for many first-time buyers to afford homeownership.

- According to data from the US Census Bureau, in November 2022, not a single newly-built home sold in the US was under $200,000.

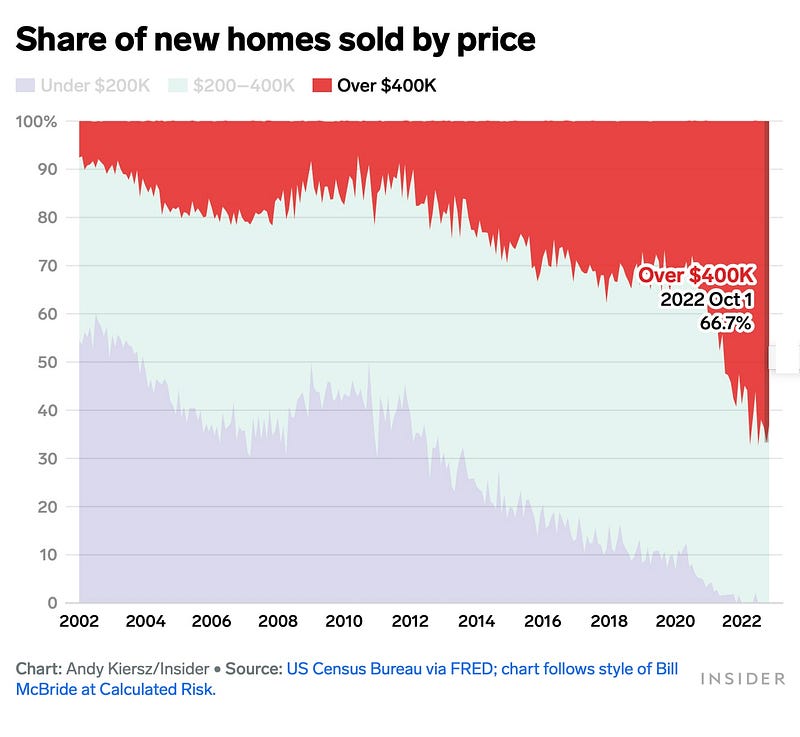

Note: There is a great chart midway down the BusinessInsider article that illustrates perfectly how much the “Over $400K” part of the market has come to dominate the “Share of new homes sold by price.” It shows how over the past decade the “Over $400K” segment of the market has gone from less than 20% of sales to 67% of sales by late 2022.

See the red section at the top of the chart? See how it grows to be 66.7% of the market by October 1, 2022?

Those are all houses that are too expensive to be purchased by the median buyer in the U.S.

See the light purple section at the bottom of the chart? See how it dwindles down to zero — literally, zero — percent of the market by 2022? That’s the “Under $200K” portion of the U.S. housing market. By late 2022 there were literally ZERO home sales anywhere in the U.S where the sale price of the house was less than $200,000.

Seriously, the number wasn’t “almost zero.”

It was zero, according to U.S. Census Bureau data.

Note: I will follow up in the next few days on this point about median income earners not being able to afford to buy a median priced house.

I did a budgeting exercise to see what median family expenses look like for a family of four in the midwest with the median income. It was disappointing — but not surprising — to see how difficult it is for a median income family to buy a median-priced house today. It’s actually kind of impossible.

I’ll share this budget along with commentary in the next few days. I wish I could say that it’s going to be a lot of happy talk, but…probably not. I had a certain expectation about what the numbers were going to show, but I was still taken aback by how brutal the numbers are.

(Subscribe to receive an email notification when I post the article with the budgeting info for our median family and commentary about what the implications probably are for non-wealthy buyers.)

What about sales of existing homes?

First, we know that by late 2022, no houses — including existing homes — were selling for less than $200,000.

And by late 2022, well over 50% of existing homeowners with a mortgage had refinanced their mortgage so that they had a 3-ish percent rate on their mortgage — those folks are locked in for years now, probably regardless of the price they paid for their house.

The BusinessInsider article also noted that while “from 2000 until the beginning of the pandemic in 2020, on average, new homes [only] made up 11% of total housing inventory,” things have changed.

What “things” are they talking about?

They are referring to the fact that “today that [new home] share is 29%” because existing homeowners who have locked in 3% rates on their current mortgage can’t afford to move if it means getting a new mortgage at 8%. So the number of existing home sales is down.

In other words, people who own homes right now — “existing homes” — are going to hold onto their current homes for dear life if they have a 3% mortgage on them.

These existing homes are going to be off the market for years — if not decades — to come.

This piece of the situation is forcing a really important long-term, unchangeable distortion into the U.S. housing market dynamics.

Further, this distortion in sales of “existing homes” isn’t going away.

And as the chart in the BusinessInsider article shows, 2/3 of that larger share of new homes fall into the “Over $400K” segment. These are homes that are generally out of the reach of the median income homebuyer in the U.S., especially given today’s 8% interest rates on 30-year fixed mortgages.

So there just isn’t that much house supply — whether new or existing — that fall into the category of “starter homes.”

From a supply perspective, a large percentage of the U.S. population — probably at least 60% of the population — is shut out of the housing market.

It’s not just that people can’t afford the houses they would normally be buying as starter homes.

It’s that the supply of those starter homes is far lower than it would normally be.

Which means that buyers who would have been struggling to buy these “least expensive” houses have to actually be looking at more expensive houses where it’s even less of a possibility that they’ll have the money to buy them.

Part 2. What can homebuyers actually afford to buy?

There are several key segments of homebuyers in 2023, including:

- institutional investors

- wealthy (enough) individuals who are buying 2nd homes, 3rd homes, etc.

- non-wealthy individuals and families who are buying a house for their primary residence

For today, I’m going to focus in only on the third segment above, which is the one that I think Hanako was focused on — the individuals and families for whom buying a house at today’s prices and mortgage interest rates is so much less affordable now than it was only two years ago.

For these non-wealthy homebuyers, their main focus is tends to be the size of the monthly payment.

That’s it.

Just the monthly payment.

Not the Total Amount of Interest they will pay over the life of the mortgage.

Just the monthly payment amount. That’s all they care about.

That’s all they can afford to care about.

And that’s because they are already having a tough time paying for the expenses that a median person in current-day America has if they’re only earning a median income.

It’s not just the general inflation of the past 2 or 3 years — food, groceries, gas, etc.

It’s not even the inflation in housing costs — whether house sales prices or rent prices.

It’s that over the past 40–50 years, there has been a relentless rise in price of the “big, fixed costs” in American life that regular working class people don’t have any choice about whether they pay or not, including:

- healthcare costs

- the already-discussed housing costs

- education costs

- childcare costs

The rise in cost of all of these “gotta-have” and “can’t not have” costs of life have been devastative in obvious and non-obvious ways to Americans in the Bottom 80–90% of the population.

If you’re below the age of 50 or so and it feels as though your economic/financial life hasn’t been as easy or fruitful as it was for your parents/grandparents, it’s not your imagination.

The actual economic numbers bear it out.

Boomers (in particular) can condescend to you all they want that, “oh, we had it just as tough as you, but we worked hard and saved money and didn’t waste money on avocado toast and Netflix subscriptions so that we were able to buy our first houses. It’s always been hard. You Millennials and Gen Z’ers just need to stop whining and start working.”

But they are incorrect, and no matter how much they say something that is either irrelevant or untrue, it doesn’t change the fact young and middle-aged adults today are dealing with dramatically higher prices for the non-negotiable, “have to buy no matter what” necessities of life than people coming of age in the 60s and 70s and early 80s did.

That’s a fact.

Side note

I’m in Japan right now, and I’ve been traveling on a JR Pass the last couple weeks visiting parts of the country I’ve never been to before — Fukuoka, Nagasaki, Akita, Aomori — in addition to return visits to Hiroshima, Sendai, and Nagoya.

As I’m riding on the shinkansen (“bullet train”) and gazing out the window, I keep looking at the communities and clusters of homes I can see from the train.

I’m struck by how good even the not-so-great houses look when I see them through “American eyes.”

And the good ones look pretty great, especially when I consider that the Japanese families who own them probably are not gambling their family’s financial future on the value of the home needing to go up a lot over the next 30 years for the purchase to have made economic sense.

Here are a few photos:

I haven’t dug into detailed data on Japanese housing in Tokyo and in other parts of Japan, but from numbers I’ve seen and friends I’ve spoken with…

It’s fair to say that housing in Japan is an expense, and it’s generally affordable (enough.)

The same cannot be said about American housing today.

Thank you for reading, subscribing, clapping, and sharing — I appreciate your time and attention.

Related and recent articles

• 30Y in 30D, Y16: The Total Cost of Ownership of Your House • 30Y in 30D, Y15: Simple Question, Complex Answer — The True Purchase Price of Your Home • 30Y in 30D, Y14: What Kind of People Are Getting Loans for Houses Right Now? • 30Y in 30D, Y13: What Does It Take to Pay Off a 30-Year Mortgage in 15 Years? • 30Y in 30D, Year 12: CBS News’ Version of (Not) Helping You Save on Mortgage Interest • 30Y in 30D, Year 11: Dream Home or Financial Freedom? Rethinking the True Cost of Stretching • 30Y in 30D • Year 10: A Tale of Two Eras — Home Buying in 1972 and 2023 • 30Y in 30D • Year 9: Visualizing Savings — Mortgage Charts that Matter • 30Y in 30D • Year 8: The Mechanics of Mortgage Interest — What Really Matters • 30Y in 30D • Year 7: The Big Payoff of Early Extra Payments • 30Y in 30D • Year 6: Mortgage Power Play with a Single $100 Extra Payment • 30Y in 30D • Year 5: Are Car Buyers Smarter than Homebuyers? • 30Y in 30D • Year 4: Accelerate Payoff Via Extra Monthly Payments • 30Y in 30D • Year 3: Early Extra Payments Are Magical • 30Y in 30D • Year 2: Rapid Progress on the 30-Year Mortgage •30Y in 30D • Year 1: Starting Strong on the Mortgage Journey • Kickstarting “30 Years in 30 Days” — Decades of Mortgage Wisdom in 1 Month • A Friend Texted to Ask “Who I Favored” for 2024 but Hated My Answer • Has U.S. Healthcare Really Become a Mob Protection Racket?

(Subscribe to receive email notifications when I post new articles in this series and on other topics.)