30 Years in 30 Days • Year 9: Visualizing Savings—Mortgage Charts that Matter

Today in “Year 9” of our 30-year mortgage journey, I want to use simple charts to illustrate what we’ve seen so far and to add a new insight or two.

Related and recent articles

(Full list of “30 Years in 30 Days” Series articles available at bottom of this article.) • 30 Years in 30 Days • Year 10: A Tale of Two Eras — Home Buying in 1972 and 2023 • 30 Years in 30 Days • Year 6: Mortgage Power Play with a Single $100 Extra Payment • 30 Years in 30 Days • Year 3: Early Extra Payments Are Magical • 30 Years in 30 Days • Year 2: Rapid Progress on the 30-Year Mortgage • 30 Years in 30 Days • Year 1: Starting Strong on the Mortgage Journey • Kickstarting “30 Years in 30 Days” — Decades of Mortgage Wisdom in 1 Month • A Friend Texted to Ask “Who I Favored” for 2024 butHated My Answer • Has U.S. Healthcare Really Become a Mob Protection Racket?

(Subscribe to receive email notifications when I post new articles in this series and on other topics.)

Today in “Year 9” of our 30-year mortgage journey, I have created simple charts to illustrate what we’ve seen so far and to add a new insight or two.

If you have any suggestions for other charts or additions to the ones below that would help you as you’re thinking about mortgages and loans, please share them in the comments below. If possible, I’ll add them in to the mix.

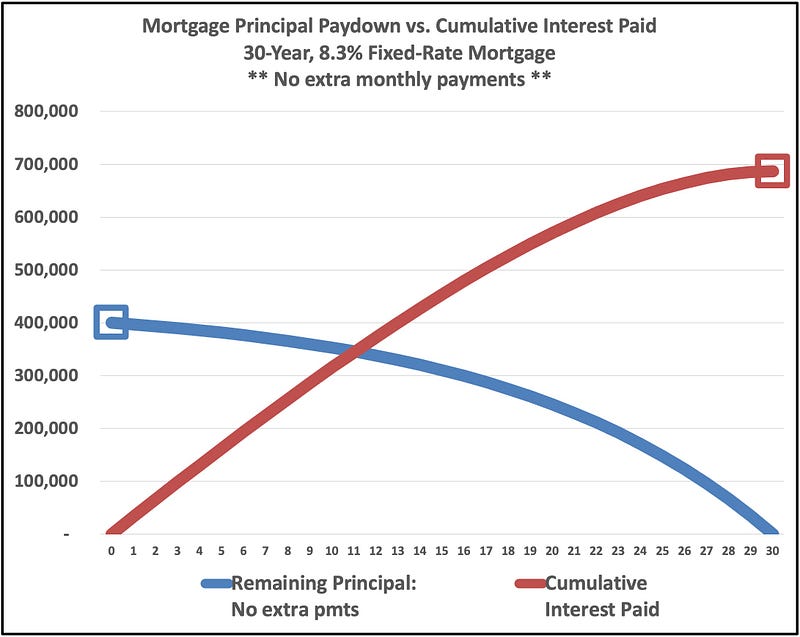

1. Back to Basics

Here is the most basic view possible of what happens with a 30-year mortgage:

Just a few takeaways here, but you get them at a glance:

- The mortgage amount borrowed is $400,000 — that’s the point with the hollow blue square around it.

- Over the course of 30 years, that amount gets paid down to zero — very gradually at first and then more and more rapidly over the years.

- The cumulative interest paid — the red line — starts at $0 back in Year 0.

- Over the course of 30 years, the Total Interest Paid amount eventually works its way up to $686,890 by the end of Year 30.

- But check this out — really look hard at it — that red square is sitting on top of a MUCH larger number than the blue square is. In other words, we can see at a glance that over the course of this regular, nothing-very-special 30-year mortgage, a lot more money ($686,890) gets paid in interest than was originally borrowed ($400,000.)

Before we move on, take one more look at that chart and sear 2 things into your memory:

- The end of the red line is MUCH higher than the beginning of the blue line.

- The true cost of the house in this example is (1) that original “purchase price” of $400,000 PLUS (2) the cost of the Total Interest Paid, which is almost $687,000. So by the time you are done paying for it, the real cost of the house will be dramatically higher than the $400K “purchase price” you would probably have incorrectly fixed into your mind. (Note: there are nuances that we should factor in here such that in some ways the $687,000 won’t seem like quite so much money…but in other ways it will actually be more impactful than people realize in the moment. More on this later in this series.)

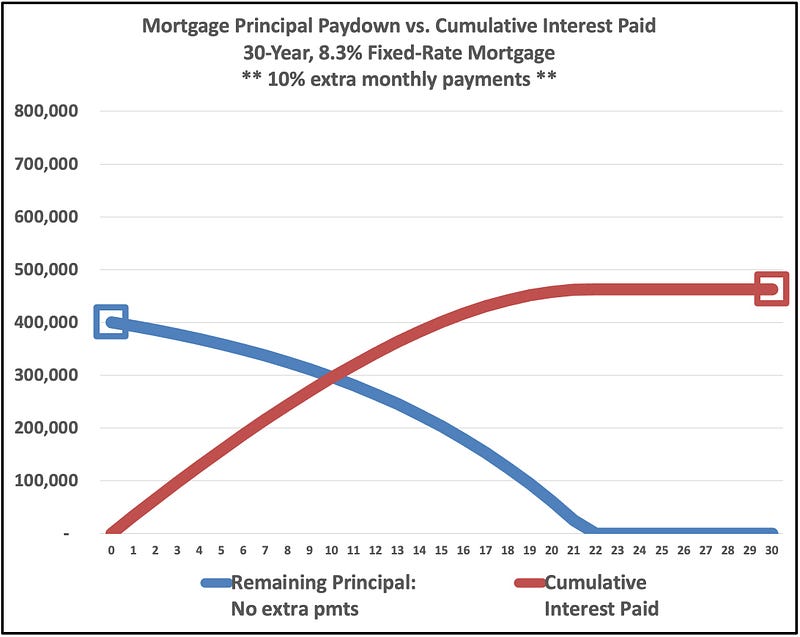

2. Paying 10% extra all the way through to the end of the mortgage

Now the story gets more interesting. My takeaways here are:

- Because we are paying extra each month — in this case, 10% extra with each regular monthly payment — we finish the mortgage around Year 21. Over 8 years early! That’s why both the red line and the blue line flatten between Years 21 and 22.

- While the “Total/Cumulative Interest Paid” number — i.e., the endpoint of the red line — is still higher than the $400,000 starting point for the mortgage principal, it’s a LOT closer than it was in the first chart. So paying extra each month really DOES make a difference.

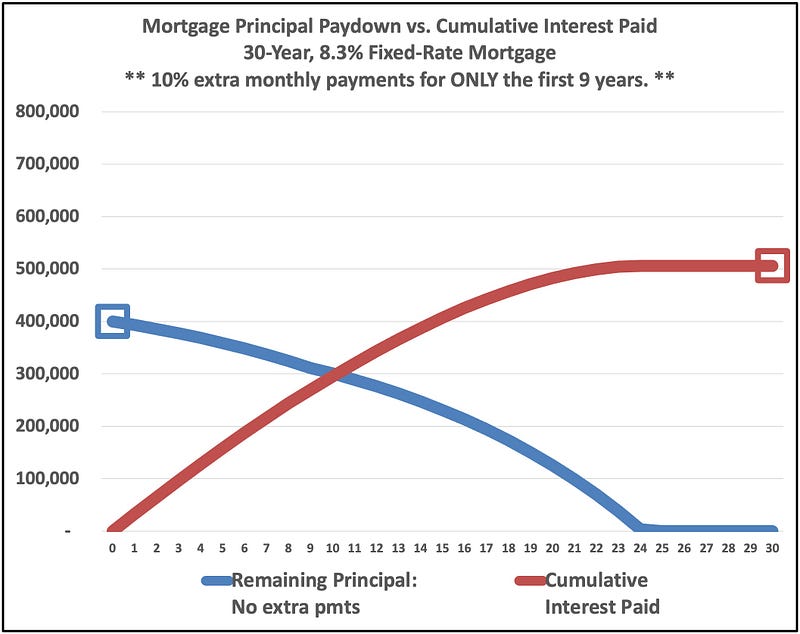

3. Paying 10% extra each month for ONLY the first 9 years

Takeaways

- Even though in this example we are only making the 10% extra payments for the first 9 years only — i.e., not for the entire length of the mortgage — we still get the mortgage principal fully paid down almost 6 years ahead of schedule in about 24 years instead of the original 30 years. Total Interest Paid is about $506,000, or almost $189,000 less than if we were making no extra payments at all.

- This $189,000 is over 80% of what we would save if we made 10% extra payments all the way through.

- Think about that. We only made the extra payments for the first 9 years, and that gets us to over 80% of what we would save if we did the payments for more than 20 years! The key takeaway here is that payments in the first few years are the most impactful in terms of (1) decreasing the interest you pay and (2) decreasing the number of years it takes to fully pay off the mortgage.

Again, please share comments and suggestions below if there are other charts or ways of thinking about this topic that you would find helpful.

Thank you for reading, subscribing, clapping, and sharing — I appreciate your time and attention.

Related and recent articles

• 30Y in 30D, Y16: The Total Cost of Ownership of Your House • 30Y in 30D, Y15: Simple Question, Complex Answer — The True Purchase Price of Your Home • 30Y in 30D, Y14: What Kind of People Are Getting Loans for Houses Right Now? • 30Y in 30D, Y13: What Does It Take to Pay Off a 30-Year Mortgage in 15 Years? • 30Y in 30D, Year 12: CBS News’ Version of (Not) Helping You Save on Mortgage Interest • 30Y in 30D, Year 11: Dream Home or Financial Freedom? Rethinking the True Cost of Stretching • 30Y in 30D • Year 10: A Tale of Two Eras — Home Buying in 1972 and 2023 • 30Y in 30D • Year 9: Visualizing Savings — Mortgage Charts that Matter • 30Y in 30D • Year 8: The Mechanics of Mortgage Interest — What Really Matters • 30Y in 30D • Year 7: The Big Payoff of Early Extra Payments • 30Y in 30D • Year 6: Mortgage Power Play with a Single $100 Extra Payment • 30Y in 30D • Year 5: Are Car Buyers Smarter than Homebuyers? • 30Y in 30D • Year 4: Accelerate Payoff Via Extra Monthly Payments • 30Y in 30D • Year 3: Early Extra Payments Are Magical • 30Y in 30D • Year 2: Rapid Progress on the 30-Year Mortgage •30Y in 30D • Year 1: Starting Strong on the Mortgage Journey • Kickstarting “30 Years in 30 Days” — Decades of Mortgage Wisdom in 1 Month • A Friend Texted to Ask “Who I Favored” for 2024 but Hated My Answer • Has U.S. Healthcare Really Become a Mob Protection Racket?

(Subscribe to receive email notifications when I post new articles in this series and on other topics.)