12月聯儲局FOMC原文及經濟預測+記者會全分析|市場高興得太早?高通脹未受控,最快明年尾才有望減息?

戰績回顧: (一) 11月3日文章提到可開始分段吸納VOO(一隻S&P500 ETF,可說是更低管理費版的SPY),當日收市價是340.83,12月14日收市價是367.16,個半月升幅7.7%;(二) 5月開始連出幾篇文看淡港樓,至今CCL已由當時的180.97跌至12月9日的157.67,跌幅12.9%。以上預測準確,總算對得住讀者。

TLDR: 聯儲局12月14日把fed fund rate(FFR)加到4.5%。市場近期因CPI稍為回落且低於預期很高興,但Jay Powell在記者會上就潑了冷水。FOMC statement和上月一樣搬字過紙,重申dual mandate,通脹高企而就業數據好,就有需要有條件加息。FOMC經濟預測上調了明年Core PCE inflation和失業率預測,明年高通脹仍在,但加息條件卻減少了。結合FOMC經濟預測及CME利率期貨市場聰明錢去看,估計FFR明年大部分時間都在5%以上,到明年Q4才有機會掉頭減息。但,實際幾時掉頭減息,可能連FED官員自己也不知道,只能繼續緊貼最新數據去估。

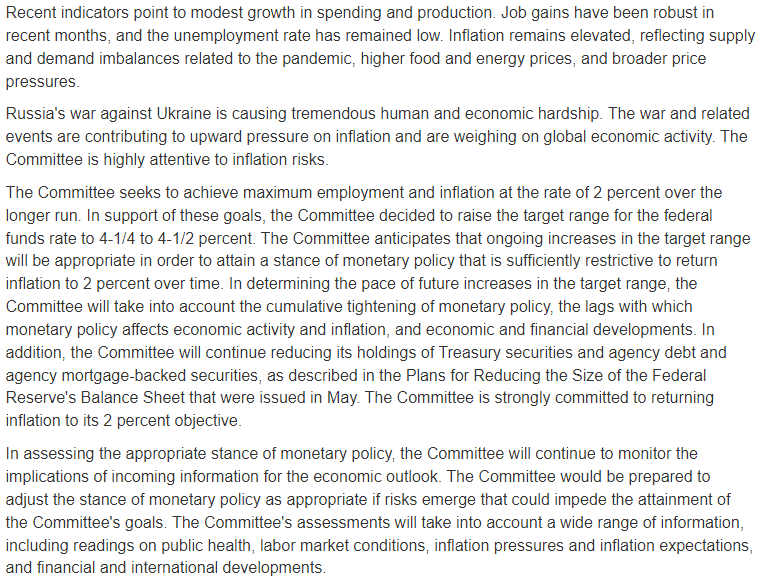

(1) FOMC statement:

註:搬字過紙,立場不變?

- 再次重申dual mandate — 調控失業率和通脹率,為此決定加息0.5厘,FFR升至4.5%。

- Unemployment remained low — 美國11月失業率3.7%,同10月持平,符合市場預期,繼續低於長期平均值NAIRU的~5%。11月非農就業人數亦不錯,新增26.3萬,稍高於上期的26.1萬,亦高於市場預期的20萬。就業數據靚,聯儲局有條件起碼按目前步伐加息。

- Inflation remains elevated —美國11月CPI回落至7.1%(由10月的7.7%),令市場最近開心咗一陣。但,即使CPI見頂,仍處7%以上高水平,距離~2%通脹目標水平仍有相當差距,FED有需要起碼按目前步伐加息。其實,即使FFR加到5%水平就停,不代表會馬上掉頭減息。另外,也要等埋FED更看重的11月core PCE,11月數據仍未出爐。上期,10月core PCE稍微回落至按年增長5.0%,但按月就仍然增長維持0.2%。

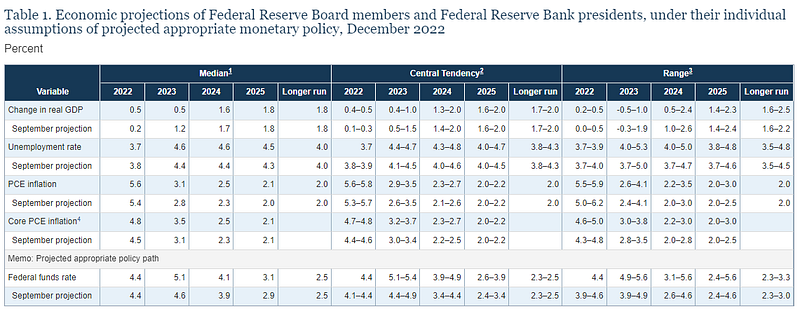

(2) FOMC經濟預測:

這才是戲玉,遠比上面的搬字過紙FOMC statement重要。

- 2023年FFR預測中位數,由上次9月預測的4.6%上調至5.1%,估計區間為4.9%至5.6%。2024年和2025年亦分別上調了0.2個百分點到4.1%和3.1%。按目前最新路徑圖看,FED在2023年加息到5%以上似乎事在必行,估計會在2024年實現掉頭減息。

- CME利率期貨市場數據反映,目前聰明錢下注2023年3月FFR加息至5%,維持到9月,然後11月掉頭減息至4.75%,12月再減息至4.5%。

- 另外,FED最看重的Core PCE inflation,2023年預計數字由9月預測的3.1%上調至3.5%,反映FED不認同高通脹受控之說。但,FED也把未來3年的失業率統統上調0.2個百分點,2023年和2024年預計失業率4.6%,也即是失業率將接近NAIRU ~5%水平,意味明年開始加息條件變得有限。

- 明年real GDP增長也由1.2%下調至0.5%,反映經濟著陸不能避免。

(3) Jay Powell記者會:

“I wish there were a completely painless way to restore price stability. There isn’t, and this is the best we can do… the largest amount of pain, the worst pain, would come from a failure to raise rates high enough and from us allowing inflation to become entrenched.”

“Our focus right now is really on moving our policy stance to one that is restrictive enough to ensure a return of inflation to our 2% goal over time, it’s not on rate cuts”

The inflation data received so far in October and November show a welcome reduction in the pace of price increases, but it will take substantially more evidence to give confidence inflation is on a sustained downward path”

- 我在11月文章提到,「看著經濟數據的走向,距離2%通脹目標仍遠,不太可能斷言看到加息的盡頭。對上一次相近的情況(高通脹差經濟),就要數到Paul Volcker在1980年把FFR加到20%才能把居高不下的滯脹解決。先例有限,也許FED暫時還是摸著石頭過河,也沒有信心要加到幾多厘才能壓倒通脹。」

- 果然,即使市場因為最新CPI數據似乎高興了一會兒,但Jay Powell似乎仍堅持Paul Volcker路徑,長痛不如短痛,即使明知經濟必受影響,也堅持加息壓通脹,也表示「最痛的結局」就是利率不夠高,壓不倒高通脹。其實,這正是Arthur Burns的結局,加一會兒又減,減一會兒又加,十年間壓不倒高通脹,經濟也不好,兩頭唔到岸。

- 所以Powell也說,現時要保持足夠緊縮(restrictive enough)的貨幣政策去把通脹壓到2%目標水平,目前談什麼掉頭減息都是言之尚早。10月和11月通脹數據不錯,但仍需要「大量更多證據」去證實通脹受控。

- 現時CPI距離2%通脹目標仍遠,不能太可能看到加息盡頭。今次比Volcker時期更多variables(俄烏戰爭、中國經濟放緩、供應鍊、能源糧食價格…),幾時掉頭減息,可能連FED官員心中都未有答案。

- 不過幾乎可以肯定,FED明年大部分時間都係維持偏高利率(>=5%),睇住最新數據,摸著石頭過河。

“We don’t talk about this kind of recession, that kind of a recession. We just make these forecasts… I don’t think it would qualify as a recession … That’s positive growth… it is not going to feel like a boom.”

- FOMC經濟預測圖估計,明年real GDP只按年微升0.5%,估計區間為負0.5%–正1.0%... 看到Powell這樣說,有點想起孔乙己,「GDP可能還有微增,不能算recession!」(笑)

投資:

- IMF最新2023展望報告提到,明年環球經濟增長降至2.7%,撇除2008年GFC及2020年COVID的話,估計是2001年以來最差的一年。明年全球面對三大風險:Russian-Ukraine War、cost-of-living crisis、中國經濟放緩。在這樣疲弱的經濟環境下,如果FFR仍維持在5%水平,企業借款成本不低,盈利又不見好轉,實體經濟不容樂觀。

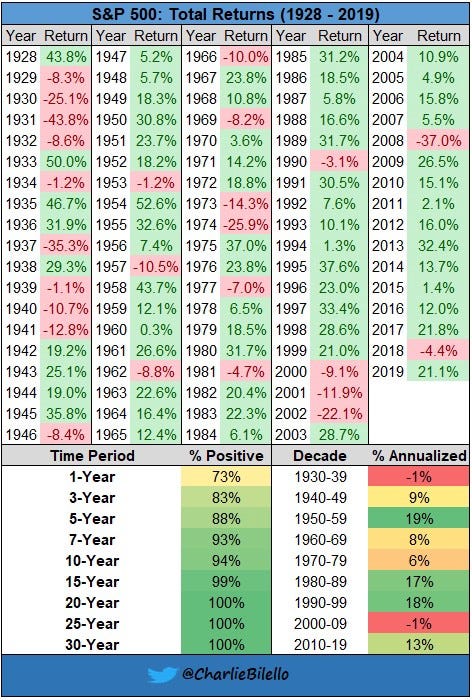

- 當然,股票是炒預期的,看估值的,就像2020年中期,疫情未平,美股已率先爆升,谷底在哪,只在事後才知,根本can’t catch the bottom。市場最近有點兒高興得太早,可在VOO回落時逢低吸納,分段累積。再一次貼出下圖,提提自己、提提大家,巴神如是說,“never bet against America”。不過,high beta stocks就暫時不碰,wake me up when 掉頭減息。

延伸閱讀: