30 Years in 30 Days • Year 10: A Tale of Two Eras — Home Buying in 1972 and 2023

Decoding the affordability crisis in the modern housing market — how has buying a house in the U.S. changed since the 1970s?

Related and recent articles

(Full list of “30 Years in 30 Days” Series articles available at bottom of this article.) • 30 Years in 30 Days • Year 9: Visualizing Savings — Mortgage Charts that Matter • 30 Years in 30 Days • Year 6: Mortgage Power Play with a Single $100 Extra Payment • 30 Years in 30 Days • Year 3: Early Extra Payments Are Magical • 30 Years in 30 Days • Year 2: Rapid Progress on the 30-Year Mortgage • 30 Years in 30 Days • Year 1: Starting Strong on the Mortgage Journey • Kickstarting “30 Years in 30 Days” — Decades of Mortgage Wisdom in 1 Month • A Friend Texted to Ask “Who I Favored” for 2024 butHated My Answer • Has U.S. Healthcare Really Become a Mob Protection Racket?

(Subscribe to receive email notifications when I post new articles in this series and on other topics.)

When you talk with Baby Boomers, they often say that there is nothing fundamentally different with today’s housing market in the U.S. compared to when they were buying their first homes in the 1970s.

After all, it’s always been nerve-racking and a big investment to buy a house in any decade.

[Side note: Boomers also have a perspective based on their own life experiences when it comes to student loan debt and debt relief that is very out of step from the life experiences and needs of Gen X, Millennials and Gen Z student debtholders. I discussed this in “3 Things You Didn’t Know about Student Loan Debt and (Potential) Debt Cancellation” and included a chart that makes these generational difference very clear.]

And even though today’s 7% and 8% fixed 30-year mortgage rates seem extremely high compared to the low rates we have seen for the past 15-plus years, interest rates back in 1972 were — coincidentally enough — 8%.

So maybe buying a home hasn’t really changed all that much…?

Or has it?

Let’s look back to what it was like buying and owning a house in 1972 and compare it to the same experience today in 2023.

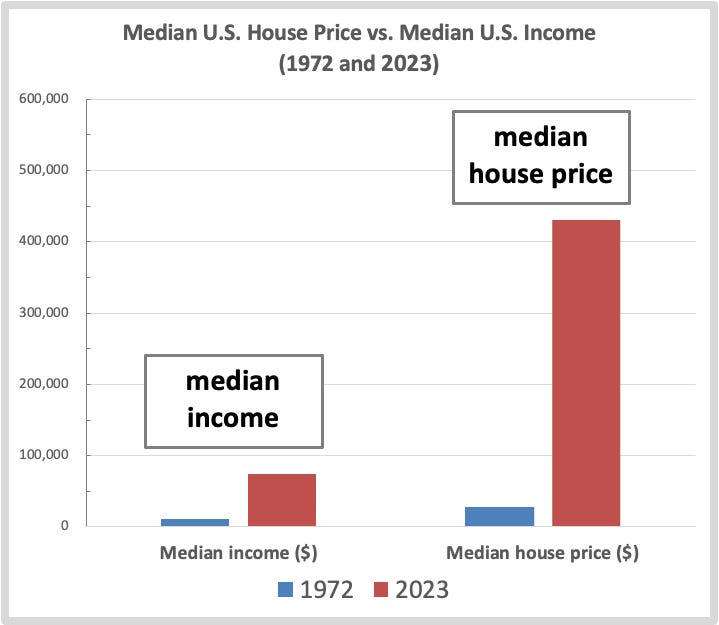

1. Homes have indeed become less affordable in 2023 for younger buyers. Soaring prices and stagnant incomes.

Soaring prices combined with stagnant incomes

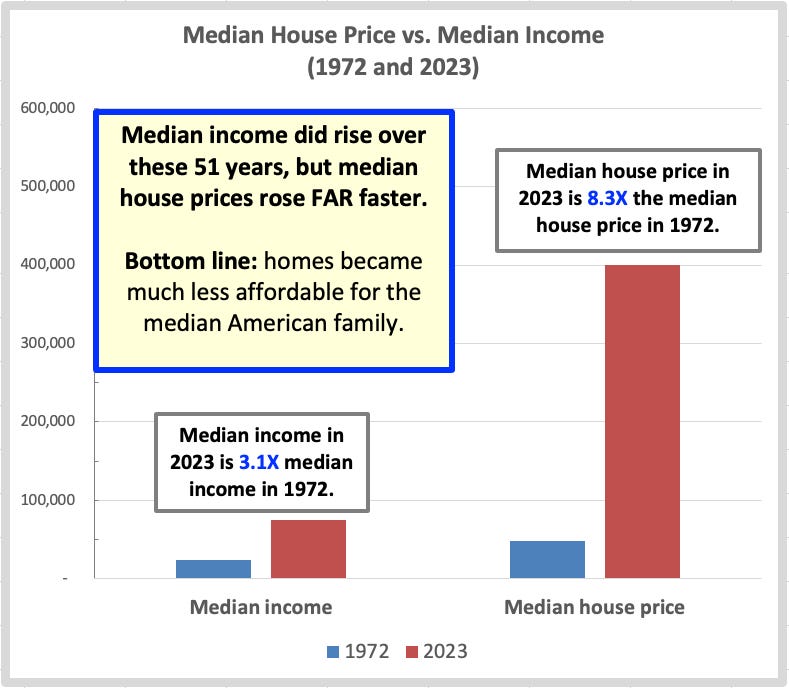

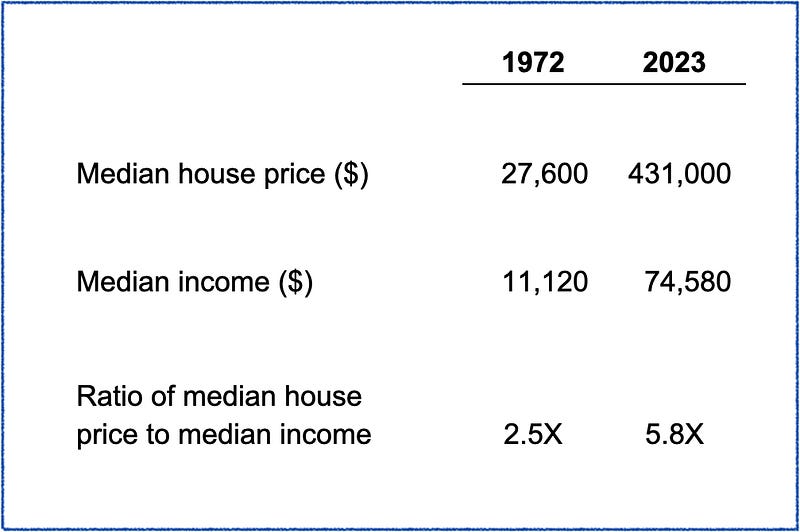

1972 had lower house prices, no question about it.

Prices were lower in the 1970s (1) in absolute terms compared to today, of course, and also lower (2) when compared to median incomes back then.

When we look at U.S. Census data from the early 1970s versus today, “median house prices as a multiple of median income” seem to be about 30–50% less back in the early 1970s than than is today in 2023.

Factoring in median incomes from 1972 and 2023, buying a house today in 2023 is more than twice as expensive as it was in 1972.

So when you bought a house in the early 1970s, it was always a big thing, but you didn’t feel as though you were betting your family’s entire financial future on the house you bought and on the price and terms you got.

Today you often feel as though you are taking something that is literally — not just figuratively — a “bet the house” risk.

2. Everything else is more expensive today — and not just because of inflation over the past 2 years

All of the other big fixed costs for Americans have also gone up dramatically over these 51 years, including healthcare, education, and childcare.

This puts a great deal more financial pressure on families and homeowners.

It also leaves homeowners with far less financial cushion to fall back on if there are emergencies or if someone loses a job.

Healthcare and education costs, for instance, have been going up rapidly and relentlessly since the 1980s.

For instance, in the case of healthcare, not only is your health insurance more expensive in terms of premiums and coverage levels and types, but in addition, actual prices of services and drugs have gone up dramatically. And even with these massive price increases, there is still a huge amount of uncertainty — let’s call it risk — in terms of whether your health insurance company will actually cover your healthcare costs when you need them to. (See “Has U.S. Healthcare Really Become a Mob Protection Racket?”)

Less cushion, more pushin’ on your family finances

So the average American family has far less financial cushion with which to absorb these additional costs and risks. Less financial cushion means that if anything happens to the family’s sources of income, they are much more at risk of losing their homes and potentially having to declare bankruptcy.

Things like “medical bankruptcies” didn’t exist to any significant extent back in the 1970s.

There sure weren’t articles being written — as there are today — about “100 million people in America [being] saddled with medical debt.”

And let’s not even get started about how much more expensive college education is today compared to the 1970s, especially when you normalize it to median incomes.

All of these things — and others — would make it far harder today for the median family in the U.S. to be able to buy a house as their parents and grandparents did.

But when you also add in the fact that “the median house as a multiple of median income” is more than twice as expensive in 2023 as it was in 1972…?

Wow.

The financial burden on the median family today is breathtaking.

3. Intergenerational bidding wars for houses

Younger people — especially Millennials — often find themselves competing against buyers from their parents’ and grandparents’ generations who have the money to make all-cash offers to win bidding wars.

This kind of intergenerational bidding war just wasn’t a thing back in the 70s.

But it sure is a thing today.

See:

- BusinessInsider, April 2023: Boomer homebuying bonanza.

- Fortune, October 2023: Boomer parents are suddenly muscling their kids out of the housing market according to surprising new data from realtors.

- TheHill.com, May 2023: Boomers and millennials fight for homes as housing market cools.

4. Institutional investors buying up entire neighborhoods with cash bids…and pushing prices up even further

And given that the Top 10% in the U.S. own 89% of the stock here in the U.S., it’s very likely that the Boomers who are using cash bids to outbid younger buyers for houses are also going to be benefiting as investors in the private equity funds that are buying up entire neighborhoods as investment vehicles. (See: “HOUSING VULTURES: Will DC Wake Up to Investor Pillaging?”)

5. Having economic and financial wind at your back — 1970s vs. 2020s

We also now know in retrospect that back in the 1970s, the U.S. housing market was just a few years away from a multi-decade massive runup in prices.

This was going to have the effect of making everyone who had bought a house in the 1960s and 1970s look like a financial genius by the 1990s and 2000s.

Now, I can make an argument that housing prices might still run up quite a bit over the next decade or two, but it won’t be a broad market of regular, working class, “middle-two-thirds-of-the-market” folks who will benefit from these potential price rises.

The primary beneficiaries of “the next 10X runup in prices” will instead be (1) the Top 1%; (2) to a lesser extent, the rest of the Top 10%; and (3) institutional investors.

Not being able to count on “asset appreciation” is a big problem for the median homebuyer in 2023.

With prices at such high levels today, particularly with respect to incomes, (1) you have to view buying a house as “an asset purchase” and (2) you have to make the assumption that prices will continue to go up for a long time, so that asset appreciation can make this huge purchase worthwhile for the average family.

It was certainly not the case in the early 1970s that people viewed the purchase of a house as something that only made sense if you got a lot of asset appreciation over the decades.

Back in the 1970s, because house prices were so much less expensive compared to median incomes, it was ok to view your home payments and all the other costs as just an expense…as opposed to a massive investment.

Ask any homeowner. That is not the case today.

Today in 2023, buying the median house feels far more difficult for the median income family, and that is before you factor in mortgage interest rates that are dramatically higher today in late 2023 than they were just 2 or 3 years ago.

I’m still thinking through the ways in which buying a house has changed since the 1970s or 1980s. If you have personal or professional perspectives on this, I welcome your comments on the points above and anything else that would make sense to weave into the discussion.

Thank you for reading, subscribing, clapping, and sharing — I appreciate your time and attention.

Related and recent articles

• 30Y in 30D, Y16: The Total Cost of Ownership of Your House • 30Y in 30D, Y15: Simple Question, Complex Answer — The True Purchase Price of Your Home • 30Y in 30D, Y14: What Kind of People Are Getting Loans for Houses Right Now? • 30Y in 30D, Y13: What Does It Take to Pay Off a 30-Year Mortgage in 15 Years? • 30Y in 30D, Year 12: CBS News’ Version of (Not) Helping You Save on Mortgage Interest • 30Y in 30D, Year 11: Dream Home or Financial Freedom? Rethinking the True Cost of Stretching • 30Y in 30D • Year 10: A Tale of Two Eras — Home Buying in 1972 and 2023 • 30Y in 30D • Year 9: Visualizing Savings — Mortgage Charts that Matter • 30Y in 30D • Year 8: The Mechanics of Mortgage Interest — What Really Matters • 30Y in 30D • Year 7: The Big Payoff of Early Extra Payments • 30Y in 30D • Year 6: Mortgage Power Play with a Single $100 Extra Payment • 30Y in 30D • Year 5: Are Car Buyers Smarter than Homebuyers? • 30Y in 30D • Year 4: Accelerate Payoff Via Extra Monthly Payments • 30Y in 30D • Year 3: Early Extra Payments Are Magical • 30Y in 30D • Year 2: Rapid Progress on the 30-Year Mortgage •30Y in 30D • Year 1: Starting Strong on the Mortgage Journey • Kickstarting “30 Years in 30 Days” — Decades of Mortgage Wisdom in 1 Month • A Friend Texted to Ask “Who I Favored” for 2024 but Hated My Answer • Has U.S. Healthcare Really Become a Mob Protection Racket?

(Subscribe to receive email notifications when I post new articles in this series and on other topics.)