鮑威爾選擇了Volcker路徑 — Jackson Hole演說原文導讀

TLDR:聯儲局的工作就是看通脹和失業率—現在通脹太高(一個月回落不算什麼),勞工市場過緊(失業率仍低於長期平均值),客觀來說benchmark rate仍不是特別高,尚有大把空間加息上去,別發夢短期內會掉頭減息了!再像Arthur Burns那樣拖拖拉拉加加減減,公眾就會形成高通脹預期,到時「自證預言」的高通脹就像雪球愈滾愈大,最終要像Volcker這樣「治亂世,下重典」才能解決,倒不如趁早繼續加息。

本欄在4月的三篇文章提到,Powell有兩條路可以選—取悅總統保持飯豌的Arthur Burns路徑,或者鐵面無私解決十年滯脹的Paul Volcker路徑。對於美國以至世界的貨幣經濟史,將會是重要的分水嶺。對於我們這些凡夫俗子來說,兩條路徑分別獎勵截然不同的投資決定。現在看來,Powell選擇了當時得罪全世界但名留青史的Volcker。

原文: https://www.federalreserve.gov/newsevents/speech/powell20220826a.htm

Thank you for the opportunity to speak here today.

At past Jackson Hole conferences, I have discussed broad topics such as the ever-changing structure of the economy and the challenges of conducting monetary policy under high uncertainty. Today, my remarks will be shorter, my focus narrower, and my message more direct.

The Federal Open Market Committee’s (FOMC) overarching focus right now is to bring inflation back down to our 2 percent goal. Price stability is the responsibility of the Federal Reserve and serves as the bedrock of our economy. Without price stability, the economy does not work for anyone. In particular, without price stability, we will not achieve a sustained period of strong labor market conditions that benefit all. The burdens of high inflation fall heaviest on those who are least able to bear them. (註:4月寫文解過,聯儲局的dual mandate就是控制通脹水平及失業率,通脹目標水平正是2%)

Restoring price stability will take some time and requires using our tools forcefully to bring demand and supply into better balance. Reducing inflation is likely to require a sustained period of below-trend growth. (註:聯儲局的tools主要是縮表及用OMO加息,鮑表明不但會用,而且會用一段長時間,去壓抑供求控制通脹)。Moreover, there will very likely be some softening of labor market conditions. While higher interest rates, slower growth, and softer labor market conditions will bring down inflation, they will also bring some pain to households and businesses. (註:現在失業率是3%,低於美國的長期平均失業率5%,反映勞工市場較緊張,因此近日歐美各行各業才有條件罷工要求加人工,也會進一步推動通脹,即wage-price spiral。高利率有助逆轉這情況。)These are the unfortunate costs of reducing inflation. But a failure to restore price stability would mean far greater pain.

The U.S. economy is clearly slowing from the historically high growth rates of 2021, which reflected the reopening of the economy following the pandemic recession. While the latest economic data have been mixed, in my view our economy continues to show strong underlying momentum.(註:雖然美國GDP陷入技竹整體認為經濟增長動力好)。The labor market is particularly strong, but it is clearly out of balance, with demand for workers substantially exceeding the supply of available workers. (註:再次提到勞工市場較緊張)Inflation is running well above 2 percent, and high inflation has continued to spread through the economy. While the lower inflation readings for July are welcome, a single month’s improvement falls far short of what the Committee will need to see before we are confident that inflation is moving down.(註:7月通脹稍為回落,聯儲局重申雖然樂見單月跌幅,但唔足夠,要見到通脹真正回落先會停加息。)

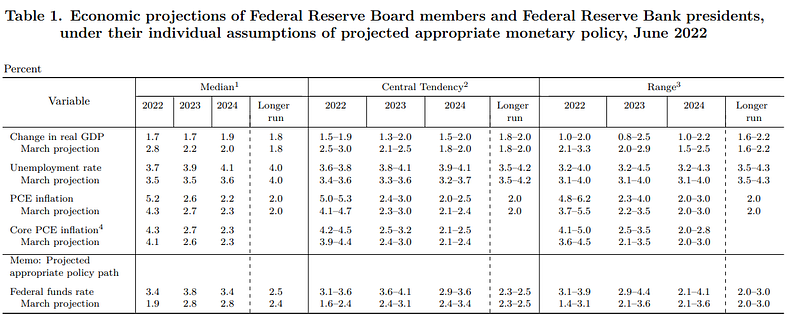

We are moving our policy stance purposefully to a level that will be sufficiently restrictive to return inflation to 2 percent. (註:再次強調2%通脹目標。)At our most recent meeting in July, the FOMC raised the target range for the federal funds rate to 2.25 to 2.5 percent, which is in the Summary of Economic Projection’s (SEP) range of estimates of where the federal funds rate is projected to settle in the longer run.In current circumstances, with inflation running far above 2 percent and the labor market extremely tight, estimates of longer-run neutral are not a place to stop or pause.(註:見下圖,SEP個longer run合理利率range是2.0%–3.0%,新常態。現在FED 7月才加到2.25%-2.5%,仍在這個neutral的range內,一點也不會太高,所以不用期望FED這樣就會掉頭減息,而且基於通脹過高勞動力市場過緊,加息不會停下來。)

July’s increase in the target range was the second 75 basis point increase in as many meetings, and I said then that another unusually large increase could be appropriate at our next meeting.We are now about halfway through the intermeeting period. Our decision at the September meeting will depend on the totality of the incoming data and the evolving outlook. At some point, as the stance of monetary policy tightens further, it likely will become appropriate to slow the pace of increases.(註:7月議息是第二次加三碼, 下次再加三碼也有可能,還是看經濟數據說話。)

Restoring price stability will likely require maintaining a restrictive policy stance for some time. The historical record cautions strongly against prematurely loosening policy. (註:要回復物價水平穩定,要收緊貨幣政策一段時間才能見效,不是一步到位的。歷史上一掉頭放鬆就出事—參考本欄4月文章寫過的70年代美國解決通脹危機的故事)Committee participants’ most recent individual projections from the June SEP showed the median federal funds rate running slightly below 4 percent through the end of 2023.(註:上面同一張圖。SEP 6月預計2023年尾中位數是要加息加到稍低於4%,9月會再更新,做好心理準備。) Participants will update their projections at the September meeting.

Our monetary policy deliberations and decisions build on what we have learned about inflation dynamics both from the high and volatile inflation of the 1970s and 1980s, and from the low and stable inflation of the past quarter-century. (註:參考本欄4月文章 - 70年代美國解決通脹危機的故事)In particular, we are drawing on three important lessons.

The first lesson is that central banks can and should take responsibility for delivering low and stable inflation.(註:央行有能力、有責任保持低而穩定的通脹率。) It may seem strange now that central bankers and others once needed convincing on these two fronts, but as former Chairman Ben Bernanke has shown, both propositions were widely questioned during the Great Inflation period.1 Today, we regard these questions as settled. Our responsibility to deliver price stability is unconditional. It is true that the current high inflation is a global phenomenon, and that many economies around the world face inflation as high or higher than seen here in the United States. It is also true, in my view, that the current high inflation in the United States is the product of strong demand and constrained supply, and that the Fed’s tools work principally on aggregate demand.None of this diminishes the Federal Reserve’s responsibility to carry out our assigned task of achieving price stability. There is clearly a job to do in moderating demand to better align with supply. (註:雖然高通脹主要源自supply chain disruption同energy prices,係全球現象,但高中Econ都有教 — 央行monetary policy係有用的,可以加息去拉低aggregate demand(AD)推低price level)We are committed to doing that job.

The second lesson is that the public’s expectations about future inflation can play an important role in setting the path of inflation over time.(註:本欄經常提到的公式Fisher Effect,real interest rate= nominal interest rate — expected inflation。如果公眾預期高通脹,實質利率只會更高,進一步刺激AD推高P,變成「自證預言」。)Today, by many measures, longer-term inflation expectations appear to remain well anchored. That is broadly true of surveys of households, businesses, and forecasters, and of market-based measures as well.But that is not grounds for complacency, with inflation having run well above our goal for some time.(註:目前公眾通脹預期合理、理性。)

If the public expects that inflation will remain low and stable over time, then, absent major shocks, it likely will. Unfortunately, the same is true of expectations of high and volatile inflation. (註:只要公眾預期長遠通脹會回到低而穩定水平,除非發生重大事故,否則通常成真。但,反之亦然)During the 1970s, as inflation climbed, the anticipation of high inflation became entrenched in the economic decisionmaking of households and businesses. The more inflation rose, the more people came to expect it to remain high, and they built that belief into wage and pricing decisions. As former Chairman Paul Volcker put it at the height of the Great Inflation in 1979, “Inflation feeds in part on itself, so part of the job of returning to a more stable and more productive economy must be to break the grip of inflationary expectations.”2(註:正如前述,公眾通脹預期和之後的通脹率,是一種「自證預言」)

One useful insight into how actual inflation may affect expectations about its future path is based in the concept of “rational inattention.” (註:中文應譯做「 理性疏忽」?意思係,做一個決定時,如果要獲取所有相關資訊成本太高,決策者就寧願理性地只基於部分資訊去做決定。簡單說,你可以調查全世界智能手機的spec和用後感,才去決定買哪部手機,但由於太費時,你決定不考慮這些,直接繼續買iPhone吧。)3 When inflation is persistently high, households and businesses must pay close attention and incorporate inflation into their economic decisions. When inflation is low and stable, they are freer to focus their attention elsewhere. Former Chairman Alan Greenspan put it this way: “For all practical purposes, price stability means that expected changes in the average price level are small enough and gradual enough that they do not materially enter business and household financial decisions.”4 (註:通脹高時,大家關注通脹,做決定時也考慮通脹。所謂物價水平穩定,是當公眾預期長遠通脹會在低而穩定水平,他們做決定時根本不考慮通脹問題。)

Of course, inflation has just about everyone’s attention right now, which highlights a particular risk today: The longer the current bout of high inflation continues, the greater the chance that expectations of higher inflation will become entrenched.(註:但,高通脹持續愈久,公眾的通脹預期通常愈高,那問題就來了。)

That brings me to the third lesson, which is that we must keep at it until the job is done. (註:因此,不能讓通脹像在Arthur Burns擔任FED主席時那麼長期持續,要加息加到壓倒通脹。)History shows that the employment costs of bringing down inflation are likely to increase with delay, as high inflation becomes more entrenched in wage and price setting. The successful Volcker disinflation in the early 1980s followed multiple failed attempts to lower inflation over the previous 15 years. A lengthy period of very restrictive monetary policy was ultimately needed to stem the high inflation and start the process of getting inflation down to the low and stable levels that were the norm until the spring of last year. Our aim is to avoid that outcome by acting with resolve now.(註:參考本欄4月文章寫過的70年代美國解決通脹危機的故事。Volcker成功之前的15年,FED就是沒有下定決心壓通脹,不斷拖拖拉拉,加一會,減一會,令高通脹延續太久,以致公眾高通脹預期形成,最終Volcker要下重手加到20厘以上。因此,還是應該「長痛不如短痛」。)

These lessons are guiding us as we use our tools to bring inflation down. We are taking forceful and rapid steps to moderate demand so that it comes into better alignment with supply, and to keep inflation expectations anchored. We will keep at it until we are confident the job is done.

延伸閱讀:

https://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20220615.pdf