25 Insider Tips for Winning Your First Round of Venture Capital — Part I (Simpsons Themed)

Picture this: 10 minutes after you’ve finished pitching your startup to the world’s most prestigious VC fund, your phone rings. It’s the head of the fund — let’s call him Montgomery R. Burns. Here’s what he says:

“My partners and I love your vision, and we’d like to lead a $5M seed round in your company.”

You’re not surprised.

It’s the third call like this you’ve had in the past week!

If this sounds like an outcome you want to achieve — multiple offers to fund your nascent startup — then I’d like to help you.

Some groundwork before we get into the 25 insider tips…

Who am I?

I’m a 3x co-founder, currently running Knowable, an audio-first learning platform, and am fortunate to have raised over $12M from some of the world’s best investors — including Andreesen Horowitz, First Round Capital, Initialized Capital, Upfront Ventures, SV Angel, Mucker, and others.

In this post I’ll share 25 tips about raising capital from VC’s that I wish I had known when I was starting out. These tips aren’t exhaustive, and they’re not right for everyone. I strongly encourage you to explore other sources, including the ones linked at the end of this post.

Also, I’m a fan of The Simpsons — particularly season 8 — hence the references.

Who’s this for?

If you’re interested in raising venture capital for your startup, then I’m guessing you’re something like Lisa Simpson: curious, resilient, and optimistic enough to believe that you can change the world for the better.

And, if you’re reading this post, then you’re likely a first-time founder, which means that you’re at a structural disadvantage when raising funds from professional investors (see tip #13).

Is your start-up VC-backable?

A key difference between a business that’s “venture-backable” and a traditional business is that the former has the potential to be highly scalable in a large market. An example of a scalable business: AirBnB.

AirBnB was able to grow to a $100B+ value primarily by providing software that connects hosts and travelers.

A less scalable, more traditional business approach would have been to launch a chain of owned-and-operated bed and breakfasts, which would be far more capital intensive, and therefore less scalable.

There’s nothing wrong with the latter, and many brick-and-mortar businesses, like Blue Bottle Coffee, can attract venture funding, but, on average, most venture investors prefer asset-light businesses over capital-intensive businesses. Of course, there are outliers that challenge this convention; looking at you Tesla and SpaceX.

Why raise from VC’s?

Why bother with trying to raise venture dollars?

Some reasons:

- High-growth startups need cash to fuel growth. Some of the most valuable businesses today started out by burning vast sums of capital. E.g. Facebook, Google, Pinterest, Amazon, AirBnB, etc.

- Cash in the bank is a competitive advantage. You’ll be able to move faster and iterate more quickly than your bootstrapped competitors.

- You can pay yourself a modest salary before your business is profitable. Note: I was making $300k per year in finance and subsequently paid myself $80k per year as CEO after my seed round. Founders typically pay themselves below their market rate because they have a vested interest in preserving company cash. Also, heads up: investors have a say in how much you pay yourself, so you should discuss your salary before you sign a term sheet.

- Some venture investors are truly value-add. In my experience, the most consistently value-add investors are the ones that have previous operating experience. They’ve worn the founder swag, and can therefore better empathize, and better anticipate, where they can be maximally helpful.

- Having a brand-name investor on your cap table gives you more credibility with potential teammates, the press, and partners.

If you can achieve your business goals without selling equity, then by all means, don’t raise from venture capitalists. Stop reading this post and get back to running your product.

Otherwise, let’s continue…

Insider tip #26 — Work backwards from where you want to be

Let’s assume you’re working on a scalable business idea — perhaps it’s a blockchain-based social network for climate activists — and jump to where you want to get after applying all the great 25 tips in this series: receiving multiple term sheets from top-tier investors in quick succession (a one to two week window is ideal).

Note: a term sheet has all the terms outlining a lead investor’s terms for financing. It seems like it should be called a “terms” sheet, because there’s more than one term, but it’s not. 🤷♂️

Rewind to 30 minutes before the aforementioned investor call / meeting: you deliver a perfect pitch to that hot VC fund, um, let’s call it Burns Capital, based in Springfield. You answer some follow up questions, thank everyone for their interest, and shortly thereafter get the call from your sponsoring partner (Monty) with an offer to lead the funding round for your fledgling startup. “The term sheet is on its way,” he says, hopeful that you like his firm as much as he likes your company.

The very best thing you can do to ensure this outcome is to have demonstrated a strong fit between what your company offers — your product — and a sufficiently large base of customers — your market. The insider startup term for this magical meeting of supply and demand: product-market fit, or PMF.

When you have PMF, you have a scalable product that has accelerating traction in a sufficiently large market. More than raising venture capital, obtaining product market fit is what you should be working toward most.

Put another way: getting multiple term sheets isn’t the end goal; finding product market fit is. If you have product market fit, investors will likely come to you, rather than vice versa, and successfully raising venture capital will be way easier than it would be otherwise.

But, many founders need to, and are able to, raise their first round of venture capital through an outbound process even before achieving PMF. That’s because startups often require capital to achieve product market fit.

TLDR: the sooner you can achieve product fit, the better. But, many startups need to raise capital before achieving product market fit. So, while building a successful business is your ultimate goal, raising capital is often a necessary step in the direction of that outcome.

Don’t confuse the means (capital) with the end (solving problems at scale); many founders do.

Fundraising is an arduous process

While understanding your end goal and working backwards will certainly help you end up in the right place, there’s still 6.75 more truckloads of work ahead of you.

There’s no shortage of advice on the internet about how to raise venture capital. A lot of it is from VC’s, and a lot of their advice is good. I’ve linked to some of the best resources at the end of this post.

But, in my experience, the best advice comes from other founders who have recently gone through the process of fundraising. Seek out the people who are one or two steps ahead of you and try to learn from them (see tip #5).

All of them will probably agree on one thing: raising capital is usually a stressful and arduous task. You’ll have to sift through often contradictory advice, including annoying posts like “25 Insider Tips For Winning Your First Round of Venture Capital” all while running your business and trying to stay ahead of your competition and that nagging mom-like voice inside your head that says “maybe you should pursue a more traditional job.”

But most will also agree that the journey is worth it, regardless of the outcome.

Alright, enough preamble. Grab your coffee, and let’s dive into the 25 tips for getting your startup funded…

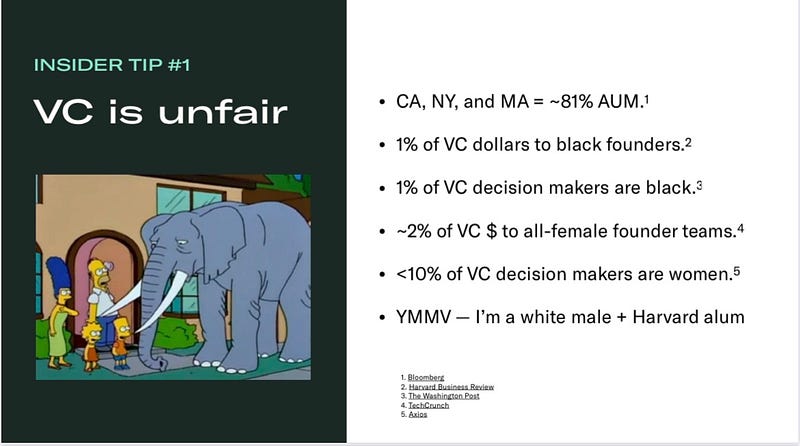

Insider tip #1 — VC is unfair

Venture capital is primarily dominated by white male investors who fund primarily white male founders. It’s not fair, and it’s not optimal for our economy, or our society, but it is unfortunately the current reality.

And, to call out the elephant in this post: I’m a white male and therefore had an easier time raising capital than I would have if I wasn’t.

That is to say: what worked for me might not work for you. I’m sharing these tips so that whatever your background, you better understand the game on the field.

Also, regardless of your background, you’ll likely find fundraising confusing and often arbitrary. “How in the world did that company raise so much money pre-launch?!” is a question that nearly every founder asks themselves at some point in their career.

Understanding the peculiar logic of venture capital investors will lessen your confusion and increase your odds of success. I.e., let’s move to insider tip #2…

Insider tip #2 — Know your customer

When you’re raising funds for your business, you’re a salesperson. I’m going to say this again, because few founders like to think of themselves as a salesperson, but it’s true, even if investors are soliciting you.

You.

Are.

A.

Salesperson.

You’re selling equity (ownership) in your business in exchange for cash to fund your business and maybe some additional benefits (advice, network support, stamp of approval).

Nuance: you want to get to a position where investors are selling you on why you should let them invest. That’s why your “working backwards” goal is both product market fit, and multiple term sheets.

Investors are in the business of buying equity, and therefore, if you’re raising capital, you’re in the business of selling equity. The best salespeople understand the needs and psychology of their counterparts, and they craft their pitch accordingly.

So, what are the needs and psychology of VC’s? Like all investors, VC’s seek to maximize returns while minimizing risks. And in particular, because of the way that most VC funds are structured, VC’s are looking for investments that have the potential to “return their fund.”

A good rule of thumb: if your business doesn’t have a plausible chance of becoming a billion dollar business, a “unicorn” in VC speak, then it’s probably not a great candidate for VC funding. If you want to understand why, I recommend Scott Kupor’s book: The Secrets of Sandhill Road.

For now, trust me: asking for $5M of capital so that you can sell your business in 5 years for $20M makes you an automatic “no” for sophisticated venture investors. It might be a good outcome for you personally, but it’s not a great outcome for your venture partner.

So, if you’re not pitching a business that has the potential to scale, in a market that’s worth, or may soon be worth, more than one billion dollars, you’re probably not a good fit for venture financing.

Nothing motivates an investor as much as 1) “greed” and 2) “fear.” Investors are paid to be greedy on behalf of their investors (LP’s), and they fear publicly missing out on a great investment (because they’ll have a harder time raising their next round of funding).

Of course, there are other motivations for investors, e.g. a desire to have a positive impact on the world, but the aforementioned two are typically the most powerful motivations to be aware of when trying to elicit a term sheet.

So, if an investor learns that 1) she’s your only funding option, and 2) your business doesn’t have significant upside potential, then you’re unlikely to get a compelling offer anytime soon.

In summary: share a compelling vision of the not-too-distant future in which your company is worth more than $1B (appeal to greed), and talk with many investors at the same time (stoke fear).

Insider tip #3 — Focus on the fundamentals

I’m belaboring this point because a lot of first-time founders confuse the means (raising capital through an irrevocable sale of equity) with the end (building a sustainable and scalable business).

The better your metrics and fundamentals — market, team, product traction — the more de-risked your company is, and the more attractive you’ll be to venture investors.

Remember from tip #2: investors want to maximize reward and minimize risk. That’s their entire job. Ironically, the less you need investors, the more they want you. It’s the Groucho Marx saying applied to VCs: investors don’t want to invest in companies that want them as investors. Well, they do, but, you know what I mean.

So, before you worry about rehearsing your pitch, first worry about de-risking — for yourself and your investors — by improving your fundamentals. This is easier said than done.

In the screenshot above I list out some tips for raising your first round of capital. Legendary founder and investor Paul Graham — read his essays (linked below) if you haven’t already — replied to the tweet with some additional thoughts.

In my opinion, both of us have good points. I agree with Paul that you want to put yourself in a position where you don’t need to raise external capital, but I also think that when you do decide to raise capital, you should maximize your chances of finding the best partner possible, and on the best terms possible that will set up you and your company for long-term success.

That means that having good fundamentals isn’t all you need to worry about.

I.e. listen to both Paul and me, and keep reading…

Insider tip #4 — Unicorns are hard to spot

We’ve established in tip #2 that investors want to invest in unicorns — or rather, companies that have a relatively high probability of becoming unicorns — but it’s really hard to know which early startups will scale, and which will fail. Even the best investors miss opportunities, and any serial venture investor has “failures” in her portfolio.

As an example, numerous famous investors famously passed on investing in both AirBnB and Uber. It’s hard to know at the onset which businesses are unicorns-to-be, and which are goats with ice cream cones glued to their foreheads.

Your job as a venture-backable founder is to maximize the chances of your company’s success. And a key part of this job is making sure you have the best funding and the best resources possible to achieve your mission.

I.e. you don’t have to killer metrics to raise your first round of funding or be accepted into an accelerator. Your first round of funding is often to help you prove that you can find product market fit. If you already have it? Amazing, this process will be way easier for you. If not, you can de-risk in other areas and hopefully still get that first bit of capital to iterate your way to further traction.

To be clear: you should never lie, but you also shouldn’t assume that just because your company isn’t an obvious unicorn today doesn’t mean that it can’t become one over the next several years.

All unicorns start as a fantasy of the future. Some turn into a reality; most do not.

Insider tip #5 — Make founder friends

The best time to build your network was 20 years ago. The second best time to build your network? 19 years ago. But, today is a good time too! Be helpful to other entrepreneurs today. It’s an investment in them, and in yourself.

I was fortunate to have made founder friends by going through an accelerator program (Mucker), and to this day the other founders who were in my cohort are among my closest friends and most valuable advisors.

I’m a big proponent of accelerators for first-time founders. Y-Combinator, Techstars, and Mucker all have great programs. There are other good ones too — OnDeck is new, but seems promising — but there are also predatory accelerators / “investors” that take advantage of first-time founder naïveté, so do your diligence (see tip #22 for more). Spoiler alert: just because Montgomery Burns seems like a nice enough guy, doesn’t mean he is.

Here are some ways that having founder friends helps:

- The best intros to investors come from other known, successful founders.

- The most honest references come from founders who already know and trust you.

- Other founders are the ones you’ll go to to benchmark, and to normalize the challenges you’ll inevitably face. E.g. how much are you paying yourself as CEO? How are you managing stress around fundraising? Etc.

- Helping other founders is a way for you to remember that even if things at your company aren’t going great, you’re still a valuable member of society. Note: every founder I know conflates their self-worth with the anticipated worth of their company. (See tip #21)

And here are some tips for making friends with other founders:

- Be helpful. Proactively find ways to help.

- Give before you ask.

- Check in regularly. Especially when you don’t need anything.

Many first-time founders attempt to build connections with founders who are already successful. But, the most meaningful relationships for any founder are established prior to success. I.e., think like an investor, and invest your social capital in people you admire before they become unicorns. Or, put another way: play the long game and start investing in your relationships today.

“Sure Warren, that’s all fine, but what if I have a hot startup idea today but no founder friends?” Here’s my advice:

- Apply for accelerators. It’s the best way to make founder friends, and if you’re admitted to a top accelerator, the equity you give up will be well worth the relationships you’ll build.

- Follow and engage with founders you admire on Twitter. Comment thoughtfully on their posts and publicly share your suggestions for improving their product. Founders like helping other founders, especially ones that are helpful to them.

- Build a kick-ass product. Easier said than done. But true. If you have a great product that people love, you’ll be less reliant on networking as a conduit to capital. And nothing eases the entrepreneur’s journey like constant growth.

Insider tip #6 — Don’t hire Lionel Hutz

Just as there’s a quality spectrum for investors, there’s a similar spectrum for lawyers. If you need to hire a lawyer — you probably don’t in the early days (see Stripe Atlas) — try and find one that specializes in startups.

Also, if your startup seems promising, some law firms will waive or defer their fees for you in the early days in order to win your business. Warm intros from other entrepreneurs will help in this regard.

If you’re serious about building a successful company, and you feel the need to consult a lawyer, then don’t assume that your mom’s friend’s divorce attorney has the right answer for you.

Quick note: I’m not a lawyer, and this isn’t legal advice (I think I’m required to say this disclaimer?), but there’s one very important item that you’ll want to be aware of when you form your company: file an 83(b) election within 30 days of issuing yourself shares. Trust me.

Insider tip #7 — Don’t f-up your cap table

The summary of who owns how many shares at your company is called a capitalization table (or “cap table” in startup speak). Your cap table is extremely important to you, your employees, and your investors.

Anytime you issue someone shares, or options to buy shares at a later date, you dilute your ownership stake. The more shares you sell or grant to others, the lower your ownership percentage.

So, don’t give shares to people who won’t help you grow the overall enterprise of your business.

You and your teammates should vest your shares over time (typically 4 years). This means that if your 50–50 co-founder quits after the first week, he doesn’t still walk off with 50% of your company.

Investors want founders to be maximally motivated to increase enterprise value, so they want to see the go-forward founder(s) and key teammates owning a meaningful amount of the equity.

I.e., if you issued 30% of your shares to Lionel Hutz for the bad legal advice he gave you last summer, that’s 1) not a great reflection on your judgment, and 2) “deadweight” on your cap table that will diminish your chances of attracting outside investors.

End of Part I / Ask

That’s the end of part I of this post.

If you’ve gotten any value so far, please follow me on Medium, and share this post with other aspiring founders (see tip #3).

I’ll be publishing tips 8 through 25 soon. Update: here’s part 2.

Additional resources:

A fundraising survival guide | Paul Graham

How to raise money | Paul Graham

A guide to seed fundraising | Y Combinator

How to raise money from a venture investor | Andreesen Horowitz

Fundraising advice to avoid | Andreesen Horowitz

The fundraising wisdom that helped our founders raise $18B in follow-on capital | First Round Review

What’s the first thing you need to do before fundraising? | Mark Suster

Step-by-step fundraising tactics from the NYC legend who raised $750M | First Round Review

Series A, B, C funding: How it works | Investopedia

What is the difference between “friends and family”, seed and Series A financings? | Cooley GO

VC: An American History | Tom Nicholas

Secrets of Sand Hill Road | Scott Kupor

Pitches

How to understand and choose a venture investor | Andreesen Horowitz

The a16z Pitch Room: Sandbox VR | Andreesen Horowitz

How to pitch investors | Michael Seibel

How to present to investors | Sequoia Capital

What should you send a VC before your meeting? | Mark Suster

Pitching your early-stage startup | Stripe Atlas

First-time founders: How to pitch your startup to investors | Mike Raab

Take your fundraising pitch from mediocre to memorable with these storytelling tips | First Round Review

Pitch resources

Sequoia Capital (Pitch Deck Template) — The industry-standard template for startup pitch decks.

DocSend — Track opens, make dynamic edits, and manage access to your deck. I use DocSend for every fundraise and love it.

Startup Pitch Decks — A curated set of fundraising decks from some of the world’s most successful companies.

Venture deals

The economics of term sheets | Andreesen Horowitz

Term sheet negotiation: How to avoid common mistakes | Atrium

Negotiating term sheets: Focus on what’s important | Cooley GO

How startup options (and ownership) work | Andreesen Horowitz

A standard and clean Series A term sheet | Y Combinator

Podcasts

The Twenty Minute VC — Interviews with a who’s who of venture players.

a16z Podcast — In-house podcast from top venture firm Andreessen Horowitz.

This Week in Startups Podcast — Prolific venture investor (and former founder and reporter) Jason Calcanis interviews leaders from across the tech landscape.

Audio courses

Launch a Startup on Knowable — Reddit-co founder, Alexis Ohanian, leads a 6 hour audio course on best practices for launching a successful startup.

Garry Tan lessons on Knowable — Entrepreneur-turned-investor Garry Tan shares his tips and insights on building venture-backed businesses.

Final ask / goodbye for now

If you have any comments or questions, please put them in the comments below and I’ll do my best to respond!

And a friendly reminder to lovingly tap that follow button so that you can get the subsequent tips as soon as they’re published. 🙏