30Y in 30D, Y11: Dream Home or Financial Freedom? Rethinking the True Cost of Stretching

30 Years in 30 Days, Year 11: Was it ever really worth “stretching” for that better or bigger house? What is the true cost of a homebuying stretch? Is conventional wisdom about stretching for the better house just plain wrong?

Related and recent articles

(Full list of “30 Years in 30 Days” Series articles available at bottom of this article.) • 30 Years in 30 Days • Year 10: A Tale of Two Eras — Home Buying in 1972 and 2023 • 30 Years in 30 Days • Year 9: Visualizing Savings — Mortgage Charts that Matter • 30 Years in 30 Days • Year 6: Mortgage Power Play with a Single $100 Extra Payment • 30 Years in 30 Days • Year 3: Early Extra Payments Are Magical • 30 Years in 30 Days • Year 1: Starting Strong on the Mortgage Journey • Kickstarting “30 Years in 30 Days” — Decades of Mortgage Wisdom in 1 Month • A Friend Texted to Ask “Who I Favored” for 2024 but Hated My Answer • Has U.S. Healthcare Really Become a Mob Protection Racket?

(Subscribe to receive email notifications when I post new articles in this series and on other topics.)

Is conventional wisdom about stretching for the better house just plain wrong? Or is it perhaps “wise” for your mortgage lender…and maybe not so smart for you?

Imagine this.

Somebody has been shopping for the last year or more for a house to buy.

She can’t find the perfect house — and for as much as a new house costs these days, she sure feels as though it should be perfect.

Or at least, “really good.”

And so she keeps chasing the market as prices continue to spiral upward.

Finally she finds a house that is within her budget and that is “ok enough” even if it’s not everything she was hoping for. It’s $400,000, right at the upper range of her budget.

And she is about to commit to buying it . . . when she sees one more house.

But it’s this “one more house” that gets her excited.

It’s a little bigger and little better, and it really would be a better fit for her needs. But at $474,100, it costs 10% more than the other house.

So it’s a stretch to buy it. The monthly costs that this Stretch House would require have her worried (not the actual $440,000 purchase price.)

Still, she rationalizes the extra costs:

- It’s a house that she is going to be more comfortable in and happier with. This is no small thing.

- The house will sell for more when it comes time for you to sell, so she will make more money over the longer-term, even if it’s costing her more on a monthly basis.

- And somehow — somehow — she will find the extra money each month to make the higher payment. After all, it’s “only” an extra 10%.

Rationalization #1 is hard — impossible? — to argue with. By now she has probably looked at enough houses that she has a good idea of what it would take to really make her happy. For the sake of this conversation, I’m comfortable trusting the intuition that she has certainly built after looking at so many houses and weighing the compromises with each one.

But Rationalization #2? Well, I’m happy to argue against this rationale, because it is more tenuous…and may well turn out to be wrong. Here’s my thinking:

- There is no guarantee that house prices will be higher on the day she wants to sell than they were on the day she will have bought the house.

- What has been true is that over the past 4 decades, the housing market has been in a long-term bull market. There have been short-term pullbacks — like in 2007–2009 — but up until now, prices have always continued in general to rise. It’s hard to imagine, though, that the next 40 years will see the same general 10X increase in prices that the past 40 or 50 years delivered.

There’s a different way to think about the cost of doing that 10% (or larger) “stretch” to buy the house, however, that a really savvy buyer should be doing.

Let me explain.

What’s the true cost of stretching to buy the house that costs 10% more?

Someone who works in real estate told me recently that she just didn’t have the cushion to pay extra each month on her mortgage because she had stretched as far as she could to buy her house.

She was saying that she had no extra money to be able to pay 10% extra each month on her mortgage, regardless of how much interest money it might save her and regardless of how much faster she’d be able to pay down her 30-year mortgage.

That got me thinking.

What if she had bought her original, “non-stretch” house BUT had then used what would have been the money for her stretch house to just pay 10% extra each month on her original, “non-dream” house?

How much interest would she have saved by doing this?

How much faster would she be able to pay off the 30-year mortgage on the original house?

And that got me thinking even more. I realized that the right way — the smart, savvy way — to think about the true cost of “the stretch” was to look at the difference in costs vs. the difference in what you get.

In “economist-speak,” that’s the marginal cost vs. the marginal value.

Use these two numbers (immediately below) to calculate the “marginal cost”:

- How much Total Interest you would pay with “The Stretch House”; and

- How much Total Interest you would pay with the original house IF you paid the Stretch Money each month as extra with your regular mortgage payments.

and then to compare the difference between the two numbers against how much you get with the “Stretch” House, which would be the “marginal value.”

Let’s look at an example of this.

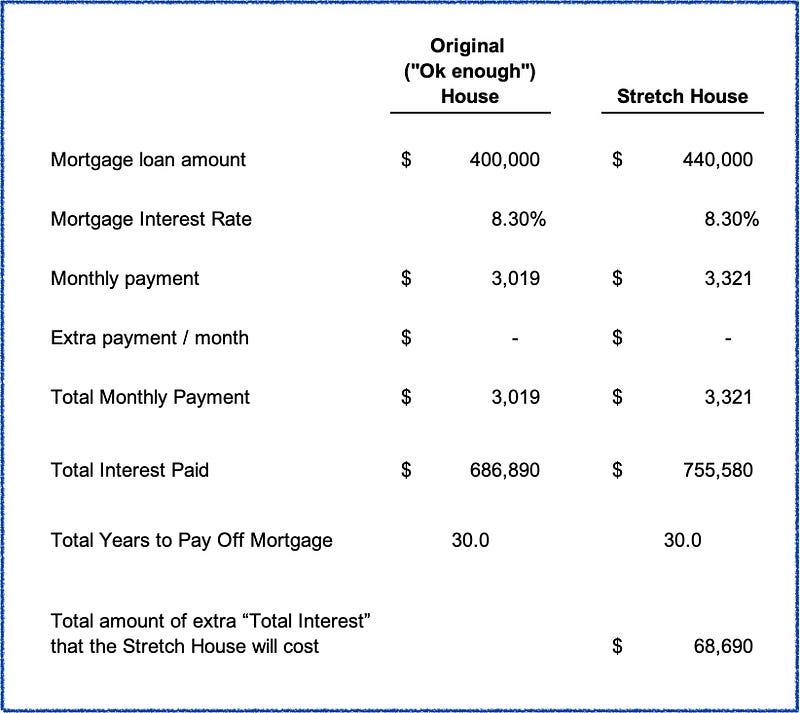

The comparison between (1) the original “Ok Enough” House and (2) the Stretch House

First and partially as a warmup, let’s do a quick comparison between the original “Ok Enough” House and the “Stretch” House:

Points to notice:

- At $440,000, the mortgage for the Stretch House is exactly 10% more than the mortgage for the original “Ok Enough” House. (I chose 10% as a reasonable amount extra — your own personal “Stretch House” might be more or less than that amount.)

- The monthly payment for the Stretch House is exactly 10% more than the monthly payment for the “Ok Enough” House.

- And the Total Interest Paid over the 30-year life of the mortgage for the Stretch House is exactly 10% more than it would be for the “Ok Enough” House.

This warmup comparison was simple enough. But it doesn’t get to the real comparison we need to do.

Now let’s go make our conversation MUCH more interesting.

It’s inspiration time

Let’s think about this a little differently now.

Remember I told you about the real estate professional who told me that she really couldn’t afford to pay anything extra because she had committed every. last. spare. dollar. she. had. to “stretch” and buy the house she really wanted?

But . . . the fact is, she DID have the extra money for the Stretch House.

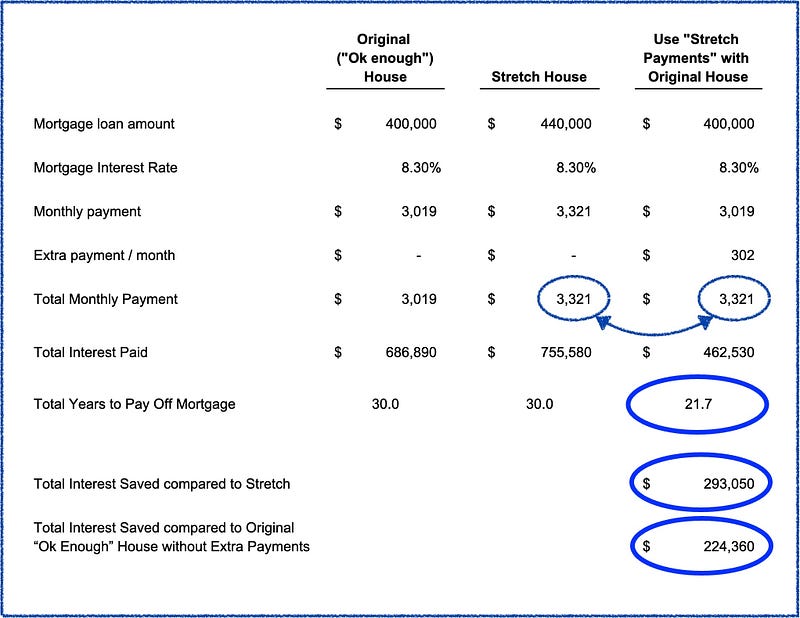

So what if — what if — she had stuck with the “Ok Enough” House BUT took the extra $302 each month (the extra 10%) and just used it to make extra payments each month on her original house?

What does that do to the numbers?

Take a look at the table below:

Once I started thinking in these terms, it totally changed the way that I think about the cost of “stretching” to get a better/bigger house.

Here’s why.

First, the monthly payments are the same between (1) the Stretch House (column 2) and (2) where we buy the original house and use the extra 10% to pay down that house’s mortgage faster and save on interest (column 3) — they are $3,321 in each case.

There are some advantages and disadvantages to going with the Column 3 approach I have laid out above.

Let’s start with the advantages of Column 3 — “Use Stretch Payments with the original house.

- We save $293,000 — that’s almost $300,000! — in Total Interest Paid over the life of the mortgage. This is a nest egg of money that could be used for sending a kid to college or as retirement money for you — lots of options for how you can make good use of an extra $300,000 in 22 years.

- We pay the mortgage down in 21.7 years instead of 30 years.

And there are 2 disadvantages with Column 3.

- Our buyer is NOT getting her preferred house — i.e., the “Stretch House.” She is instead buying the one that was sorta, kinda good enough (…but boy, she really did want to stretch and get the other house.)

- If/when it comes time to sell her house at some point in the future it is the case that housing market prices have gone up, then it is reasonable to assume that the Stretch House should sell for more. Today’s buyer could well make some amount of extra money on the sale. How much more? We can’t know that. Is it guaranteed that housing market prices will be higher at the point in time when our buyer wants to sell? No, it is definitely not guaranteed.

But you know what is guaranteed?

That if you do the 10% extra monthly payments with the original $400,000 house, you WILL save $293,000 versus the case where you bought the Stretch House.

So what is the true cost of the Stretch House?

Instead of thinking of it as “just pay $302 extra each month and then you get the Stretch House you would prefer to get,” it is a LOT more useful to frame it as:

“The True Cost to our buyer of getting her Stretch House is that (1) she will leave almost $300,000 on the table and (2) she will take the full 30 years to pay off her 30-year mortgage instead of finishing it up in 21.7 years.”

Now, there might be some buyers who are willing and able to leave that $300,000 on the table and take the entire 30 years to pay off their mortgage in order to get the house that is going to make them more perfectly happy.

That’s fine.

But that’s the tradeoff you need to think about.

And I suspect that there are a lot of homebuyers outside of the Top 10% or Top 20% of the housing market who would prefer to have (1) an extra few hundred thousand dollars in their bank account at the end of (2) an abbreviated/shortened mortgage.

But again, this is the buyer’s choice to make.

And now you have a decision framework for thinking about this that is better than just blindly accepting a “conventional wisdom” truism that dates back to the experience your parents or grandparents had buying a home decades ago.

Now you can look at the True Costs of the Stretch House.

And you’re better equipped to ask — and answer — the question, “Is a few hundred thousand dollars better off in my mortgage lender’s pocket, or is it better off in my pocket?”

Thank you for reading, subscribing, clapping, and sharing — I appreciate your time and attention.

Related and recent articles

• 30Y in 30D, Y16: The Total Cost of Ownership of Your House • 30Y in 30D, Y15: Simple Question, Complex Answer — The True Purchase Price of Your Home • 30Y in 30D, Y14: What Kind of People Are Getting Loans for Houses Right Now? • 30Y in 30D, Y13: What Does It Take to Pay Off a 30-Year Mortgage in 15 Years? • 30Y in 30D, Year 12: CBS News’ Version of (Not) Helping You Save on Mortgage Interest • 30Y in 30D, Year 11: Dream Home or Financial Freedom? Rethinking the True Cost of Stretching • 30Y in 30D • Year 10: A Tale of Two Eras — Home Buying in 1972 and 2023 • 30Y in 30D • Year 9: Visualizing Savings — Mortgage Charts that Matter • 30Y in 30D • Year 8: The Mechanics of Mortgage Interest — What Really Matters • 30Y in 30D • Year 7: The Big Payoff of Early Extra Payments • 30Y in 30D • Year 6: Mortgage Power Play with a Single $100 Extra Payment • 30Y in 30D • Year 5: Are Car Buyers Smarter than Homebuyers? • 30Y in 30D • Year 4: Accelerate Payoff Via Extra Monthly Payments • 30Y in 30D • Year 3: Early Extra Payments Are Magical • 30Y in 30D • Year 2: Rapid Progress on the 30-Year Mortgage •30Y in 30D • Year 1: Starting Strong on the Mortgage Journey • Kickstarting “30 Years in 30 Days” — Decades of Mortgage Wisdom in 1 Month • A Friend Texted to Ask “Who I Favored” for 2024 but Hated My Answer • Has U.S. Healthcare Really Become a Mob Protection Racket?

(Subscribe to receive email notifications when I post new articles in this series and on other topics.)