How a novice trader made 25% despite a market crash

An honest look at 6 trading strategies I tried, and how I turned deep losses into a 25% profit in my first year

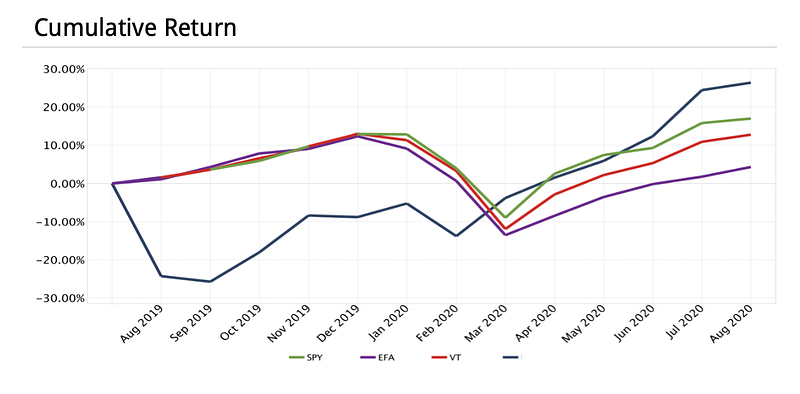

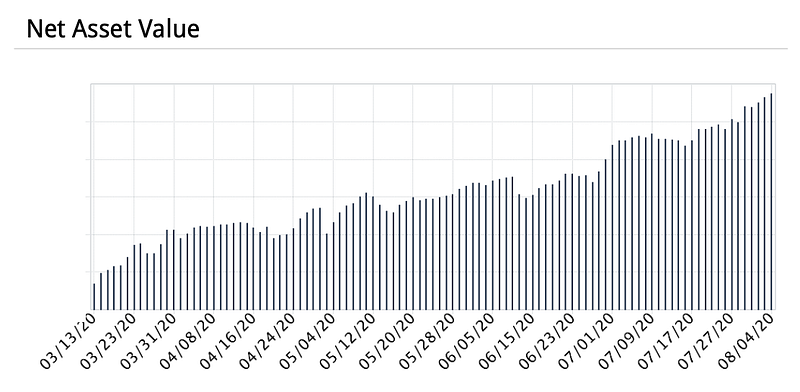

I just reached the 1-year milestone on my trading account with a 25% annual return — all of which was made after the COVID-19 stock market crash in February 2020.

This is a walkthrough of my first year of active trading, detailing my psychology, tactics used (both failed and successful) and lessons learnt. I’m here to unabashedly show you all the dumb mistakes I made and how I paid for them, because that’s the reality of trading.

Note: this is an intermediate-level article on trading. For investing and trading basics, feel free to read this guide I wrote below.

I’m not an expert. I’m fortunate to have an undergraduate finance education, but I’m not armed with any form of sophistication unattainable by a monkey with a typewriter and Investopedia.

I’m not a guru. I don’t have the predictive powers privy to Twitter stock psychics and guys with doomsday bunkers, and I’m not going to peddle Tesla stock or gold coins to you.

I started trading because I want to one day be financially independent, and because I seem to have a thing for money. Unthinkable, I know. Despite the unattractive return on investment for writing, I’m doing so because:

- More people are starting to trade/invest during the pandemic

- Losing money is far easier than making it, and…

- I, for one, had no idea what I was doing going in.

Stocks, and investments in general, are brilliant. Mashed together in a price chart are all the elements of a Sherlock Holmes mystery and a Golovkin title fight, plus the potential to actually make profits. If I get you excited about making 25%, great, but I hope I also encourage you to become a more thoughtful and sustainable trader, instead of trying to be an overnight boy wonder.

If you’re curious: I use Interactive Brokers because their Trader Workstation is pretty powerful, even though their administrative capabilities leave much to be desired. Most large brokers are just fine, but personally I stay away from Robinhood because I believe gamification is counterproductive to the analysis and pain involved in active trading.

Let’s jump in.

1) Overconfidence and utter failure (-33%)

I began my active trading journey overconfident, and I say so because:

- I thought I knew enough to not lose money

- I started trading live (i.e. not with a simulated paper account) immediately*

*There’s actually nothing wrong with starting with real money, as long as you understand you’ll be losing some of it. Having skin in the game feels completely different from a simulation and may change your trading behavior; plus, if you’re like me, you may learn better with hands-on experience.

I can explain. You see, I’m a finance major, I’ve done equity research, I’m not one to believe in shady ads for stock picks, I always stay hydrated, my ring finger is longer than my index finger, etc.

I’d like to think my confidence was justified, but overconfidence seems to be a defect endemic to all amateurs. We all think we know enough, but we don’t. Not even close. Before I put on any positions, I had read up on what stocks are, fundamental analysis, and technical analysis. Hope this isn’t a spoiler, but that’s not nearly enough — what will keep you from losing is consistent edge and risk management, both of which come with experience.

Wall St continues to thrive because no one has solved the market. It’s a complex and confounding beast, whom the idea of taming continues to seduce and subdue hedge funds and asset managers.

My first trading approach: buying stocks right before earnings, hoping for prices to spike up.

Stocks I tried include UBER, AMZN, JNJ, BRK, M. This was a massive failure. Trading earnings is viable because volatility is elevated around earnings dates, increasing the probability of both outsized returns and losses. But, to be successful at trading earnings you need:

- High probability of earnings going in your favor AND the stock behaving as expected (meaning you need a deep understanding of what drives the company’s earnings and stock, and macro conditions in its industry)

- Good risk/reward ratio (meaning you’ll make more if you’re right than lose if you’re wrong, typically happens when you think the company’s earnings will deviate significantly from analyst estimates)

- Or, make use of the elevated vol to trade technicals.

I just went with my gut, so I lost on about 60–70% of my trades.

My second approach: intraday trading using RSI, support/resistance levels, Ichimoku Cloud, and Level II.

This was also a crapshoot (for me). Things I didn’t know and had to learn about technical indicators:

- Each is designed for a very specific purpose, and is not a standalone holy grail. E.g. RSI is a momentum indicator that tells you if something’s overbought or oversold based on average price movements over the last 14 periods. It says nothing about volume and trends, only helps if you assume the stock will stay in a certain price range, and uses arbitrary levels — many stocks happily stay overbought/sold for weeks.

- They’re purely proxies. They manipulate price and volume to attempt at estimating trends and momentum, and you’d be hard-pressed to find one that gets it right more than 50% of the time.

- As a result of their imperfection, traders must know the indicators they use intimately, especially how they’re calculated and where their shortfalls are.

I lost on about 70% of my trades. Now, the best trend-following traders may have a similar win percentage, but they minimize the losers and maximize the winners.

If you want to be successful at technical trading (and you can be), learn proper risk management, use several indicators in conjunction, and know everything about them.

Main takeaways:

- There’s no sure or easy thing, even if online gurus want you to believe it so that you’ll pay them.

- Everyone going into trading thinks they know more than they do.

- Start with real money if you want, but know that you’ll lose some.

2) Exploration and complacency (+11%)

After early failures and a steep downwards equity curve, I reluctantly gave up on trying to find an easy, quick and guaranteed trading method.

By this point, I had cut a third off my initial account value, and had to stomach the humiliation of refilling my account. So, I started exploring more traditional and passive approaches.

My third approach: Semi-passive, fundamental stock picking.

I used IB Trader Workstation’s lesser-known Portfolio Builder which automatically ranks, picks and buys/sells stocks based on rules such as P/E, earnings growth, market cap, etc. I say semi-passive, because these portfolios get rebalanced regularly so it’s not quite buy-and-hold, and I actively design the rules and shift allocation between several portfolios.

Instead of trying to shoot for the moon, I reined in expectations and aimed just to outperform the S&P, while diversifying my investments. This meant investing in various industries and putting some capital in bond ETFs like TLT and LQD. This strategy worked decently and I’m still maintaining it to this day, but some warnings:

- Fundamentals and prices are often divorced in the short term — your portfolio can have the best companies but still lose money for weeks. If you play fundamentals, go long.

- Don’t fall in love with one stock. Too much exposure to one company or holding it too long can cause more damage than it’s worth — keep stops in place and stick to them.

- Bonds add diversity, but when push comes to shove, correlations between asset classes increase and burn a hole in your portfolio anyway. More on that later.

- Past performance is not a crystal ball. The Builder in IB TWS has a backtesting function — I obviously only used systems that backtested well, but I tried to avoid relying on the backtests. The Builder is also something of a black box. You pick the rules, but you don’t see the exact impact of each choice and could fall into the trap of over-optimizing a system to the point it’ll never work in real life.

I was mostly able to outperform the index slightly, and would recommend any new investor/trader to start with a similar approach. Conduct some simple research, do a little long-short stock picking, stay diversified and keep your sights set on longer-term investments.

It might be counter-intuitive, but in the markets the difficulty level generally increases as your investment time horizon decreases. Time drowns out noise and highlights the investments that are truly high-quality.

My account having recovered a little, I tried my hand at options. Here, my finance degree gave me a leg up because I didn’t have to relearn options basics.

My fourth approach: buying butterflies.

This is a strategy with limited loss, that profits if the stock price stays within a range (if held till expiration) or if volatility decreases (before expiration). I started by buying low-risk butterflies on large cap low-beta stocks, before gradually dialling up the risk (by adjusting strikes) and shifting into higher beta stocks.

I was mildly successful because generally, the markets are less volatile than implied by options in normal times. A few crucial things I learned:

- Don’t try this in turbulent markets if you’re just starting out. Butterflies are non-directional (i.e. no difference if stock moves up or down), but short volatility. Losses are limited if you hold to expiration — before that, vol spikes could burn your account more quickly and severely than you’d expect.

- Beware of assignment risk. Butterflies involve selling an in-the-money leg, so if the stock gaps there’s a chance the option holder will exercise it, and you’ll suddenly end up long or short 100 shares. At best it’ll jack up your margin, at worst it’ll slash a chunk off your account while you’re trying to unwind your entire position. Trust me, I know.

- It’s better to buy butterflies when you expect volatility to decrease than when you just think price will end up in a certain range. The win probability is higher, and you’ll realize gains much faster than waiting till expiration.

Overall this was a rather smooth-sailing period, but that got me a little complacent. I ended up with too much exposure to high-beta tech stocks, which came back to bite me in the Feb crash. That said, even if no crash happened, staying well-diversified in a buy-and-hold strategy is a must.

Main takeaways:

- Buy-and-hold (smartly) is better than buy-and-hope

- Refer to past performance, but don’t take it out to dinner and marry it

- Trade options only when you’re ready to swallow 100x your current losses

3) Panic and uncertainty (-15%)

I had almost recovered all my losses when we ushered in the dawn of a new decade. The gentle golden sun rose over sweeping hills, incinerating the faraway spectre of US-China tensions and the disembodied whispers of ‘the market is due for a correction’.

The best part is, I got worried about COVID spreading to the US, so I bought a bear put spread on the SPY a week before the crash. Market started declining, I decided I’m a genius and proceeded to take the hedge off way too early.

The market crash erased 15% of my account in a week. Doesn’t sound like a lot, but I had pumped much more money into it since my early days, so the dollar amount I shed was much bigger, much faster and much less due to my own stupidity than I had ever expected. If you weren’t invested through the crash, I’d bet that losing 15% feels worse than you’d imagine, especially if there’s nothing you can do about it.

‘Nothing you can do’ isn’t entirely true, though. I lost 15% and not 35% like the broader market because I cut 70–80% of all my positions immediately. Bonds and stocks had become positively correlated as the markets sold everything to get back in cash, and none of my Portfolio Builder backtests had ever covered this extent of market turmoil, so I felt like I had no choice.

Looking back, there are two things I’d like to point out to novices like myself.

Main takeaways

- Stay invested, if you’re willing to see it get worse before it gets better. It’s said that retail investors are a great contrary indicator — by the time we pile in or out of something, it’s usually too late. History shows we’re not very good at timing the market, so in crash scenarios you have two choices. Either you have a long term investment horizon and should just strap in for the ride, or you should get the hell out yesterday. In the last decade, time in the market was more important than market timing. There were short bursts of high return that if you missed, you’d have lost most of the profits stocks enjoyed, so instead of timing your shots you should just stay in the game. While this regime might be changing (topic for another day), ‘stay invested’ is still good advice for the amateur.

- Have a crisis plan for what to buy and sell. The best money managers know that crises are more like Black Friday sales — the indiscriminate selling creates opportunities to get amazing investments on the cheap (cue Buffett). Think tech stocks that benefit from the crisis, or investment grade bonds. Even in tranquil times, prepare a plan for what positions you’d buy on the cheap when a crisis happens, like keeping a shopping list for BF except you don’t know when BF will be. I didn’t, and missed out on a wonderful opportunity to load up on high quality, long term holdings. Your plan should also include what existing positions to get rid of, to free up dry powder for shopping.

4) Research, reset and recovery (+35%)

I took a break from trading after the crash, leaving a small portion of my account invested in safe stocks and keeping everything else in cash.

During those weeks I did some research and tried to formulate the best strategy to recover my account. Right before the crash I had just recovered everything I lost when I started out, only to watch the painstaking gains (and more) evaporate again.

If you ever find yourself in the same situation (and you will, if you do this long enough), just remember hindsight is 20/20. Don’t beat yourself up over what you didn’t do. How could I have missed going long on NFLX and ZM and short on airlines and hotels? How could I have not noticed IG bonds trading at such a massive discount? How could I have missed the 2-for-1 day at Starbucks?

If it has come and gone, forget it. I missed the lowest point in the stock market and started putting my longer term positions back on on the way up. In the meantime, I initiated a new strategy that saved my account.

My fifth approach: Selling delta-hedged puts.

I sold far out-of-the-money put options on a few stocks I either believed will not fall far (thus the options expire worthless) or wouldn’t mind being assigned if they did crash. For example, I sold some $150 strike puts on TSLA; if it doesn’t crash to $150, I keep the premium. If it does, I get 100 shares of TSLA at a cheap $150. Typically these extreme options will be worth nothing, but due to the elevated volatility their premiums became significant. I kept these positions delta-hedged for the first weeks, which really weighed on my margins but let me sleep better at night.

In every success story is an element of serendipity. I didn’t come up with this strategy on my own — I read about it on SeekingAlpha, researched the risks and adapted it for myself. Also, if there had been an immediate and equally devastating second crash after March, I’d have lost abysmally with this play.

In the month following late March, I gradually put on more of these positions, trying to keep them spread out (TSLA, BA, ZM, NFLX, C, etc.). The delta hedges and diversification helped reduce day-to-day fluctuations, though of course there were still rough patches. That one time Musk tweeted that TSLA’s ‘too high’ gave me February crash flashbacks. If you sell vol, you’d better know you’re in for a ride.

Since then, I’ve adapted this tactic to be used opportunistically on stocks where news events create volatility that I think is overblown. Instead of just using short puts, I’ve also been using more butterflies and iron condors (reduces risk and margin). Eventually, using this tactic effectively brought my account back up to about +15%.

My sixth approach: Macro bets and diversification.

Studying macroeconomics and reading commentary on Financial Times and WSJ helped me add another dimension to my trading. Macro is something I think is underrated amongst retail investors/traders; I personally avoided it previously because I thought it was too complex — to some degree that’s valid, but a basic understanding of macro is still extremely helpful, even if you don’t trade on it. It’s just like how technical traders advocate looking at a higher timeframe (e.g. hourly bars) than what you trade (e.g. 15-min bars) because it gives you a sense of which way the wind’s blowing.

In late June, given the ultra-supportive Fed, weak US virus response relative to China and Europe, European joint debt issuance, weakening dollar and recovering inflation expectations, I entered separate trades on long Chinese consumer ETF, long gold and long EUR (against the dollar). These expressed my macro views and also helped me diversify my portfolio further, making me less susceptible to US market problems. Long story short, they’ve been paying off well and augmenting my returns, bringing me to the +25% today.

Main takeaways

- Forget about the shots not taken

- Read widely and always be open to improve your approach

The final word

Trading is the best sport in the world. But like a sport, amateurs pay to play, and pros get paid to play. Problem is, there isn’t a ‘right way’ to do things, nor a coach that will tell you exactly what to do.

Making money is far harder than losing it, and anyone who says otherwise just wants you to buy a course. I’ve only been trading for a little while and barely finding my own footing, but I’d be glad if my experience helps you to achieve +25%, without getting burned -33% like I did.

Study hard, find your method and stay inside your risk tolerance. All the best on your journey.

Gain Access to Expert View — Subscribe to DDI Intel